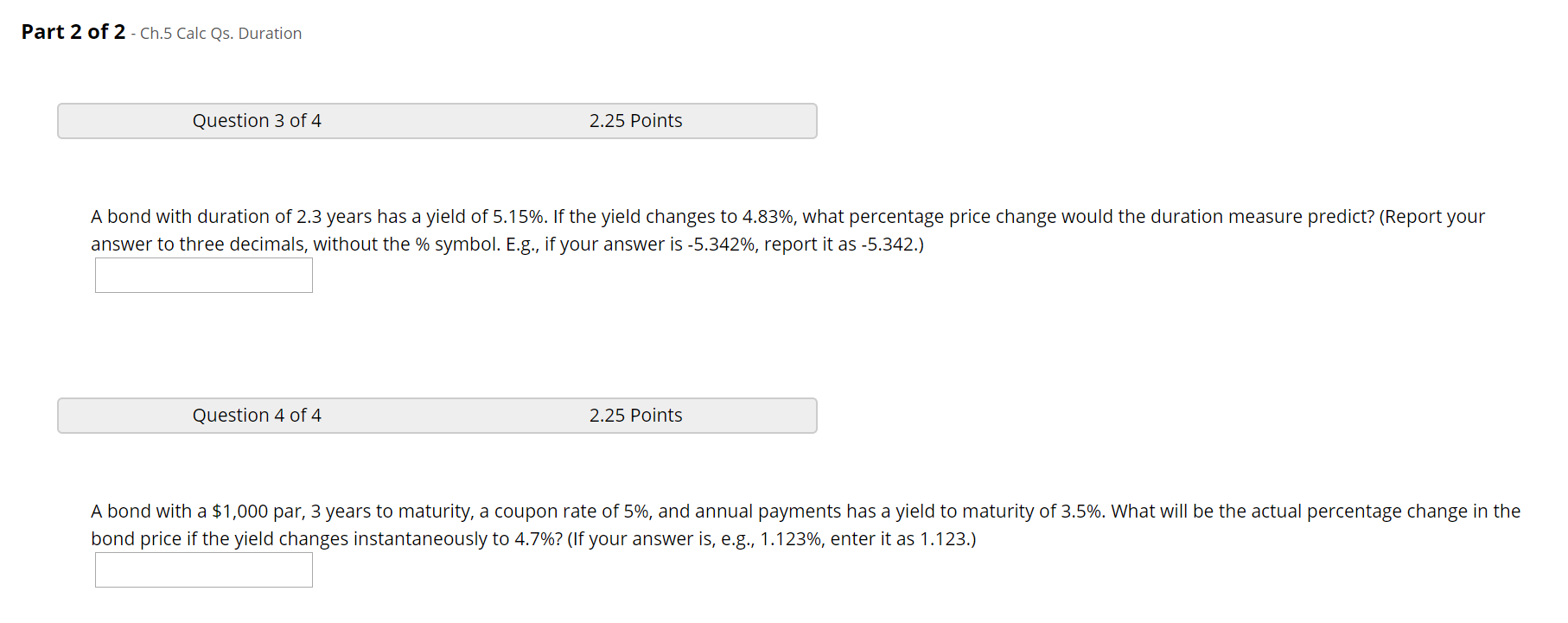

Question: Part 2 of 2 - Ch.5 Calc Qs. Duration Question 3 of 4 2.25 Points A bond with duration of 2.3 years has a yield

Part 2 of 2 - Ch.5 Calc Qs. Duration Question 3 of 4 2.25 Points A bond with duration of 2.3 years has a yield of 5.15%. If the yield changes to 4.83%, what percentage price change would the duration measure predict? (Report your answer to three decimals, without the % symbol. E.g., if your answer is -5.342%, report it as -5.342.) Question 4 of 4 2.25 Points A bond with a $1,000 par, 3 years to maturity, a coupon rate of 5%, and annual payments has a yield to maturity of 3.5%. What will be the actual percentage change in the bond price if the yield changes instantaneously to 4.7%? (If your answer is, e.g., 1.123%, enter it as 1.123.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts