Answered step by step

Verified Expert Solution

Question

1 Approved Answer

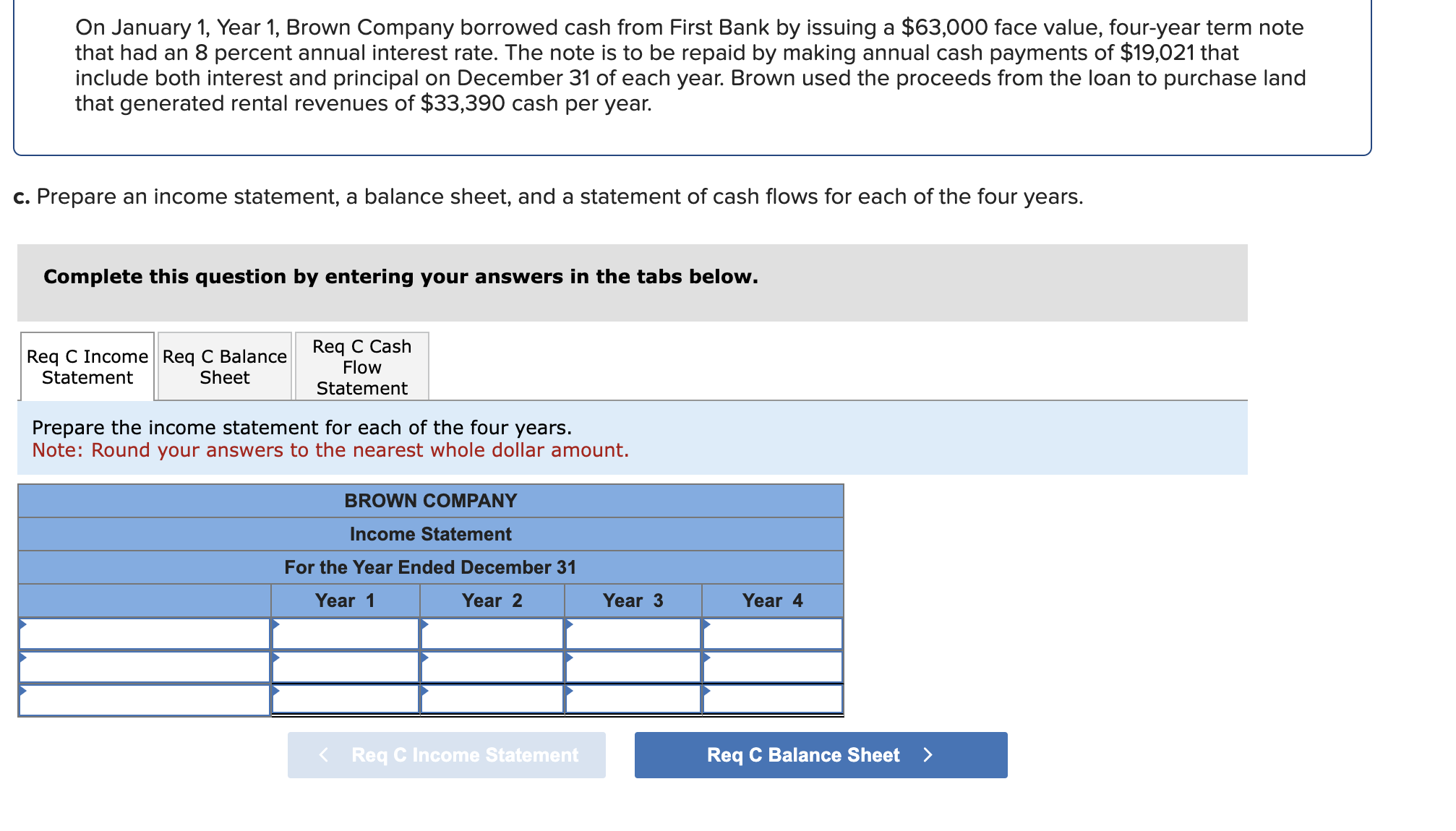

On January 1, Year 1, Brown Company borrowed cash from First Bank by issuing a $63,000 face value, four-year term note that had an 8

