Answered step by step

Verified Expert Solution

Question

1 Approved Answer

recording a change in estimate, an error correction, and a change in accounting principle Recording a Change in Estimate, an Error Correction, and a Change

recording a change in estimate, an error correction, and a change in accounting principle

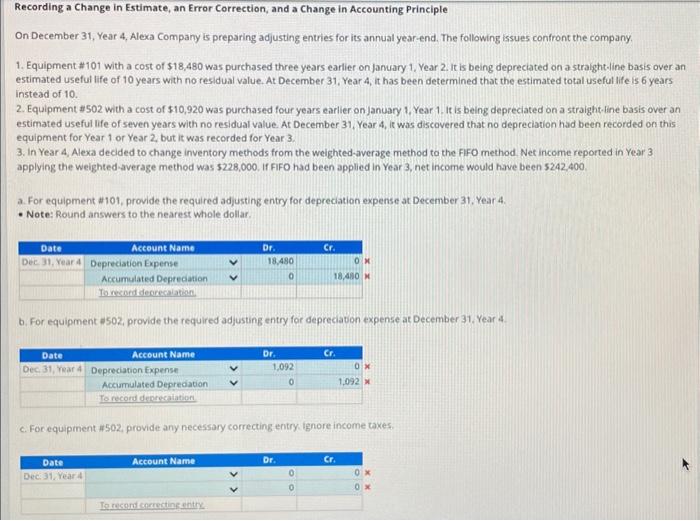

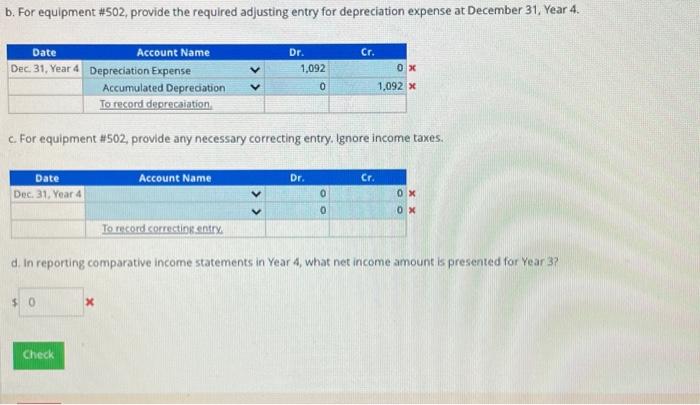

Recording a Change in Estimate, an Error Correction, and a Change in Accounting Principle On December 31, Year 4, Alexa Company is preparing adjusting entries for its annual year-end. The following issues confront the company. 1. Equipment #101 with a cost of $18,480 was purchased three years earlier on january 1 , Year 2 it is being depreciated on a straight-line basis over an estimated useful life of 10 years with no residual value. At December 31 , Year 4 , it has been determined that the estimated total useful life is 6 years Instead of 10. 2. Equipment $502 with a cost of $10,920 was purchased four years earlier on january 1, Year 1 , It is being depreciated on a straight-fine basis over an estimated useful life of seven years with no residual value. At December 31, Year 4 , it was discovered that no depreciation had been recorded on this equipment for Year 1 or Year 2 , but it was recorded for Year 3. 3. In Year 4, Alexa decided to change inventory methods from the weighted-average method to the fifo method. Net income reported in Year 3 applying the weighted-average method was $228,000. If FIFO had been applied in Year 3 , net income would have been $242,400. a. For equipment #101, provide the required adjusting entry for depreciation expense at December 31 , Year 4. - Note: Round answers to the nearest whole dollar. b. For equipment $502, provide the required adjusting entry for depreciaton expense at December 31 , Year 4. c. For equipment $502, provide any necessary correcting entry ignore income taxes. b. For equipment \#502, provide the required adjusting entry for depreciation expense at December 31 , Year 4 . c. For equipment \#502, provide any necessary correcting entry. Ignore income taxes. d. In reporting comparative income statements in Year 4 , what net income amount is presented for Year 3 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Principles Volume 1

Authors: Jerry J. Weygandt, Donald E. Kieso, Paul D. Kimmel, Barbara Trenholm, Valerie Warren, Lori Novak

9th Canadian Edition

978-1119786818, 1119786819