Answered step by step

Verified Expert Solution

Question

1 Approved Answer

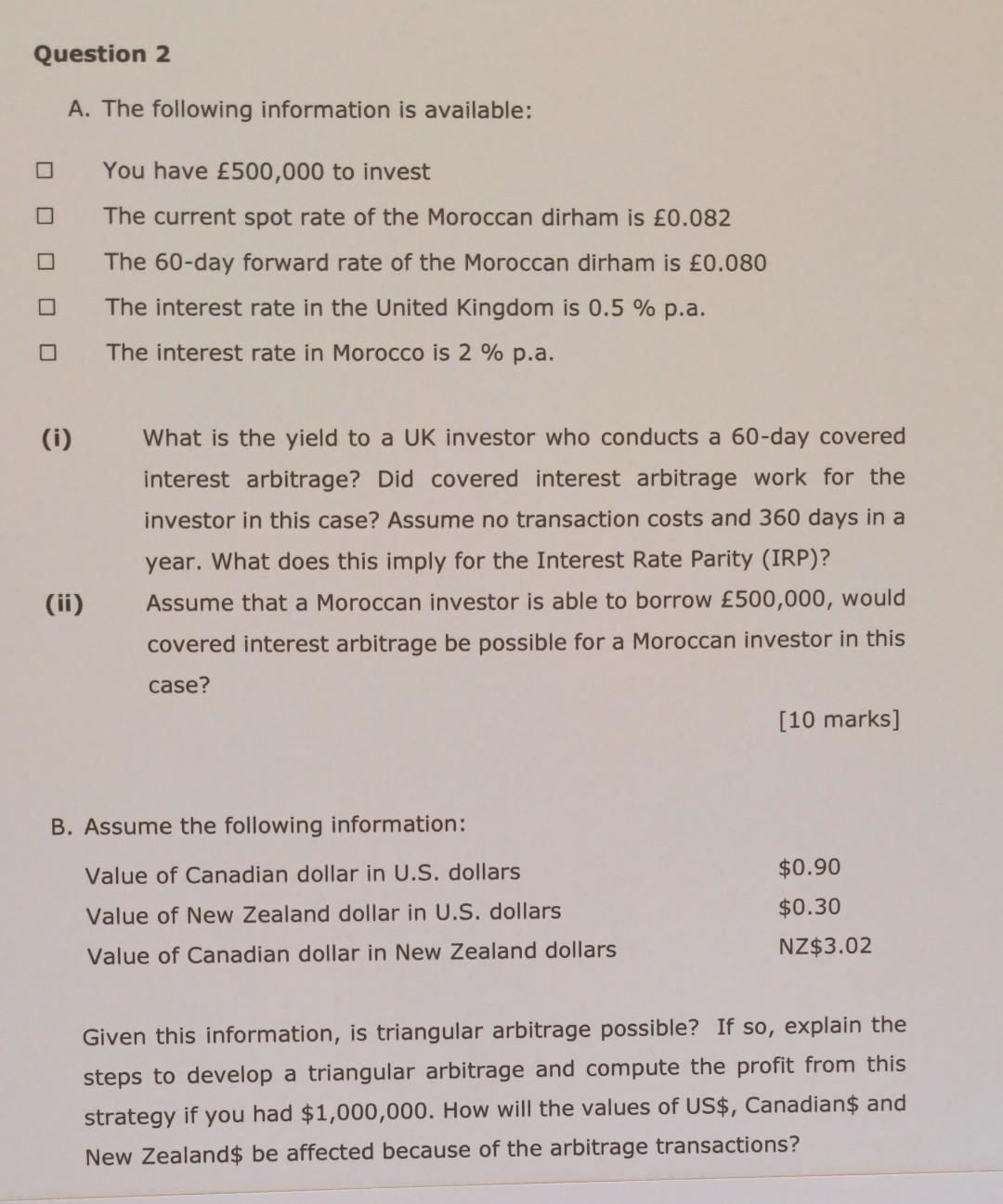

Question 2 A. The following information is available: You have 500,000 to invest The current spot rate of the Moroccan dirham is 0.082 The 60-day

Question 2 A. The following information is available: You have 500,000 to invest The current spot rate of the Moroccan dirham is 0.082 The 60-day forward rate of the Moroccan dirham is 0.080 O D The interest rate in the United Kingdom is 0.5 % p.a. The interest rate in Morocco is 2 % p.a. (i) What is the yield to a UK investor who conducts a 60-day covered interest arbitrage? Did covered interest arbitrage work for the investor in this case? Assume no transaction costs and 360 days in a year. What does this imply for the Interest Rate Parity (IRP)? Assume that a Moroccan investor is able to borrow 500,000, would covered interest arbitrage be possible for a Moroccan investor in this a case? [10 marks] (ii) B. Assume the following information: Value of Canadian dollar in U.S. dollars $0.90 Value of New Zealand dollar in U.S. dollars $0.30 NZ$3.02 Value of Canadian dollar in New Zealand dollars Given this information, is triangular arbitrage possible? If so, explain the steps to develop a triangular arbitrage and compute the profit from this strategy if you had $1,000,000. How will the values of US$, Canadians and New Zealand$ be affected because of the arbitrage transactions

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments An Introduction

Authors: Herbert B Mayo

9th Edition

324561385, 978-0324561388