Answered step by step

Verified Expert Solution

Question

1 Approved Answer

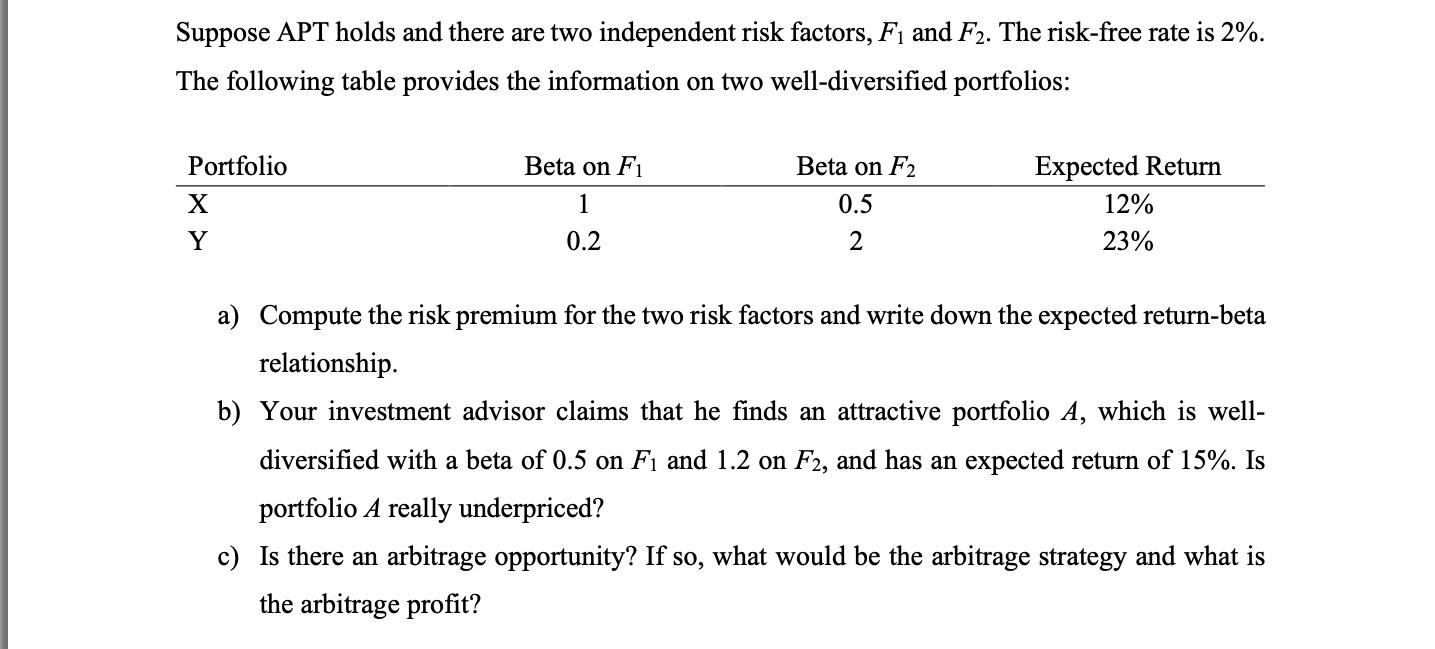

Suppose APT holds and there are two independent risk factors, F1 and F2. The risk-free rate is 2%. The following table provides the information

Suppose APT holds and there are two independent risk factors, F1 and F2. The risk-free rate is 2%. The following table provides the information on two well-diversified portfolios: Portfolio X Y Beta on Fi 1 0.2 Beta on F2 0.5 2 Expected Return 12% 23% a) Compute the risk premium for the two risk factors and write down the expected return-beta relationship. b) Your investment advisor claims that he finds an attractive portfolio A, which is well- diversified with a beta of 0.5 on F1 and 1.2 on F2, and has an expected return of 15%. Is portfolio A really underpriced? c) Is there an arbitrage opportunity? If so, what would be the arbitrage strategy and what is the arbitrage profit?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703