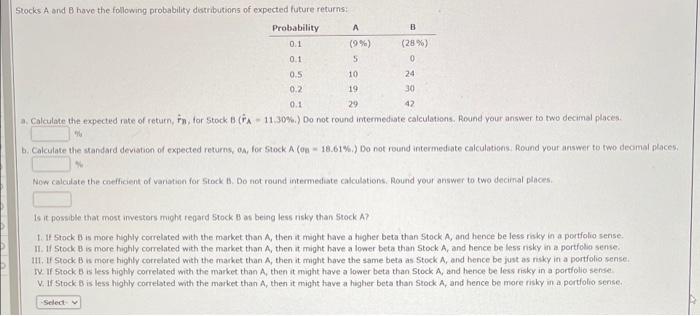

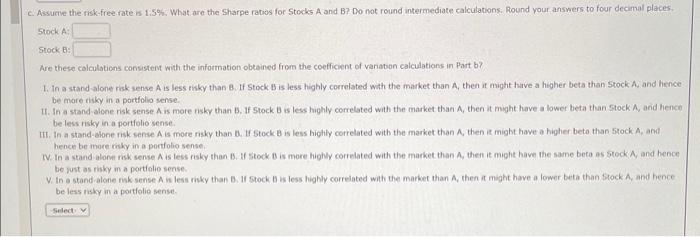

Stocks A and B have the following probability distributions of expected future returns: a, Calculate the expected rate of return, rn, for Stock B(rA=11,30%. Do not round intermedate calculations. Round your answer to two decimal places. Tila. b. Calculate the sandard deviation of expected returns, 0A, for Stock A(0a=18.61 \%. ) Do not round intermediate calculations. Rovind your answer to two decimal plac 4 Non calculate the corfificient of variation for Stock. B. Do fot round intermediate calculations. Round your answer to two decimal places. Is it possible that most iwestors micht reqard 5 tock B at being less nisky than 5 tock A ? 1. If Stock B is moce highly correlated with the market than A, then it might have a higher beta than 5 tock A, and hence be less riaky in a portfolio sense. II. if 5 tock B is more highly correlated with the market than A, then it might have a lower beta than 5 tock A, and hence be less risky in a portfolin sense. 111. If Stock B is more highly correlated with the market than A, then it might have the same beta as 5 tock A, and hence be just as nisky in a portfolio sense. W. If stock B is less highty correlated with the market than A, then it might have a lower beta than 5 tock A, and hence be less risky in a partfolio sense. W. If Stack 8 is less highly correlated with the market than A, then it might have a higher beta than stock A, and heace be more risky in a portfolio sense. Assume the risk-free rate is 1.5%. What are the Sharpe ratoos for Stocks A and B? Do not round intermediate calculations. Round your answers to four decimal places. srock A: stock B: Are these colculaticns consistent with the information obtained from the coefficient of variabon calculations in Part b? 1. In a stand alone risk sense A is less rikky than B. If Stock B is less highly correlated with the market than A, then it might hirve a higher beta than Stock A, and hence be more risky in a portfolio sense. U. In a stand-alone risk sense A is more risky than B. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, anid hence be less risky in a portfolio sense: III. If a stand-alone nisk sense A is more risky than D. If Stock B is less highly correlated with the market than A, then it might have a higher beta than 5 fock A, and hence te thore wisky in a portolio sense. TV. In a stand alont risk sense A is less risky than B.16 stock. 8 is moce highty correlated with the market than A, then it might have the same beta as stock A, and hence be wost as risky in a portiolio sense. V. In a stand-alone risk sense A is less risky than B. If stock B is less highly correlated with the market than A, then it might have a lower beta than 5 tock A, and hence. be less risky in a portfolio sense