please type out the answer. thank you! ONLY ANswer #5

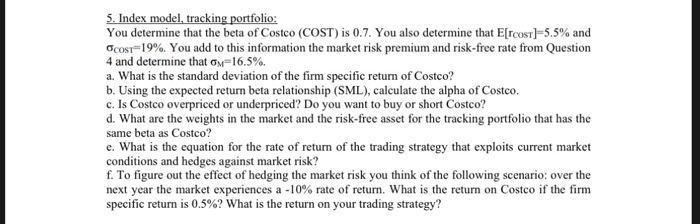

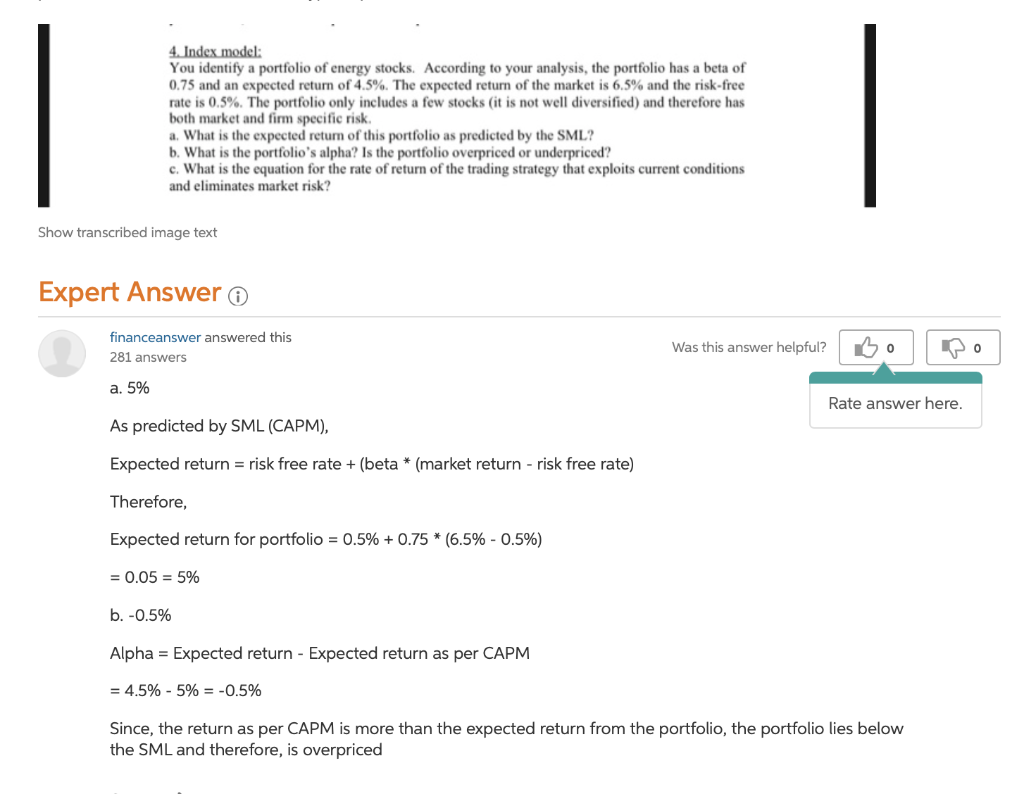

5. Index model, tracking portfolio: You determine that the beta of Costco (COST) is 0.7. You also determine that E[rosh-5.5% and Ogos,-19%. You add to this information the market risk premium and risk-free rate from Question 4 and determine that or 16.5%. a. What is the standard deviation of the firm specific return of Costco? b. Using the expected return beta relationship (SML), calculate the alpha of Costco. c. Is Costco overpriced or underpriced? Do you want to buy or short Costco? d. What are the weights in the market and the risk-free asset for the tracking portfolio that has the same beta as Costco? e. What is the equation for the rate of return of the trading strategy that exploits current market conditions and hedges against market risk? f. To figure out the effect of hedging the market risk you think of the following scenario: over the next year the market experiences a-10% rate of return. What is the return on Costco if the firm specific return is 0.5%? What is the return on your trading strategy? You identify a portfolio of energy stocks. According to your analysis, the portfolio has a beta of 0.75 and an expected return of 4.5%. The expected return of the market is 6.5% and the risk-free rate is 0.5%. The portfolio only includes a few stocks (it is not well diversified) and therefore has both market and firm specific risk a. What is the expected return of this portfolio as predicted by the SML? b. What is the portfolio's alpha? Is the portfolio overpriced or underpriced? c. What is the equation for the rate of return of the trading strategy that exploits current conditions and eliminates market risk? Show transcribed image text Expert Answer@ financeanswer answered this Was this answer helpful? 0 281 answers a.5% As predicted by SML (CAPM), Expected return risk free rate (beta (market return - risk free rate) Therefore Expected return for portfolio = 0.5% + 0.75 * (6.5%-0.5%) -0.05-5% b.-0.5% Alpha = Expected return-Expected return as per CAPM = 4.5%-5% =-0.5% Since, the return as per CAPM is more than the expected return from the portfolio, the portfolio lies below Rate answer here the SML and therefore, is overpriced 5. Index model, tracking portfolio: You determine that the beta of Costco (COST) is 0.7. You also determine that E[rosh-5.5% and Ogos,-19%. You add to this information the market risk premium and risk-free rate from Question 4 and determine that or 16.5%. a. What is the standard deviation of the firm specific return of Costco? b. Using the expected return beta relationship (SML), calculate the alpha of Costco. c. Is Costco overpriced or underpriced? Do you want to buy or short Costco? d. What are the weights in the market and the risk-free asset for the tracking portfolio that has the same beta as Costco? e. What is the equation for the rate of return of the trading strategy that exploits current market conditions and hedges against market risk? f. To figure out the effect of hedging the market risk you think of the following scenario: over the next year the market experiences a-10% rate of return. What is the return on Costco if the firm specific return is 0.5%? What is the return on your trading strategy? You identify a portfolio of energy stocks. According to your analysis, the portfolio has a beta of 0.75 and an expected return of 4.5%. The expected return of the market is 6.5% and the risk-free rate is 0.5%. The portfolio only includes a few stocks (it is not well diversified) and therefore has both market and firm specific risk a. What is the expected return of this portfolio as predicted by the SML? b. What is the portfolio's alpha? Is the portfolio overpriced or underpriced? c. What is the equation for the rate of return of the trading strategy that exploits current conditions and eliminates market risk? Show transcribed image text Expert Answer@ financeanswer answered this Was this answer helpful? 0 281 answers a.5% As predicted by SML (CAPM), Expected return risk free rate (beta (market return - risk free rate) Therefore Expected return for portfolio = 0.5% + 0.75 * (6.5%-0.5%) -0.05-5% b.-0.5% Alpha = Expected return-Expected return as per CAPM = 4.5%-5% =-0.5% Since, the return as per CAPM is more than the expected return from the portfolio, the portfolio lies below Rate answer here the SML and therefore, is overpriced