Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please provide solution details Q4) A stock is expected to pay a dividend of $1 per share in 2 months and in 5 months. The

please provide solution details

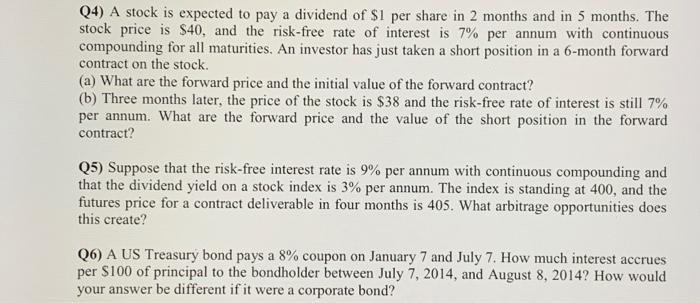

Q4) A stock is expected to pay a dividend of $1 per share in 2 months and in 5 months. The stock price is $40, and the risk-free rate of interest is 7% per annum with continuous compounding for all maturities. An investor has just taken a short position in a 6-month forward contract on the stock. (a) What are the forward price and the initial value of the forward contract? (b) Three months later, the price of the stock is $38 and the risk-free rate of interest is still 7% per annum. What are the forward price and the value of the short position in the forward contract? Q5) Suppose that the risk-free interest rate is 9% per annum with continuous compounding and that the dividend yield on a stock index is 3% per annum. The index is standing at 400 , and the futures price for a contract deliverable in four months is 405 . What arbitrage opportunities does this create? Q6) A US Treasury bond pays a 8% coupon on January 7 and July 7 . How much interest accrues per $100 of principal to the bondholder between July 7, 2014, and August 8, 2014? How would your answer be different if it were a corporate bond Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Housing An Introduction

Authors: Cathy Davis

1st Edition

1447306481, 978-1447306481