Question

Suppose the market for good X is competitive. Assume there are 1000 firms in this market and all these firms are identical. Table 1. Below,

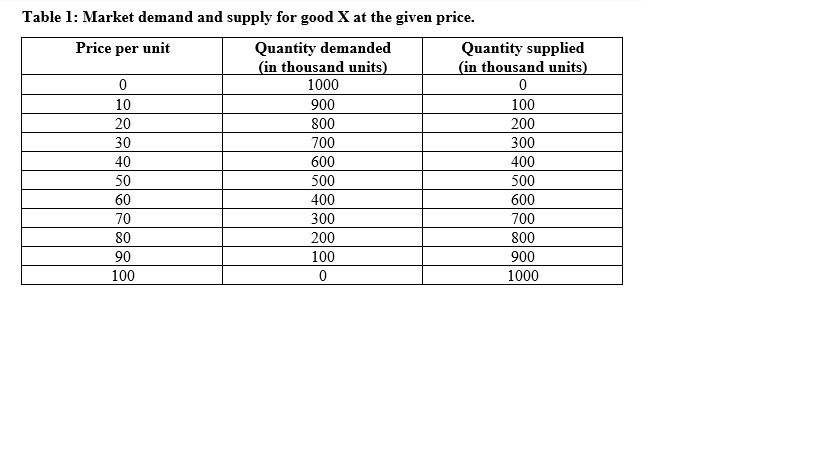

Suppose the market for good X is competitive. Assume there are 1000 firms in this market and all these firms are identical. Table 1. Below, provides the market demand and supply for good X (in thousand units). Suppose the firm's objective is to maximize profit and its average total cost for producing the profit-maximizing quantity is $30.

(a) Use the given information below, to draw the diagrams to represent the market equilibrium and firm equilibrium. Label the equilibrium price and quantity of the market and the equilibrium quantity of the firm.

(b) Determine and describe the initial market equilibrium price and quantity, consumer surplus, producer surplus, and total surplus.

(c) Determine and describe the firm's equilibrium quantity and profit. Can this firm continue to make the profit in the long run? Explain.

(d) Assume a firm, in the long run, produces 400 units and the firm's minimum average total cost is $20. What is the new market equilibrium price and quantity and how many new firms have entered the market? Assume the new firms and existing firms are identical.

(e)Suppose the government decided to set a price ceiling of $20 per unit. Use your diagram from part(a) to determine and explain how the price policy affects the market, consumers, and producers, and market efficiency.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Economics A Problem-Solving Approach

Authors: Luke M. Froeb, Brain T. Mccann

2nd Edition

B00BTM8FK0