Which 6 steps of financial statement analysis does Moodys appear to be using? Which steps does it appear not to be using? What questions do you have about Moodys analysis?

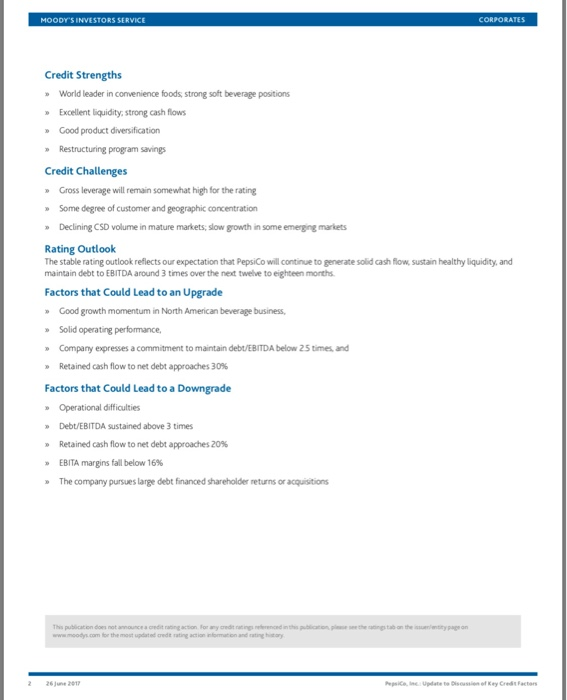

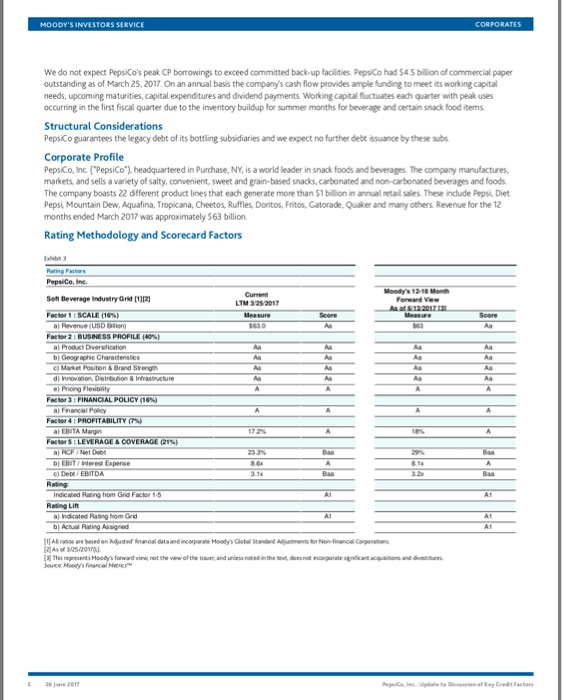

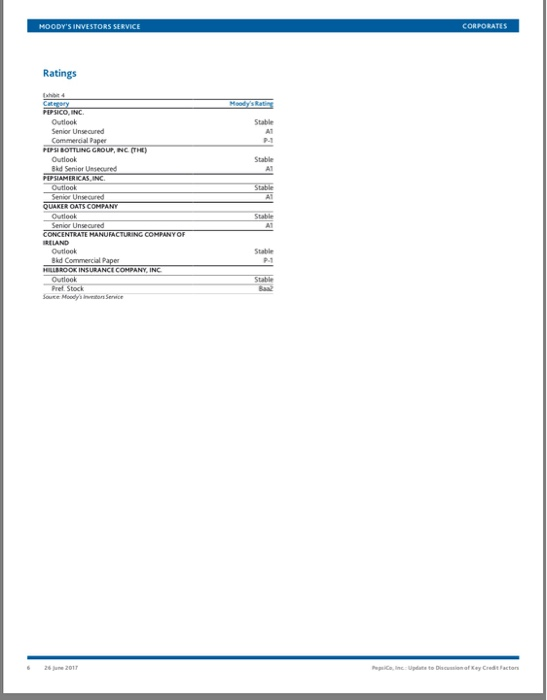

MOODYS INVESTORS SERVICE CREDIT OPINION 26 June 2017 PepsiCo, Inc. Update to Discussion of Key Credit Factors Update Summary Rating Rationale PepsiCo's A1long-term senior unsecured rating reflects its strong snack food and beverage franchises, extensive global footprint, and solid innovation pipelines. It also reflects its efficient operations, and an extensive multifaceted distribution network, as well as its excellent liquidity and solid financial performance. These factors are tempered by gross leverage that-while modest-has been rising over time. The company's liquidity is strong with solid and predictable cash flow, large cash balances and $75 billion in committed Rate this Research> Peps Co, Inc hethase, New kbank faoilities. While PepsiCo's scale, diversity and strong franchises help to offset some ted Sttes leverage creep, we expect that debt to EBITDA will remain slightly above 3 times over the Senior Unsecued- next 12-18 months PepsiCo faces challenges to grow its volume in mature carbonated soft drink (CSD)makets. But this weakness is partially offset by its strong innovation program and productivity initiatives. It is also helped by goodgrowth prospects in food and beverage internationally, and in its Frito-Lay North American snacks segment Gross Leverage at High End of Range for Rating Contacts Linda Montag 12-553-1336 oVice Presidn Peter H. AbL CFA MD-Corporate Finance 12-553-4024 YE 201 VE 20 CORPORATES The difference between gross and net leverage wil increase as PepsiCo continues to build cash oveneas. Most of PepsiCo's cash is domiciled internationally and would require tx payments to repatriate to the U.S. We estimate that the incremental tax rate to bring its foreign earnings home would range from 18%-25% here is tax la change, we expect that PepsiCo would take advantage of the opportunity to bring cash home at lower rates and would use a significant portion of it to reduce US debt, thus lowering gross (but not net) leverage RESTRUCTURING PROGRAM LIKE LY TO OFFER SAVINGS Achieving growth and improving profits should be manageable over the next year due to moderate commodity cost inflation Headwinds, however, will include the ongoing dedine of CSD consumption in North America, constantly evolving consumer preferences and stiffcompetition We expect operating profit growth in the low-to-mid single-digit range. To offset some of these headwinds, PepsiCo announced in early 2014 a $5 billion, five year productivity plan and has taken out $1 billion per year since the program began PepsiCo expects the program to cost a total $990 million pre-tax, of which $705 million will be cash expenditures The company incurred $160 million in charges related to the restructuring initiative in 2016, $95 million of which was cash In addition to the five billion productivity program, Pepsi initiated ts own version of aero-based budgeting or smart spending in Q3 2015 which focuses on right sizing operating expenses without starving top-line growth GOOD PRODUCT DIVERSIFICATION WITH SOME CUSTOMERAND GEOGRAPHIC CONCENTRATION We expect Pepsico's geographic diversity to improve as its operations in emerging markets grow faster than at home. Although its products are sold in more than 200 markets, PepsiCo is not as geographically diversified as some of its competitors It generates about 63% of its net revenues the U S and Canada, both mature markets with delning CSD category trends Nonetheless, PepsiCo's widespread and efficient distribution infrastructure provides it with opportunities to expand its geogaphic reah and intemational revenue base. The company has a clear strategy to further grow its international business, PepsiCo has announced significant capital nvestments in Brasil, India, Mexico, China and Russia in recent years These are mostly related