Answered step by step

Verified Expert Solution

Question

1 Approved Answer

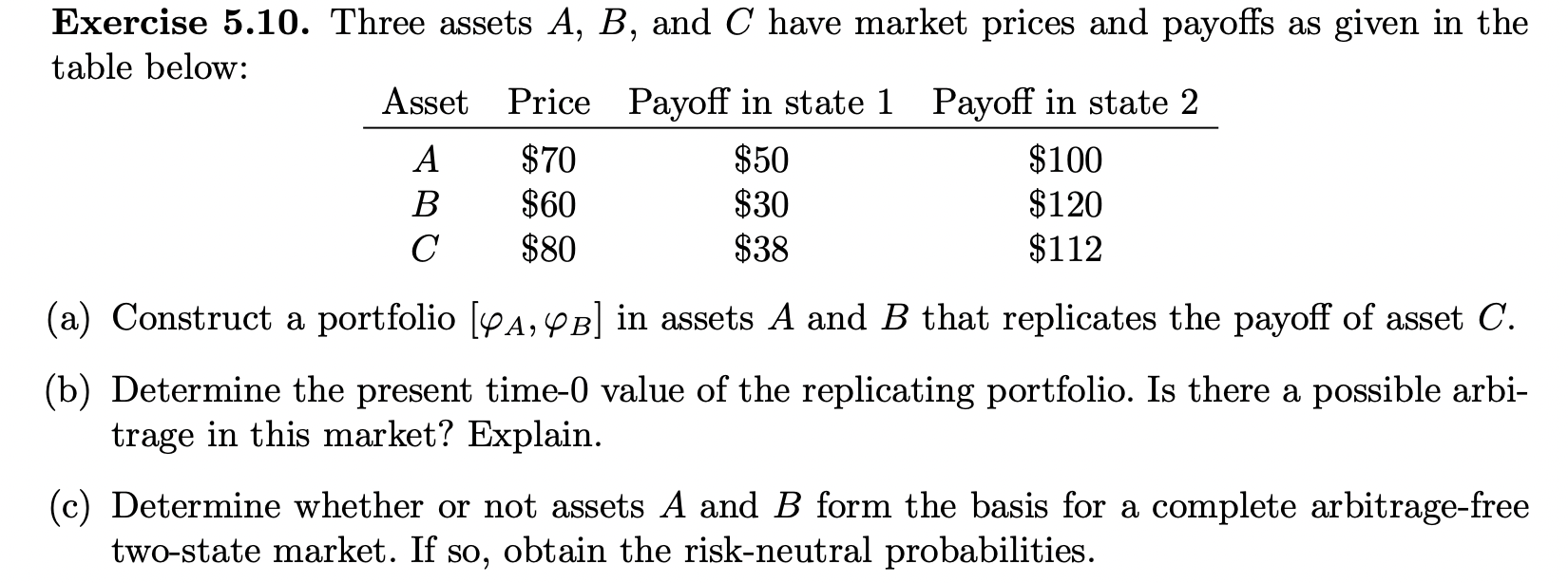

Please answer in detailed steps. Exercise 5.10. Three assets A,B, and C have market prices and payoffs as given in the table below: (a) Construct

Please answer in detailed steps.

Exercise 5.10. Three assets A,B, and C have market prices and payoffs as given in the table below: (a) Construct a portfolio [A,B] in assets A and B that replicates the payoff of asset C. (b) Determine the present time- 0 value of the replicating portfolio. Is there a possible arbitrage in this market? Explain. (c) Determine whether or not assets A and B form the basis for a complete arbitrage-free two-state market. If so, obtain the risk-neutral probabilitiesStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Essential Nonprofit Fundraising Handbook

Authors: Michael A. Sand, Linda Lysakowski

1st Edition

1601630727, 978-1601630728