Answered step by step

Verified Expert Solution

Question

1 Approved Answer

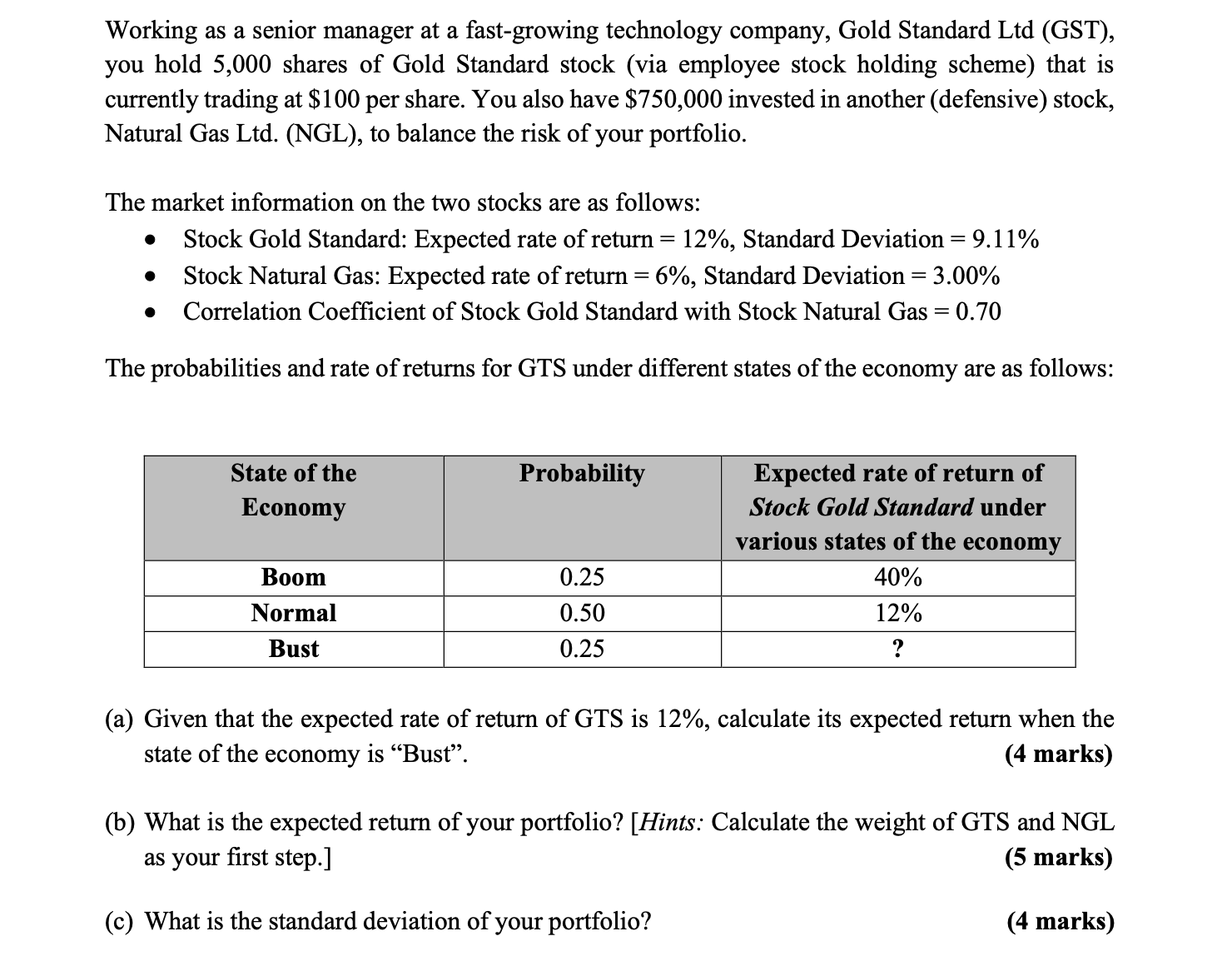

Working as a senior manager at a fast - growing technology company, Gold Standard Ltd ( GST ) , you hold 5 , 0 0

Working as a senior manager at a fastgrowing technology company, Gold Standard Ltd GST

you hold shares of Gold Standard stock via employee stock holding scheme that is

currently trading at $ per share. You also have $ invested in another defensive stock,

Natural Gas LtdNGL to balance the risk of your portfolio.

The market information on the two stocks are as follows:

Stock Gold Standard: Expected rate of return Standard Deviation

Stock Natural Gas: Expected rate of return Standard Deviation

Correlation Coefficient of Stock Gold Standard with Stock Natural Gas

The probabilities and rate of returns for GTS under different states of the economy are as follows:

a Given that the expected rate of return of GTS is calculate its expected return when the

state of the economy is "Bust".

marks

b What is the expected return of your portfolio? Hints: Calculate the weight of GTS and NGL

as your first step.

marks

c What is the standard deviation of your portfolio?

marks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance

Authors: Angelico Groppelli, Ehsan Nikbakht

7th Edition

1438010362, 9781438010366