Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Use the following image(IF NEEDED) to answer the question below. QUESTION: The preparation of the trial balance occurs after to the preparation of the financial

Use the following image(IF NEEDED) to answer the question below.

QUESTION:

The preparation of the trial balance occurs after to the preparation of the financial statements.

o True

o False

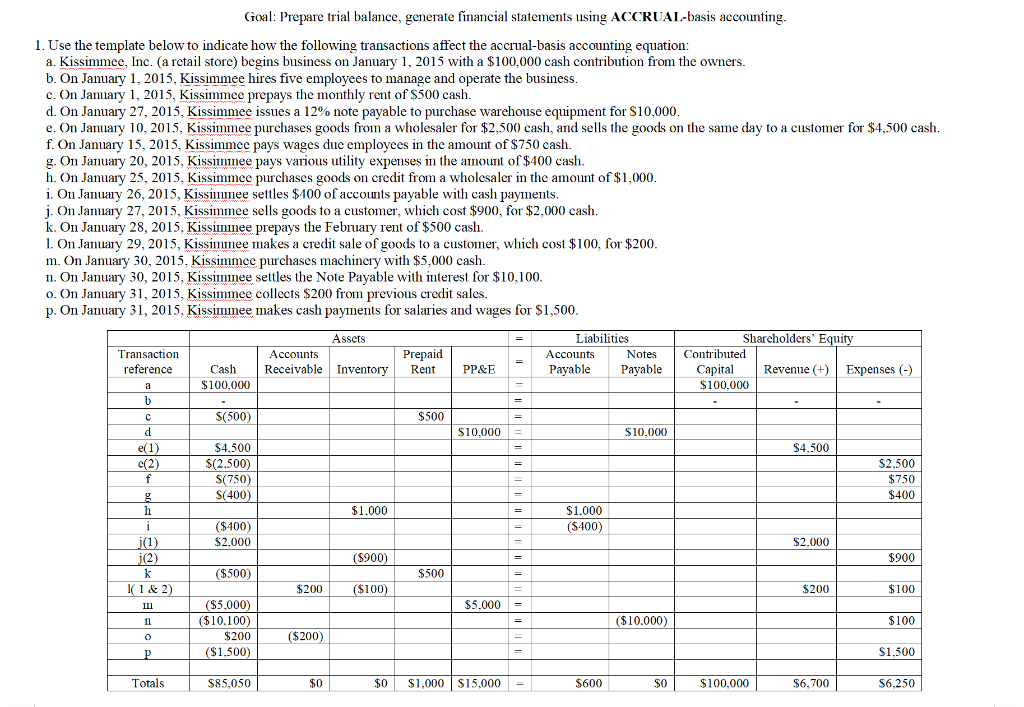

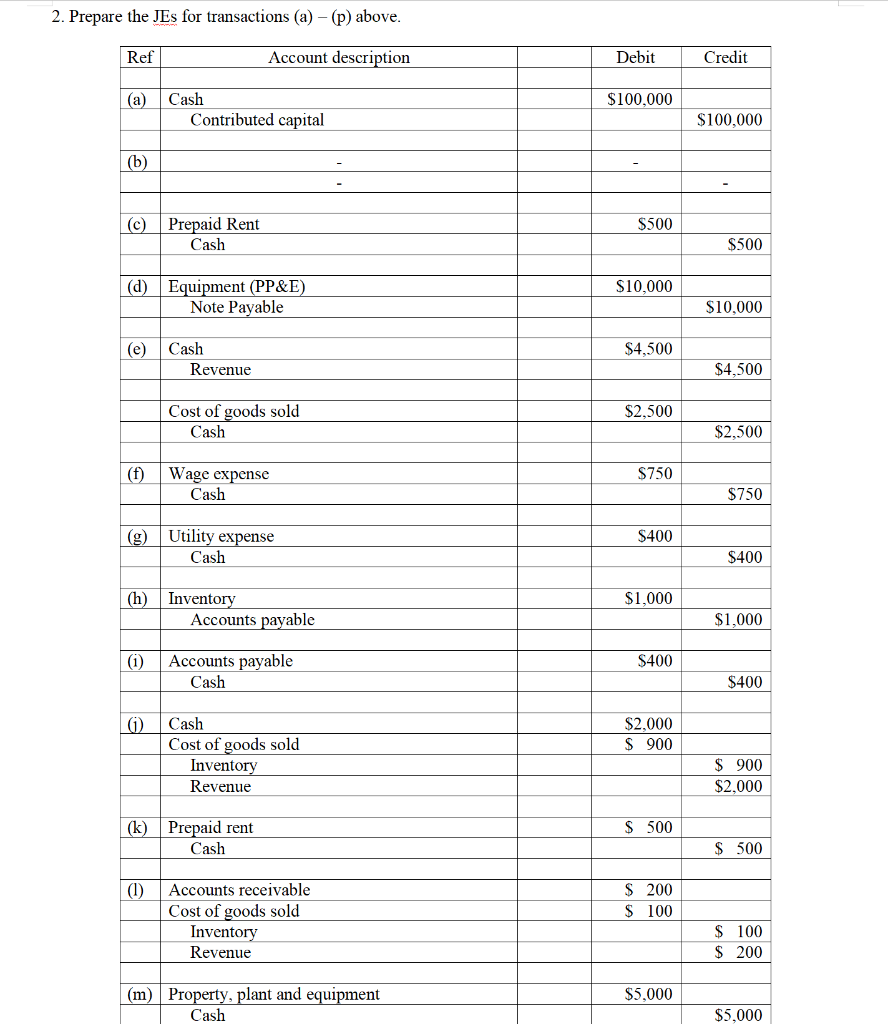

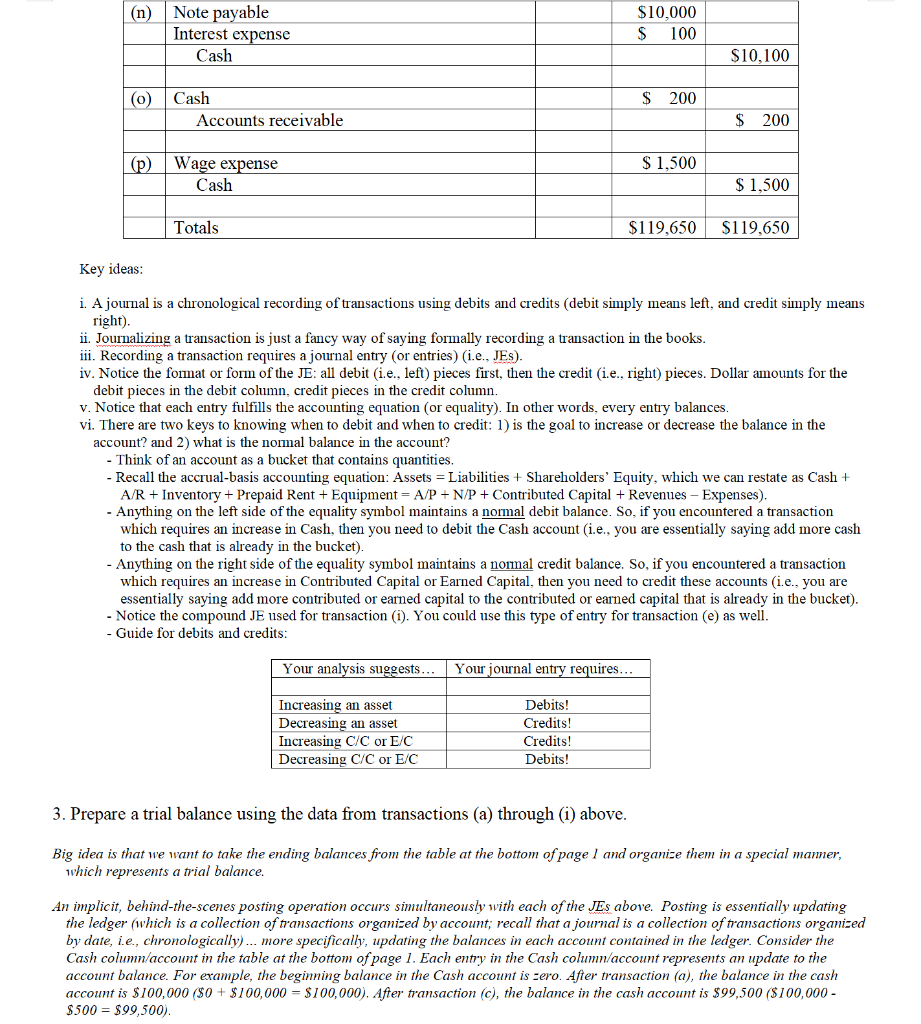

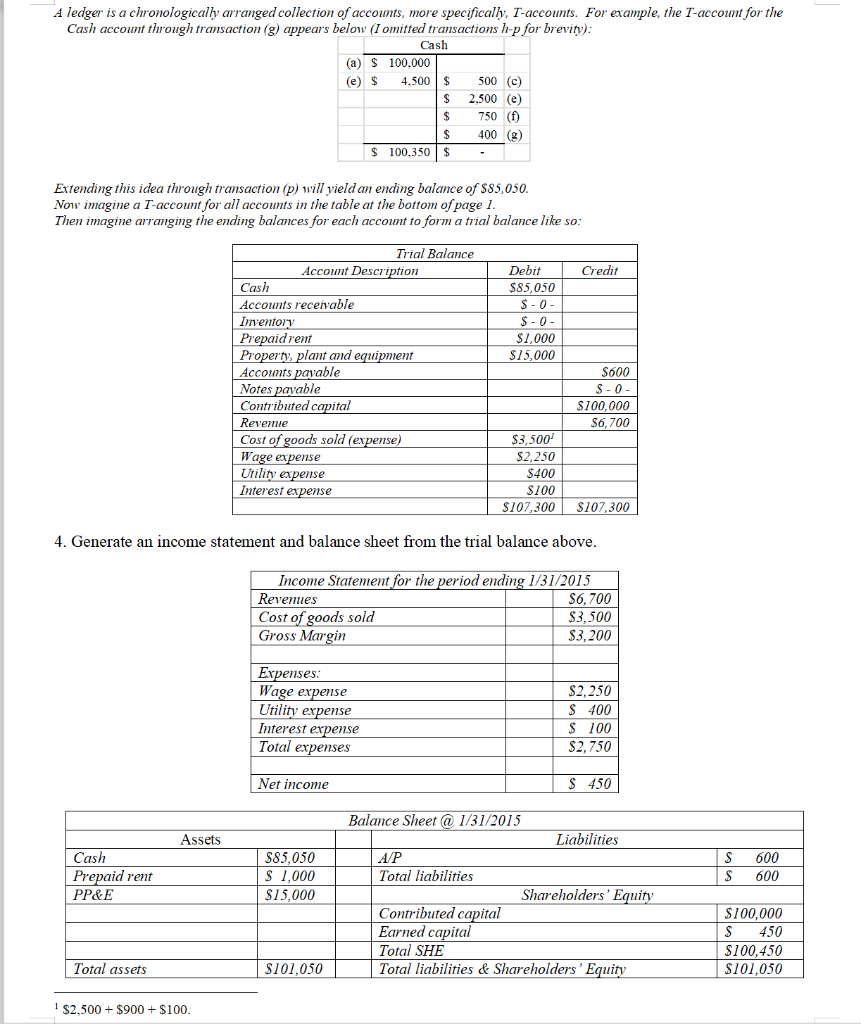

g Goal: Prepare trial balance, generate financial statements using ACCRUAL-basis accounting. 1. Use the template below to indicate how the following transactions affect the accrual-basis accounting equation: a. Kissimmee, Inc. (a retail store) begins business on January 1, 2015 with a $100,000 cash contribution from the owners. b. On January 1, 2015, Kissimmee hires five employees to manage and operate the business. c. On January 1, 2015, Kissimmee prepays the monthly rent of $500 cash. d. On January 27, 2015, Kissimmee issues a 12% note payable to purchase warehouse equipment for $10,000. e. On January 10, 2015, Kissimmee purchases goods from a wholesaler for $2,500 cash, and sells the goods on the same day to a customer for $4,500 cash. f. On January 15, 2015, Kissimmee pays wages due employees in the amount of $750 cash. On January 20, 2015, Kissimmee pays various utility expenses in the amount of $400 cash. h. On January 25, 2015, Kissimmee purchases goods on credit from a wholesaler in the amount of $1,000. i. On January 26, 2015, Kissiminee settles $400 of accounts payable with cash payinents. j. On January 27, 2015, Kissimmee sells