Answered step by step

Verified Expert Solution

Question

1 Approved Answer

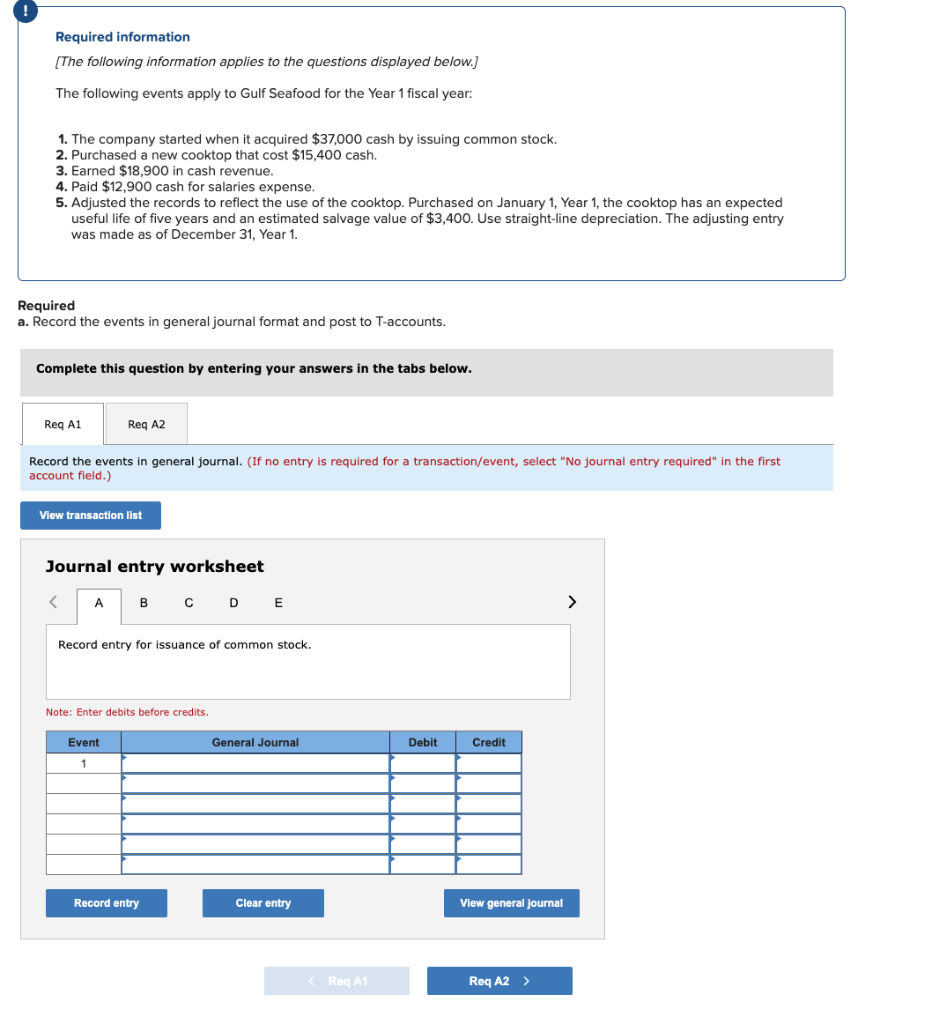

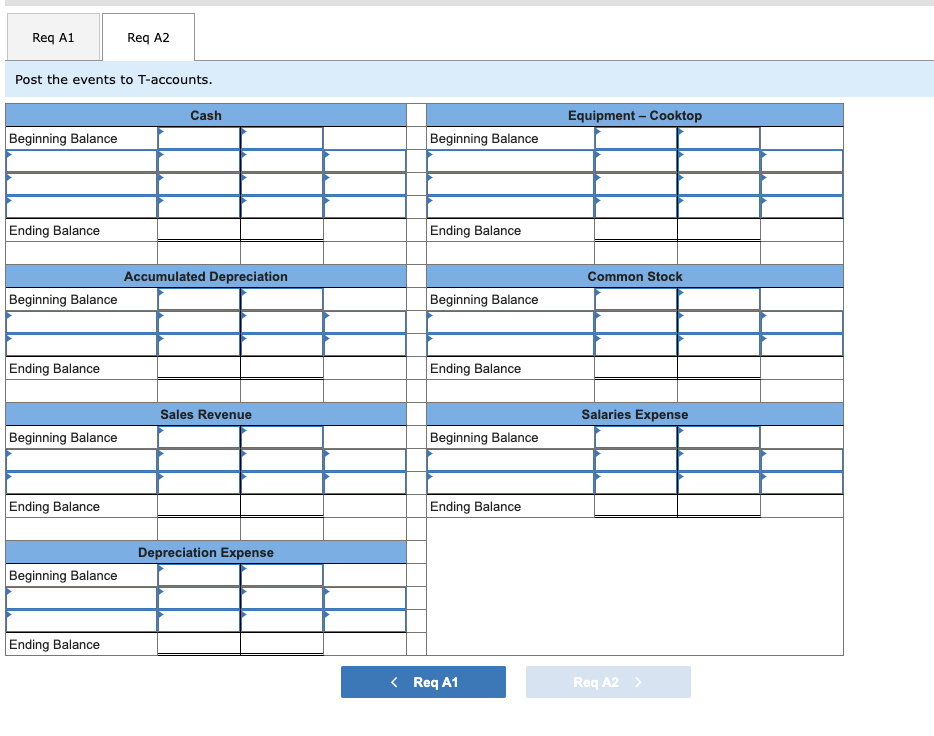

Required information [The following information applies to the questions displayed below.] The following events apply to Gulf Seafood for the Year 1 fiscal year: 1.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Security Audit And Review Toolkit The Modern Toolkit For Security And Risk Professionals To Grow Their Business And For The Business Owners.

Authors: L Burke Files, Gamal Newry, Ibrahim Yeku

1st Edition

1674831315, 978-1674831312