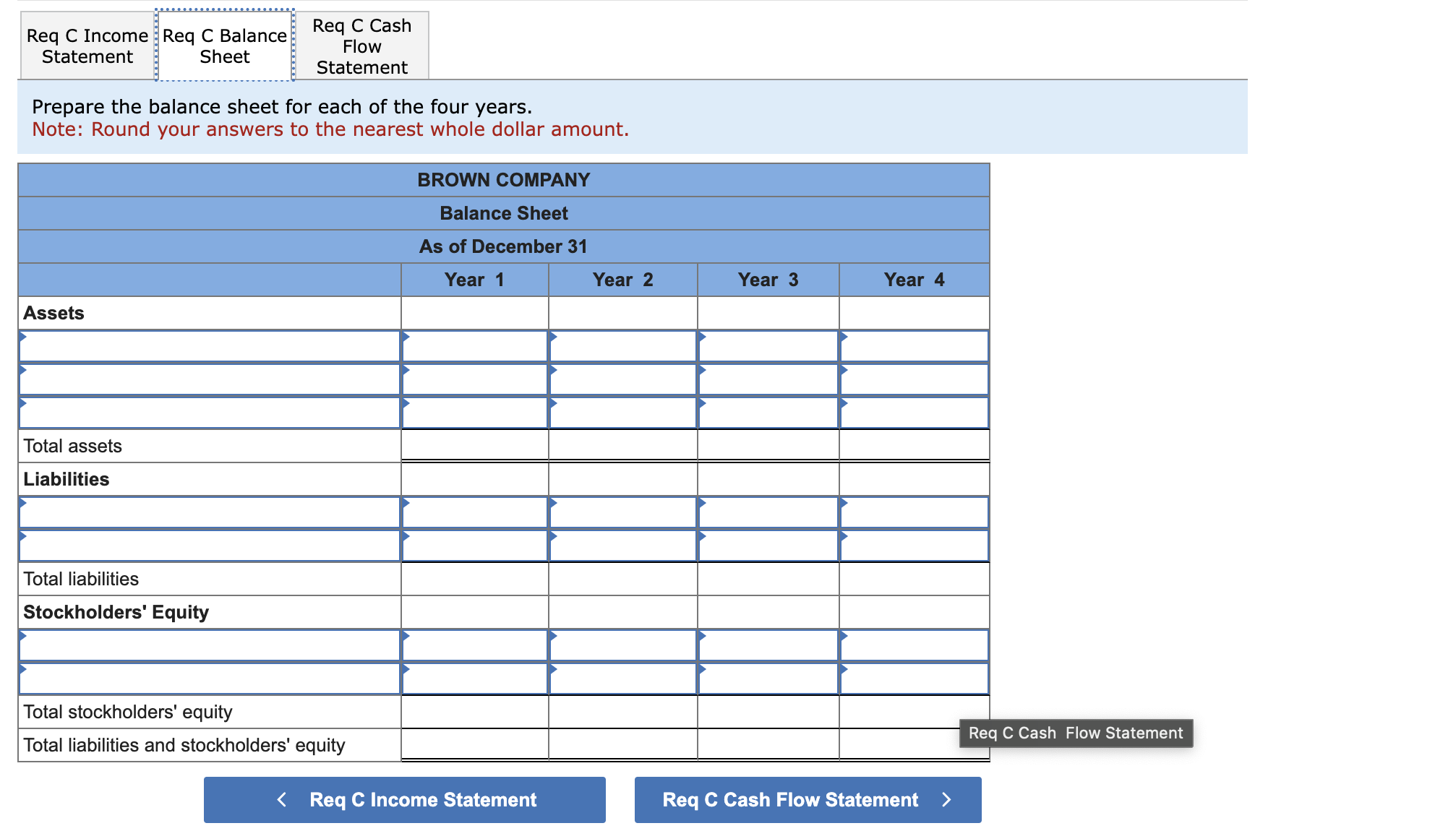

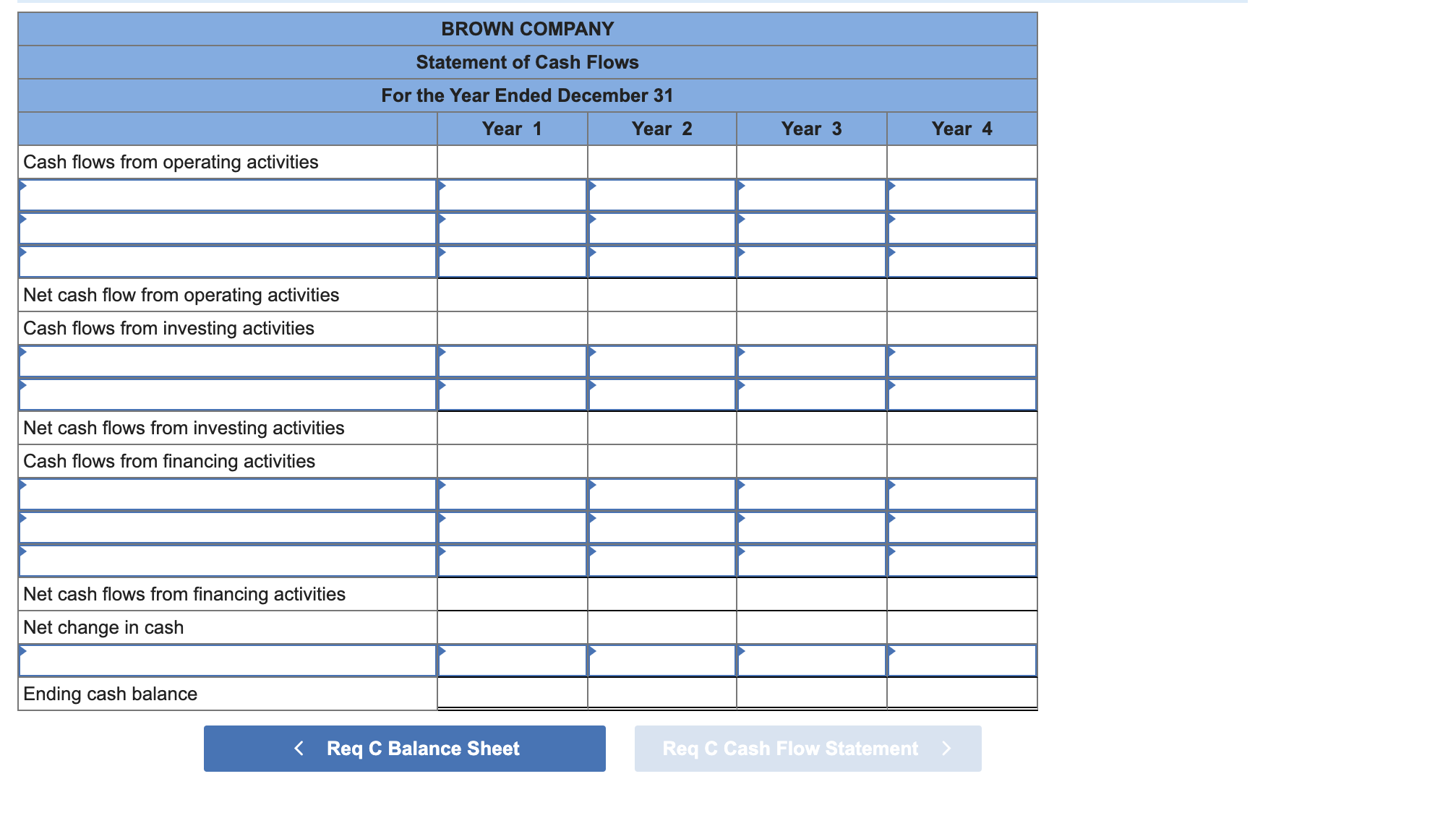

On January 1, Year 1, Brown Company borrowed cash from First Bank by issuing a $63,000 face value, four-year term note that had an 8 percent annual interest rate. The note is to be repaid by making annual cash payments of $19,021 that include both interest and principal on December 31 of each year. Brown used the proceeds from the loan to purchase land that generated rental revenues of $33,390 cash per year. Prepare an income statement, a balance sheet, and a statement of cash flows for each of the four years. Complete this question by entering your answers in the tabs below. Prepare the income statement for each of the four years. Note: Round your answers to the nearest whole dollar amount. Prepare the balance sheet for each of the four years. Note: Round your answers to the nearest whole dollar amount

On January 1, Year 1, Brown Company borrowed cash from First Bank by issuing a $63,000 face value, four-year term note that had an 8 percent annual interest rate. The note is to be repaid by making annual cash payments of $19,021 that include both interest and principal on December 31 of each year. Brown used the proceeds from the loan to purchase land that generated rental revenues of $33,390 cash per year. Prepare an income statement, a balance sheet, and a statement of cash flows for each of the four years. Complete this question by entering your answers in the tabs below. Prepare the income statement for each of the four years. Note: Round your answers to the nearest whole dollar amount. Prepare the balance sheet for each of the four years. Note: Round your answers to the nearest whole dollar amount Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started