Answered step by step

Verified Expert Solution

Question

1 Approved Answer

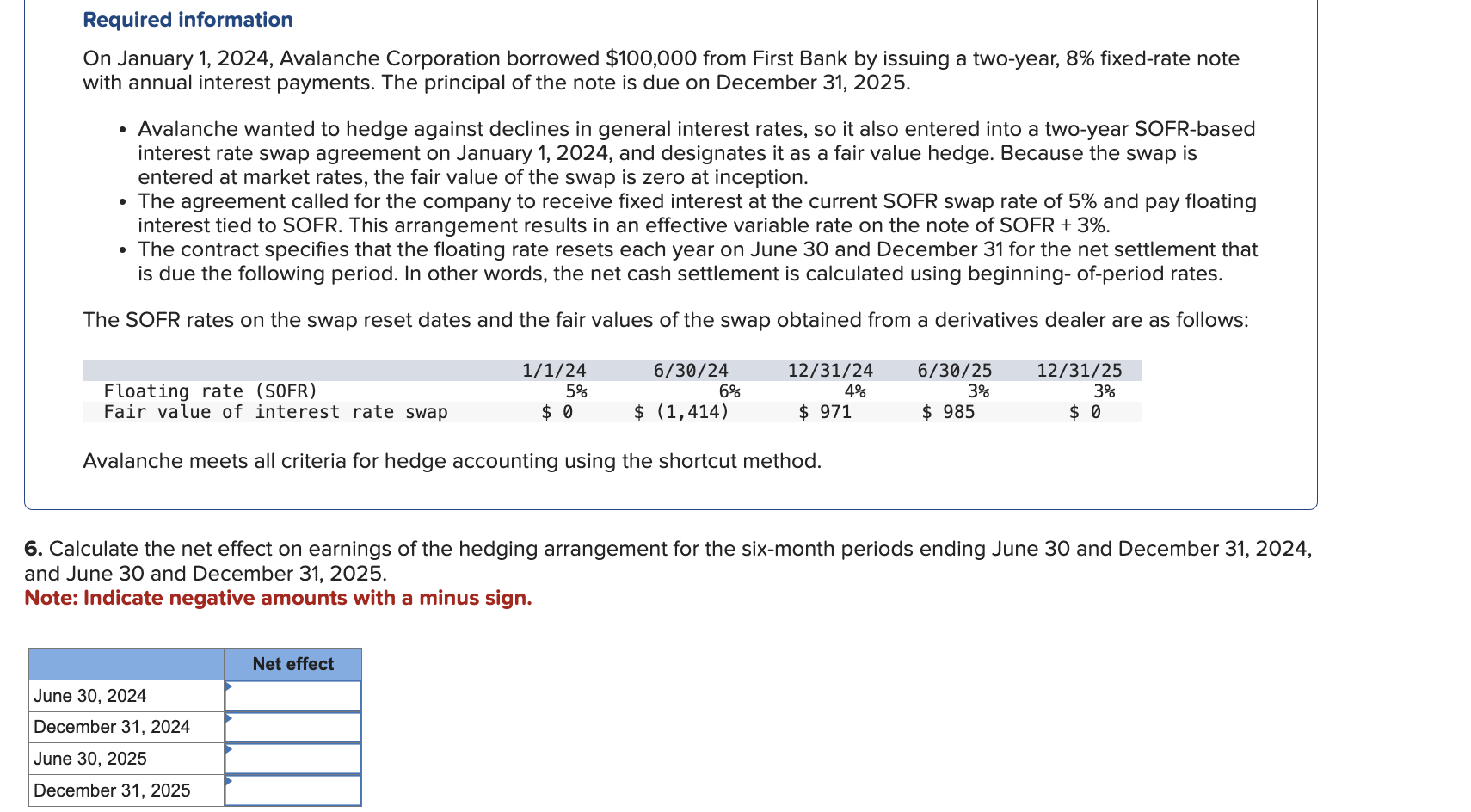

Required information On January 1 , 2 0 2 4 , Avalanche Corporation borrowed $ 1 0 0 , 0 0 0 from First Bank

Required information

On January Avalanche Corporation borrowed $ from First Bank by issuing a twoyear, fixedrate note

with annual interest payments. The principal of the note is due on December

Avalanche wanted to hedge against declines in general interest rates, so it also entered into a twoyear SOFRbased

interest rate swap agreement on January and designates it as a fair value hedge. Because the swap is

entered at market rates, the fair value of the swap is zero at inception.

The agreement called for the company to receive fixed interest at the current SOFR swap rate of and pay floating

interest tied to SOFR. This arrangement results in an effective variable rate on the note of SOFR

The contract specifies that the floating rate resets each year on June and December for the net settlement that

is due the following period. In other words, the net cash settlement is calculated using beginning ofperiod rates.

The SOFR rates on the swap reset dates and the fair values of the swap obtained from a derivatives dealer are as follows:

Avalanche meets all criteria for hedge accounting using the shortcut method.

Calculate the net effect on earnings of the hedging arrangement for the sixmonth periods ending June and December

and June and December

Note: Indicate negative amounts with a minus sign.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Geography Of Finance

Authors: Gordon L. Clark, Darius Wójcik

1st Edition

0199213364, 978-0199213368