Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Q2. Please show excel formulas. Problem 2 You have until 11:36 PM to complete thing assignment. Intro The current level of a broad stock market

Q2. Please show excel formulas.

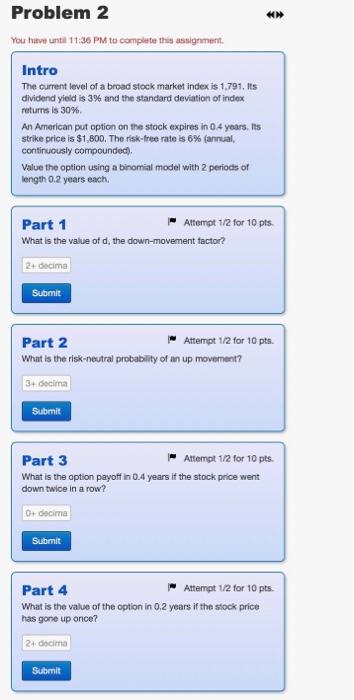

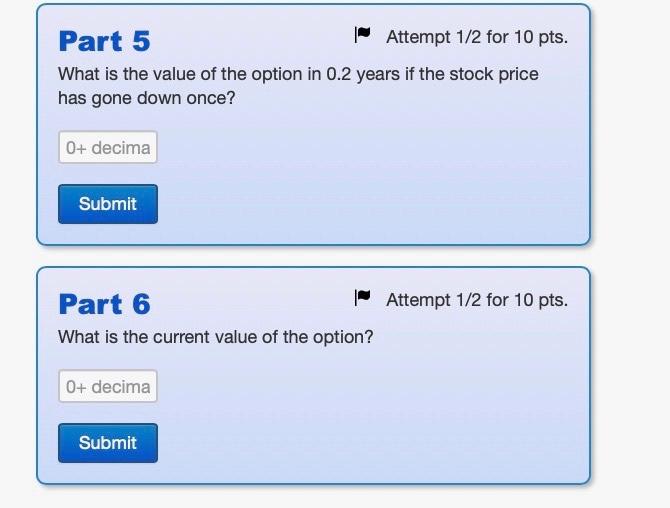

Problem 2 You have until 11:36 PM to complete thing assignment. Intro The current level of a broad stock market index is 1.791. Its dividend yield is 3% and the standard deviation of index returns is 30% An American put option on the stock expires in 0.4 years. Its strike price is $1,800. The risk-free rate is 6% annual continuously compounded) Value the option using a binomial model with 2 periods of length 0.2 years each. Part 1 Attempt 1/2 for 10 pts What is the value of d, the down-movement factor? 2+ decima Submit Part 2 Attempt 1/2 for 10 pts. What is the risk-neutral probability of an up movement? 31.decima Submit Part 3 Attempt 1/2 for 10 pts What is the option payoff in 0.4 years if the stock price went down twice in a row? 0+ decima Submit Part 4 Attempt 1/2 for 10 pts. What is the value of the option in 0.2 years if the stock price has gone up once? 2 decim Submit Part 5 | Attempt 1/2 for 10 pts. What is the value of the option in 0.2 years if the stock price has gone down once? 0+ decima Submit Part 6 6 - Attempt 1/2 for 10 pts. What is the current value of the option? 0+ decima Submit Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets and Institutions

Authors: Jeff Madura

12th edition

9781337515535, 1337099740, 1337515531, 978-1337099745