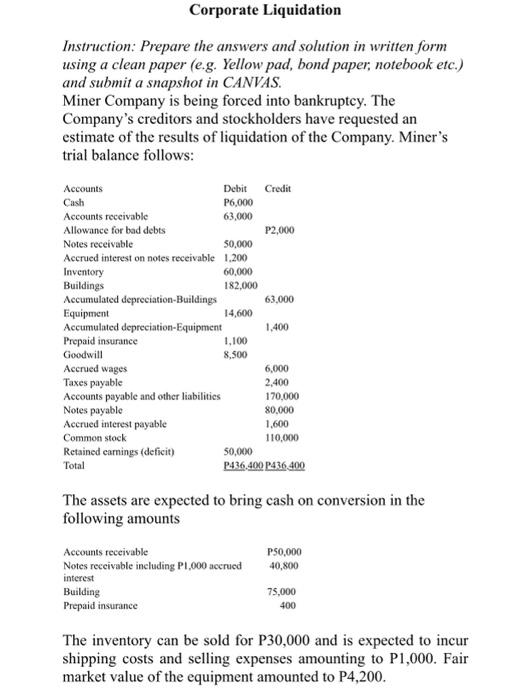

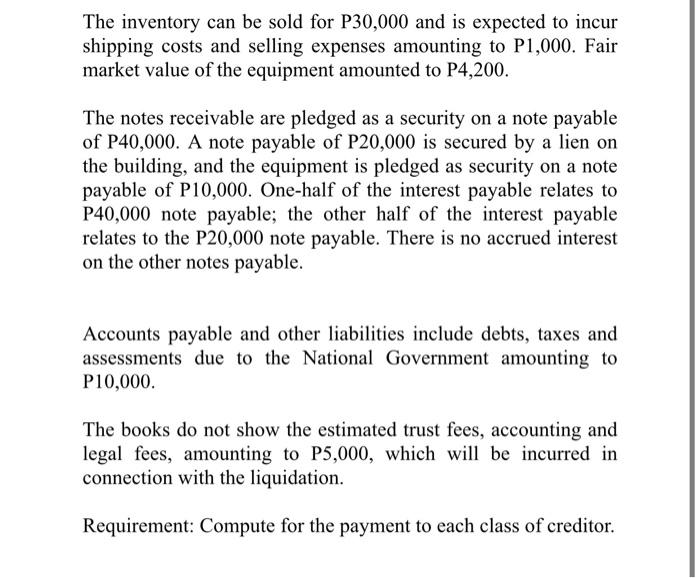

Corporate Liquidation Instruction: Prepare the answers and solution in written form using a clean paper (eg. Yellow pad, bond paper, notebook etc.) and submit a snapshot in CANVAS. Miner Company is being forced into bankruptcy. The Company's creditors and stockholders have requested an estimate of the results of liquidation of the Company. Miner's trial balance follows: Accounts Debit Credit Cash P6,000 Accounts receivable 63,000 Allowance for bad debts P2,000 Notes receivable 50.000 Accrued interest on notes receivable 1.200 Inventory 60,000 Buildings 182,000 Accumulated depreciation Buildings 63.000 Equipment 14,600 Accumulated depreciation-Equipment 1.400 Prepaid insurance 1.100 Goodwill 8,500 Accrued wages 6,000 Taxes payable 2,400 Accounts payable and other liabilities 170,000 Notes payable 80,000 Accrued interest payable 1.600 Common stock 110,000 Retained carnings (deficit) 50,000 Total P436.400 P436 400 The assets are expected to bring cash on conversion in the following amounts P50,000 40,800 Accounts receivable Notes receivable including P1,000 accrued interest Building Prepaid insurance 75,000 400 The inventory can be sold for P30,000 and is expected to incur shipping costs and selling expenses amounting to P1,000. Fair market value of the equipment amounted to P4,200. The inventory can be sold for P30,000 and is expected to incur shipping costs and selling expenses amounting to P1,000. Fair market value of the equipment amounted to P4,200. The notes receivable are pledged as a security on a note payable of P40,000. A note payable of P20,000 is secured by a lien on the building, and the equipment is pledged as security on a note payable of P10,000. One-half of the interest payable relates to P40,000 note payable; the other half of the interest payable relates to the P20,000 note payable. There is no accrued interest on the other notes payable. Accounts payable and other liabilities include debts, taxes and assessments due to the National Government amounting to P10,000. The books do not show the estimated trust fees, accounting and legal fees, amounting to P5,000, which will be incurred in connection with the liquidation. Requirement: Compute for the payment to each class of creditor. Corporate Liquidation Instruction: Prepare the answers and solution in written form using a clean paper (eg. Yellow pad, bond paper, notebook etc.) and submit a snapshot in CANVAS. Miner Company is being forced into bankruptcy. The Company's creditors and stockholders have requested an estimate of the results of liquidation of the Company. Miner's trial balance follows: Accounts Debit Credit Cash P6,000 Accounts receivable 63,000 Allowance for bad debts P2,000 Notes receivable 50.000 Accrued interest on notes receivable 1.200 Inventory 60,000 Buildings 182,000 Accumulated depreciation Buildings 63.000 Equipment 14,600 Accumulated depreciation-Equipment 1.400 Prepaid insurance 1.100 Goodwill 8,500 Accrued wages 6,000 Taxes payable 2,400 Accounts payable and other liabilities 170,000 Notes payable 80,000 Accrued interest payable 1.600 Common stock 110,000 Retained carnings (deficit) 50,000 Total P436.400 P436 400 The assets are expected to bring cash on conversion in the following amounts P50,000 40,800 Accounts receivable Notes receivable including P1,000 accrued interest Building Prepaid insurance 75,000 400 The inventory can be sold for P30,000 and is expected to incur shipping costs and selling expenses amounting to P1,000. Fair market value of the equipment amounted to P4,200. The inventory can be sold for P30,000 and is expected to incur shipping costs and selling expenses amounting to P1,000. Fair market value of the equipment amounted to P4,200. The notes receivable are pledged as a security on a note payable of P40,000. A note payable of P20,000 is secured by a lien on the building, and the equipment is pledged as security on a note payable of P10,000. One-half of the interest payable relates to P40,000 note payable; the other half of the interest payable relates to the P20,000 note payable. There is no accrued interest on the other notes payable. Accounts payable and other liabilities include debts, taxes and assessments due to the National Government amounting to P10,000. The books do not show the estimated trust fees, accounting and legal fees, amounting to P5,000, which will be incurred in connection with the liquidation. Requirement: Compute for the payment to each class of creditor