Question

The price of a stock evolves as in the following two-steps binomial tree: Let X be a European call option with maturity at tick-time 2

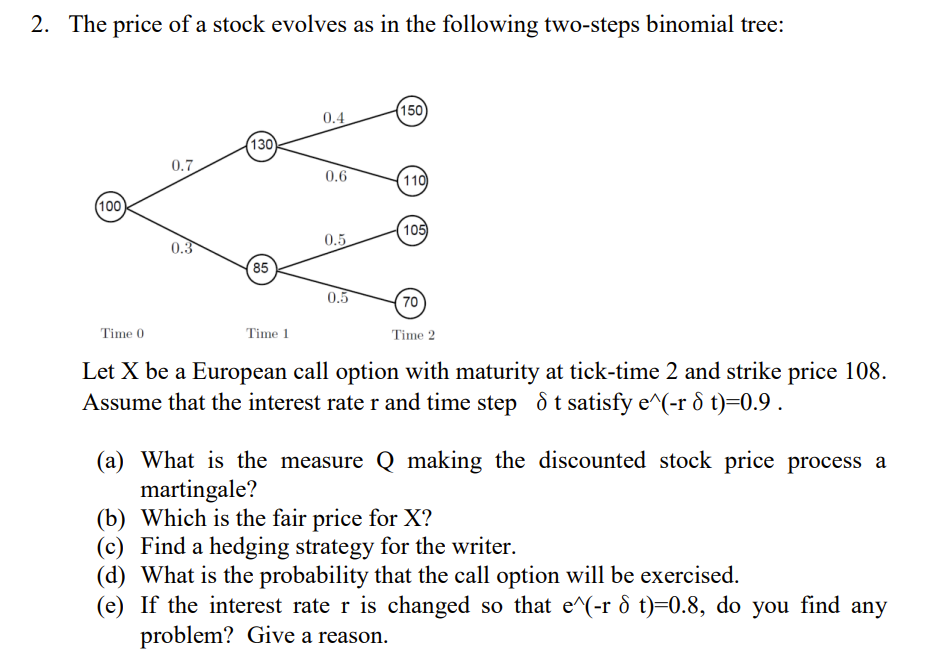

The price of a stock evolves as in the following two-steps binomial tree:

Let X be a European call option with maturity at tick-time 2 and strike price 108. Assume that the interest rate r and time step t satisfy e^(-rt)=0.9 .

(a) What is the measure Q making the discounted stock price process a martingale? (b) Which is the fair price for X? (c) Find a hedging strategy for the writer. (d) What is the probability that the call option will be exercised.

(e) If the interest rate r is changed so that e^(-rt)=0.8, do you find any problem? Give a reason.

If no answering Q5 doesn't matter, first 4 problems pls

2. The price of a stock evolves as in the following two-steps binomial tree: Let X be a European call option with maturity at tick-time 2 and strike price 108 . Assume that the interest rate r and time step t satisfy e(rt)=0.9. (a) What is the measure Q making the discounted stock price process a martingale? (b) Which is the fair price for X ? (c) Find a hedging strategy for the writer. (d) What is the probability that the call option will be exercised. (e) If the interest rate r is changed so that e(rt)=0.8, do you find any problem? Give a reason. 2. The price of a stock evolves as in the following two-steps binomial tree: Let X be a European call option with maturity at tick-time 2 and strike price 108 . Assume that the interest rate r and time step t satisfy e(rt)=0.9. (a) What is the measure Q making the discounted stock price process a martingale? (b) Which is the fair price for X ? (c) Find a hedging strategy for the writer. (d) What is the probability that the call option will be exercised. (e) If the interest rate r is changed so that e(rt)=0.8, do you find any problem? Give a reason

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Sharing Finance

Authors: Bakkali Mirakhor, Saad Abbas

1st Edition

3110590468, 978-3110590463