Question

Preparing the [I] consolidation entries for sale of depreciable assetsCost method Assume that on January 1, 2013, a parent sells to its wholly owned subsidiary,

Preparing the [I] consolidation entries for sale of depreciable assetsCost method Assume that on January 1, 2013, a parent sells to its wholly owned subsidiary, for a sale price of $226800 equipment that originally cost $259200 The parent originally purchased the equipment on January 1, 2009, and depreciated the equipment assuming a 12-year useful life (straight-line with no salvage value). The subsidiary has adopted the parents depreciation policy and depreciates the equipment over the remaining useful life of 8 years. The parent uses the cost method of pre-consolidation investment bookkeeping.

a. Compute the pre-consolidation annual depreciation expense for the subsidiary (post-intercompany sale) and the parent (pre-intercompany sale).

b. Compute the pre-consolidation Gain on Sale recognized by the parent during 2013.

c. Prepare the required [I] consolidation entry in 2013 (assume a full year of depreciation).

d. With respect to the deferred gain on intercompany sale, what effect (i.e., amount) will it have on the [ADJ] entry necessary to prepare the consolidated financial statements for the year ended December 31, 2016? In addition, specify the account that will be debited and the account that will be credited in the [ADJ] entry for the effect of the deferred gain on intercompany sale.

Prepare the [ADJ] consolidation entry for December 31, 2016 to show the effect of the deferred gain on the intercompany sale.

e. Prepare the required [I] consolidation entry in 2016 (assuming the subsidiary is still holding the equipment).

***Please help with C, D, & E***

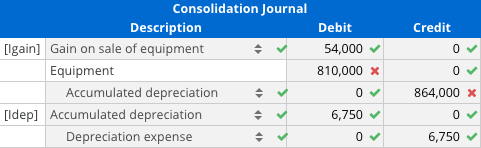

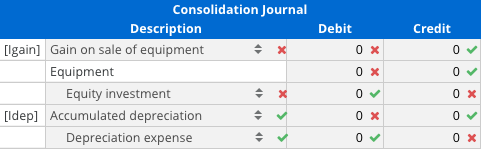

Parent depreciation expense Subsidiary depreciation expense 21,600 28,350 $ 54,000 Credit 0 Consolidation Journal Description [lgain] Gain on sale of equipment Equipment Accumulated depreciation [ldep] Accumulated depreciation Depreciation expense Debit 54,000 810,000 x 0 0 864,000 x 0 6,750 6,750 0 Debit Consolidation Journal Description [AD]] BOY Retained earnings-Parent Equity investment 54,000 x 0 Credit 0 54,000 x Debit 0 X Credit 0 X Consolidation Journal Description [lgain] Gain on sale of equipment Equipment Equity investment [ldep] Accumulated depreciation Depreciation expense 0 x 0 > X 0 0 X OX 0 0 0 X Parent depreciation expense Subsidiary depreciation expense 21,600 28,350 $ 54,000 Credit 0 Consolidation Journal Description [lgain] Gain on sale of equipment Equipment Accumulated depreciation [ldep] Accumulated depreciation Depreciation expense Debit 54,000 810,000 x 0 0 864,000 x 0 6,750 6,750 0 Debit Consolidation Journal Description [AD]] BOY Retained earnings-Parent Equity investment 54,000 x 0 Credit 0 54,000 x Debit 0 X Credit 0 X Consolidation Journal Description [lgain] Gain on sale of equipment Equipment Equity investment [ldep] Accumulated depreciation Depreciation expense 0 x 0 > X 0 0 X OX 0 0 0 XStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Frauds Of The Past Lessons For The Future A Student Led Journey Through The World Of Auditing

Authors: Dr. Manjari Sharma, Mr. Pragadeesh SP, Mr. Sivanaresh A

1st Edition

B0CGKRP289, 978-6206753247