Answered step by step

Verified Expert Solution

Question

1 Approved Answer

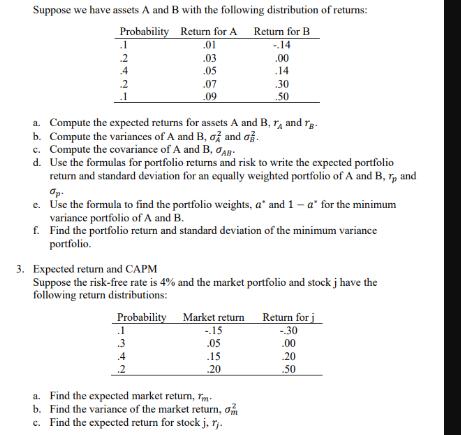

Suppose we have assets A and B with the following distribution of returns: Probability Return for A Return for B .1 .01 -14 .2

Suppose we have assets A and B with the following distribution of returns: Probability Return for A Return for B .1 .01 -14 .2 .03 .00 .4 .05 .14 .2 .07 .30 .1 .09 .50 a. Compute the expected returns for assets A and B, r and rg. b. Compute the variances of A and B, o and o c. Compute the covariance of A and B, AB d. Use the formulas for portfolio returns and risk to write the expected portfolio return and standard deviation for an equally weighted portfolio of A and B, Tp and Op- e. Use the formula to find the portfolio weights, a" and 1-a" for the minimum variance portfolio of A and B. f. Find the portfolio return and standard deviation of the minimum variance portfolio. 3. Expected return and CAPM Suppose the risk-free rate is 4% and the market portfolio and stock j have the following return distributions: Probability Market return Return for j 1 -.15 -.30 3 .05 .00 4 .15 -20 .2 20 .50 a. Find the expected market return, T- b. Find the variance of the market return, o c. Find the expected return for stock j. rj. d. Find the covariance of j and the market, jm. e. What is J's beta?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Basic Statistics

Authors: Charles Henry Brase, Corrinne Pellillo Brase

6th Edition

978-1133525097, 1133525091, 1111827028, 978-1133110316, 1133110312, 978-1111827021