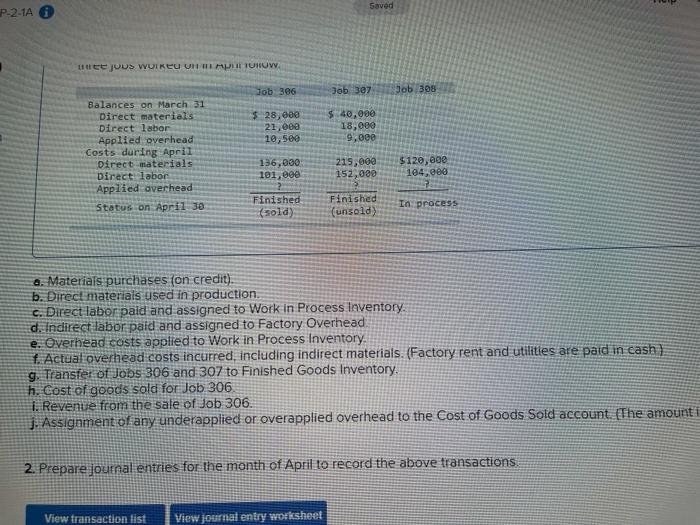

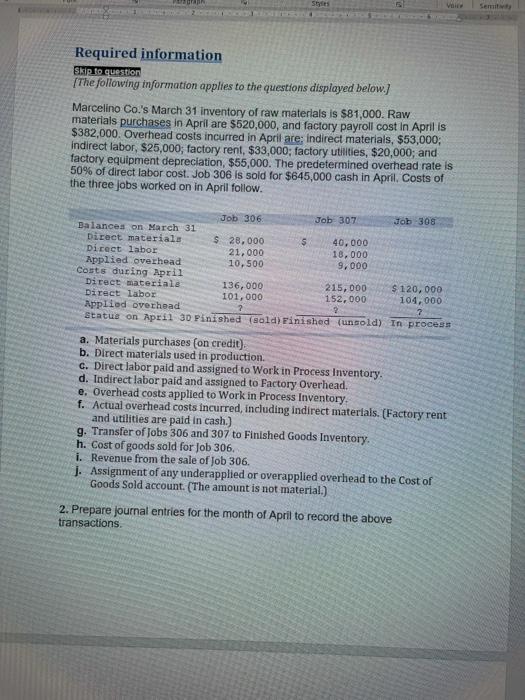

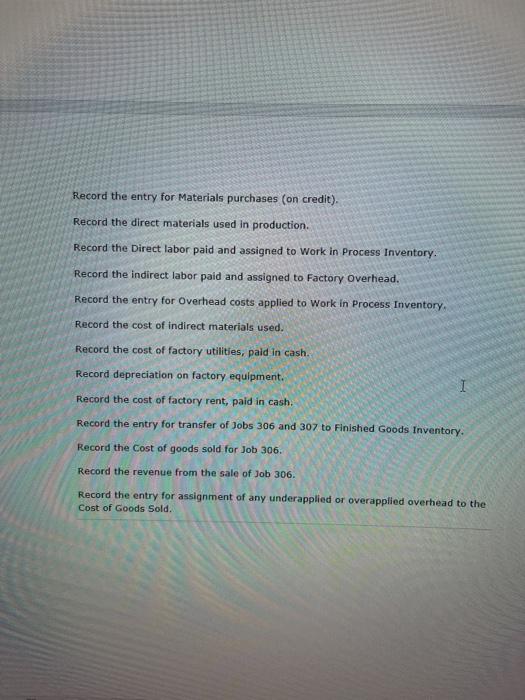

Saved P-2-1A | EE DU DIEU || ||| || Job 386 Job. 307 Job 308 $ 28,000 21,000 10,5ee $ 40,000 18,000 9,000 Balances on March 31 Direct materials Direct labor Applied overhead Costs during April Direct materials Direct labor Applied averhead Status on April 30 136,000 101,000 215,000 152,000 $120,000 184,900 Finished (sold) Finished (unsold) In process a. Materials purchases (on credit). b. Direct materials used in production, c. Direct labor paid and assigned to Work in Process Inventory d. Indirect labor paid and assigned to Factory Overhead e. Overhead costs applied to Work in Process Inventory 1. Actual overhead costs incurred, including indirect materials. (Factory rent and utilities are paid in cash) g. Transfer of Jobs 306 and 307 to Finished Goods Inventory. h. Cost of goods sold for Job 306 1. Revenue from the sale of Job 306. 3. Assignment of any underapplied or overapplied overhead to the Cost of Goods Sold account. (The amount i 2. Prepare Journal entries for the month of April to record the above transactions. View transaction list View journal entry worksheet S Required information Skip to question [The following information applies to the questions displayed below.) Marcelino Co.'s March 31 Inventory of raw materials is $81,000. Raw materials purchases in April are $520,000, and factory payroll cost In Aprilis $382,000. Overhead costs incurred in April are: indirect materials, $53,000; indirect labor, $25,000; factory rent, $33,000; factory utilities, $20,000; and factory equipment depreciation, $55,000. The predetermined overhead rate is 50% of direct labor cost. Job 306 is sold for $645,000 cash in April. Costs of the three jobs worked on in April follow. Job 306 Job 307 Job 308 Balances on March 31 Direct materials $28.000 40,000 Direct labor 21,000 18,000 Applied overhead 10,500 9,000 Costs during April Direct materials 136,000 215,000 $ 120,000 Direct labor 101,000 152.000 104,000 Applied overhead status on April 30 Pinished (old) Finished (unsold) In process a. Materials purchases (on credit) b. Direct materials used in production. 6. Direct labor paid and assigned to Work in Process Inventory. d. Indirect labor paid and assigned to Factory Overhead. e. Overhead costs applied to Work in Process Inventory. f. Actual overhead costs incurred, including indirect materials. (Factory rent and utilities are paid in cash.) g. Transfer of Jobs 306 and 307 to Finished Goods Inventory. h. Cost of goods sold for Job 306. i. Revenue from the sale of Job 306. 1. Assignment of any underapplied or overapplied overhead to the Cost of Goods Sold account. (The amount is not material.) 2. Prepare journal entries for the month of April to record the above transactions Record the entry for Materials purchases (on credit). Record the direct materials used in production. Record the Direct labor paid and assigned to work in Process Inventory Record the indirect labor paid and assigned to Factory Overhead. Record the entry for Overhead costs applied to Work in Process Inventory. Record the cost of indirect materials used. Record the cost of factory utilities, paid in cash. Record depreciation on factory equipment. Record the cost of factory rent, paid in cash. Record the entry for transfer of Jobs 306 and 307 to Finished Goods Inventory. Record the cost of goods sold for Job 306. Record the revenue from the sale of Job 306. Record the entry for assignment of any underapplied or overapplied overhead to the Cost of Goods Sold