to its food divisions further extending its presence in fast-growing and/or emerging markets We expect PepsiCo to retain solid relationships with retailers Consolidation in the retail industry increases the bargaining power of PepsiCo's largest customers PepsiCo's 2016 net revenues from Wal-Mat represented around 18% of its net sales in North Amerca and 13% of total worldwide net sales. The company's top five retail customers represented around 32% of its 2016 North Amercan net sales. But PepsiCo's powerful stable of high velocity food and beverage brands will continue to make it an important supplier to top retailers EVENT RISK PepsiCo has attracted the interest of activist investors over the past few years, some of which have agitated for transformation at the company including possible sale of businesses. PepsiCo has publically indicated that it isn't interested in such proposals PepsiCo's ratings do not incorporate the possibility of a large business transformation and recent strong performance has been a good defense against such arguments Regardless, we cannot rule out the possibility of change at the company either in its financial strategy or its business configuration or that it could become the target of other lange consumer products companies Liquidity Analysis We expect PepsiCo to maintain a solid liquidity profile over the next 12 to 18 months Its excellent liquidity is characteried by consistent operating cash lows, substantial cash, and high quality short term investments (totaling $16 0 bilion as of 3/25/17) it als has committed bank facilities to support the issuance of short-term debt including commercial paper and near-term bond maturities We estimate that PepsiCo will generate about $2 5 billion of free cash flow (CFO less capex and dividends) over the next 12 months it has $5 9 bilion in debt maturities over the next 12 months which we expect it to refinance PepsKCo has a $3.75 billion five-year committed bank revolving credit facility expiring in June 2022. The faolity has same day availability, contains no ongoing MAC larguage, and no financial covenants Additionally. PepsiCo can borrow up to $375 billion under ts 364-day unsecured revolving credit facility expiring June 2018(which it renews annually) The 364-day revolver contains a one year term-out (at PepsiCo's option) and no financial covenants 4261 MOODY'S INVEST CORPORATE We do not expect PepsiCo's peak CP borrowings to exceed committed back-up facilities. PepsiCo had $4 5 billion of commercial paper outstanding as of March 25, 2017 On an annual basis the company's cash flow provides ample funding to meet its working capital needs, upcoming maturities, capital expenditures and dividend payments Working capital Rluctuates eadh quarter with peak uses occurring in the first fiscal quarter due to the inventory buildup for summer months for beverage and certain snack food items Structural Considerations PepsiCo guarantees the legacy debt of its bottling subsidiaries and we expect no further debt issuance by these subs Corporate Profile PepsiCo, Inc. (PepsiCo"), headquartered in Purchase, NY, is aworld leader in snack foods and beverages. The company manufactures markets, and sells a variety of salty, convenient, sweet and grain-based snacks, carbonated and non-carbonated beverages and foods The company boasts 22 dfferent product lines that each generate more than $1 billion in annual retail sales These include Pepsi, Diet Pepsi Mountain Dew, Aquafina, Tropicana, Cheetos, Ruffles, Doritos, Fritos, Gatorade, Quaker and many others Revenue for the 12 months ended March 2017 was approximately $63 billion Rating Methodology and Scorecard Factors PepsiCo, in. Moody's 12-18 Monh Seft Beverage Industry Grid [1) LTM 3252017 a) Revenu (USD Eason Factor 2: BUSNESS PROFILE (40 63 0 Factor 4 PROFITABILITY Factor S:LEVE ) Debi EBITDA 3.1x 32 Indicated Rating from Grid Factoe t Rating Lin al indcated Rating from Grd b) Achual Rating Assigned 5 24 June 201 Ratings Stable Senior Unsecured PSIBOTTLING GROUP, INC (THE Stable Bd Senior Uesecured Stable Bkd Commercial Paper 26 june 201