goods to a customer, which cost $900, for $2,000 cash. k. On January 28, 2015, Kissiminee prepays the February rent of $500 cash. 1. On January 29, 2015, Kissimmee makes a credit sale of goods to a customer, which cost $100, for $200. m. On January 30, 2015, Kissimmee purchases machinery with $5,000 cash. 11. On January 30, 2015, Kissiminee settles the Note Payable with interest for $10,100. o. On January 31, 2015, Kissimmee collects $200 from previous credit sales. p. On January 31, 2015, Kissiminee makes cash payinents for salaries and wages for $1,500. Liabilities Shareholders' Equity Transaction Accounts Prepaid Accounts Notes Contributed reference Cash Receivable Inventory Rent Payable Payable Capital Revenue (+) Expenses (-) $100,000 $100,000 Assets PP&E S(500) $500 a h D d e(1) e(2) f $10,000 $10,000 $4,500 = $4,500 $(2,500) S(750) S(400) $2,500 $750 $400 $1.000 $1.000 ($400) ($400) $2,000 $2,000 g h i j(1) j (2) k 1(1&2) III ($900) $900 ($500) $500 $200 ($100) $200 $100 $5,000 ($5.000) ($10.100) 11 ($10.000) $100 $200 ($1.500) ($200) $1,500 Totals $85.050 $0 $0 $1.000 $15,000 $600 SO $100.000 $6,700 S6,250 2. Prepare the JEs for transactions (a) - (p) above. Ref Account description Debit Credit (a) $100.000 Cash Contributed capital $100,000 (b) $500 (c) Prepaid Rent Cash $500 $10,000 (d) Equipment (PP&E) Note Payable $10.000 (e) $4,500 Cash Revenue $4,500 $2,500 Cost of goods sold Cash $2,500 (f) $750 Wage expense Cash $750 (g) $400 Utility expense Cash $400 (h) $1,000 Inventory Accounts payable $1,000 (1) $400 Accounts payable Cash $400 6) $2,000 $ 900 Cash Cost of goods sold Inventory Revenue $ 900 $2,000 (k) Prepaid rent Cash $ 500 $ 500 (1) Accounts receivable Cost of goods sold Inventory