Question

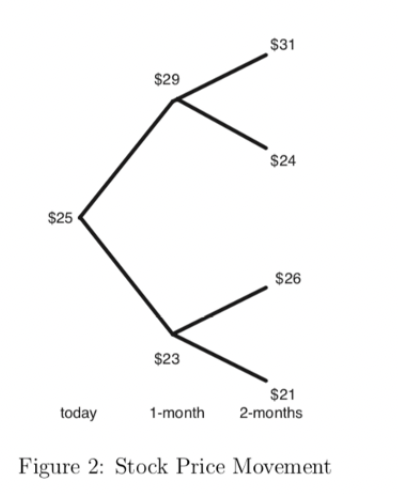

Suppose the interest rate is fixed at 1% per month. A particular stock follows the price movement below: 1 (a) What is the price of

Suppose the interest rate is fixed at 1% per month. A particular stock follows the price movement below: 1

(a) What is the price of a European put option with maturity two months, and strike of $26? To answer, construct and solve the replicating portfolio problem with position a in shares and b in bonds.

(b) What is the price of an American put option with maturity two months, and strike of $26? Again, construct and solve the replicating portfolio problem with position a in shares and b in bonds. Comment on the difference between the value of the two options, and its decomposition.

r 1gure : stock rrice ivovementStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Basic Finance An Introduction to Financial Institutions Investments and Management

Authors: Herbert B. Mayo

10th edition

1111820635, 978-1111820633