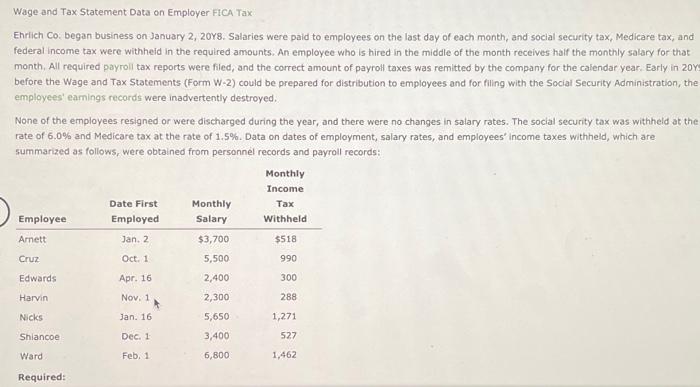

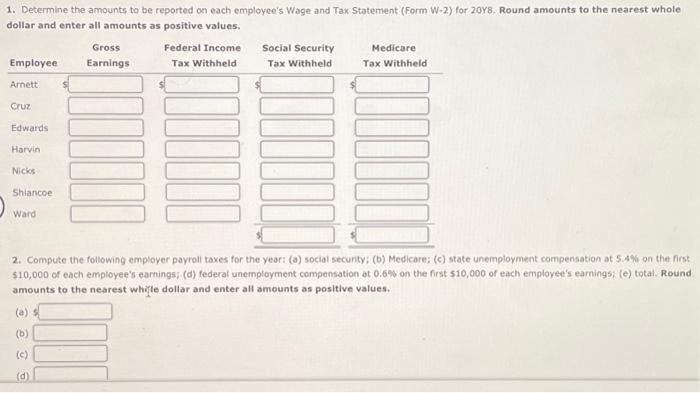

Wage and Tax Statement Data on Employer FiCA Tax Ehrlich Co. began business on January 2, 20Y8. Salaries were paid to employees on the last day of each month, and social security tax, Medicare tax, and federal income tax were withheid in the required amounts. An employee who is hired in the middle of the month receives haif the monthly salary for that month, All required payroll tax reports were filed, and the correct amount of payroll taxes was remitted by the company for the calendar year. Early in 20y before the Wage and Tax Statements (Form W-2) could be prepared for distribution to employees and for filing with the Social Security Administration, the employees' eamings records were inadvertently destroyed. None of the employees resigned or were discharged during the year, and there were no changes in salary rates. The social security tax was withheld at the rate of 6.0% and Medicare tax at the rate of 1.5%. Data on dates of employment, salary rates, and employees' income taxes withheld, which are summarized as follows, were obtained from personnel records and payroll records: 1. Determine the amounts to be reported on each employee's Wage and Tax Statement (Form W-2) for 20Y8. Round amounts to the nearest whole dollar and enter all amounts as positive values. 2. Compute the following employer payroll toxes for the year: (a) social security; (b) Medicare; (c) state unemployment compensation at 5 .4\% on the first $10,000 of each employee's earnings; (d) federal unemployment compensation at 0.6% on the first $10,000 of each employee's earnings; (e) total. Round amounts to the nearest whille dollar and enter all amounts as positive values. (a) 9 (b) (c) (d) Wage and Tax Statement Data on Employer FiCA Tax Ehrlich Co. began business on January 2, 20Y8. Salaries were paid to employees on the last day of each month, and social security tax, Medicare tax, and federal income tax were withheid in the required amounts. An employee who is hired in the middle of the month receives haif the monthly salary for that month, All required payroll tax reports were filed, and the correct amount of payroll taxes was remitted by the company for the calendar year. Early in 20y before the Wage and Tax Statements (Form W-2) could be prepared for distribution to employees and for filing with the Social Security Administration, the employees' eamings records were inadvertently destroyed. None of the employees resigned or were discharged during the year, and there were no changes in salary rates. The social security tax was withheld at the rate of 6.0% and Medicare tax at the rate of 1.5%. Data on dates of employment, salary rates, and employees' income taxes withheld, which are summarized as follows, were obtained from personnel records and payroll records: 1. Determine the amounts to be reported on each employee's Wage and Tax Statement (Form W-2) for 20Y8. Round amounts to the nearest whole dollar and enter all amounts as positive values. 2. Compute the following employer payroll toxes for the year: (a) social security; (b) Medicare; (c) state unemployment compensation at 5 .4\% on the first $10,000 of each employee's earnings; (d) federal unemployment compensation at 0.6% on the first $10,000 of each employee's earnings; (e) total. Round amounts to the nearest whille dollar and enter all amounts as positive values. (a) 9 (b) (c) (d)