Revenue $ 200 $ 100 $ 100 $ 200 $5,000 (m) Property, plant and equipment Cash $5.000 (n) Note payable Interest expense Cash $10,000 $ 100 $10,100 o) $ 200 Cash Accounts receivable $ 200 (p) $ 1.500 Wage expense Cash $ 1,500 Totals $119,650 $119,650 Key ideas: i. A journal is a chronological recording of transactions using debits and credits (debit simply means left, and credit simply means right). ii. Journalizing a transaction is just a fancy way of saying formally recording a transaction in the books. iii. Recording a transaction requires a journal entry (or entries) (i.e., JES). iv. Notice the format or form of the JE: all debit (i.e., left) pieces first, then the credit (i.e., right) pieces. Dollar amounts for the debit pieces in the debit column, credit pieces in the credit column. v. Notice that each entry fulfills the accounting equation (or equality). In other words, every entry balances. vi. There are two keys to knowing when to debit and when to credit: 1) is the goal to increase or decrease the balance in the account? and 2) what is the normal balance in the account? - Think of an account as a bucket that contains quantities. - Recall the accrual-basis accounting equation: Assets = Liabilities + Shareholders' Equity, which we can restate as Cash + A/R + Inventory + Prepaid Rent + Equipment = A/P + N/P + Contributed Capital + Revenues - Expenses). - Anything on the left side of the equality symbol maintains a normal debit balance. So, if you encountered a transaction which requires an increase in Cash, then you need to debit the Cash account (i.e., you are essentially saying add more cash to the cash that is already in the bucket). - Anything on the right side of the equality symbol maintains a normal credit balance. So, if you encountered a transaction which requires an increase in Contributed Capital or Earned Capital, then you need to credit these accounts (i.e., you are essentially saying add more contributed or earned capital to the contributed or earned capital that is already in the bucket). - Notice the compound JE used for transaction (1). You could use this type of entry for transaction (e) as well. - Guide for debits and credits: Your analysis suggests. Your journal entry requires... Increasing an asset Decreasing an asset Increasing C/C or E/C Decreasing C/C or E/C Debits! Credits! Credits! Debits! 3. Prepare a trial balance using the data from transactions (a) through (1) above. Big idea is that we want to take the ending balances from the table at the bottom of page 1 and organize them in a special mamer, which represents a trial balance. An implicit, behind-the-scenes posting operation occurs simultaneously with each of the JEs above. Posting is essentially updating the ledger (which is a collection of transactions organized by account; recall that a journal is a collection of transactions organized by date, i.e., chronologically)... more specifically, updating the balances in each account contained in the ledger. Consider the Cash column/account in the table at the bottom of page 1. Each entry in the Cash column/account represents an update to the account balance. For example, the beginning balance in the Cash account is zero. After transaction (a), the balance in the cash account is $100,000 ($0+ $100,000 = $100,000). After transaction (c), the balance in the cash account is $99,500 ($100,000 - $500 = $99,500). A ledger is a chronologically arranged collection of accounts, more specifically, T-accounts. For example, the T-account for the Cash account through transaction (g) appears below (I omitted transactions h-p for brevity): Cash (a) $ 100.000 (e) $ 4.500 $ 500 (c) 2,500 (e) 750 (f) $ 400 (8) $ 100,350 $ $ $ Extending this idea through transaction (p) will yield an ending balance of $85,050. Now imagine a T-account for all accounts in the table at the bottom of page 1. Then imagine arranging the ending balances for each account to form a trial balance like so: Credit Debit $85,050 S-0 S-0 $1,000 $75,000 Trial Balance Account Description Cash Accounts receivable Inventory Prepaid rent Property, plant and equipment Accounts payable Notes payable Contributed capital Reveme Cost of goods sold (expense) Wage expense Utility expense Interest expense $600 S-0- $100.000 $6,700 $3,500 $2,250 $400 $100 $107.300 $107,300 4. Generate an income statement and balance sheet from the trial balance above. Income Statement for the period ending 1/31/2015 Revenues S6,700 Cost of goods sold $3,500 Gross Margin $3,200 Expenses Wage expense Utility expense Interest expense Total expenses $2,250 S 400 $ 100 $2,750 Net income $ 450 Assets Cash Prepaid rent PP&E $85,050 $1,000 $75,000 $ S 600 600 Balance Sheet @ 1/31/2015 Liabilities AP Total liabilities Shareholders' Equity Contributed capital Earned capital Total SHE Total liabilities & Shareholders' Equity $100,000 S 450 $100,450 $101,050 Total assets $101,050 $2,500 + $900 + $100

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Final Audit In Pursuit Of Nazi War Booty Compulsively Readable And Superbly Narrated Dlied With Love Suspense Insight Wisdom And Dry Humor

Authors: Carnie Matisonn

1st Edition

1452094845, 978-1452094847