Answered step by step

Verified Expert Solution

Question

1 Approved Answer

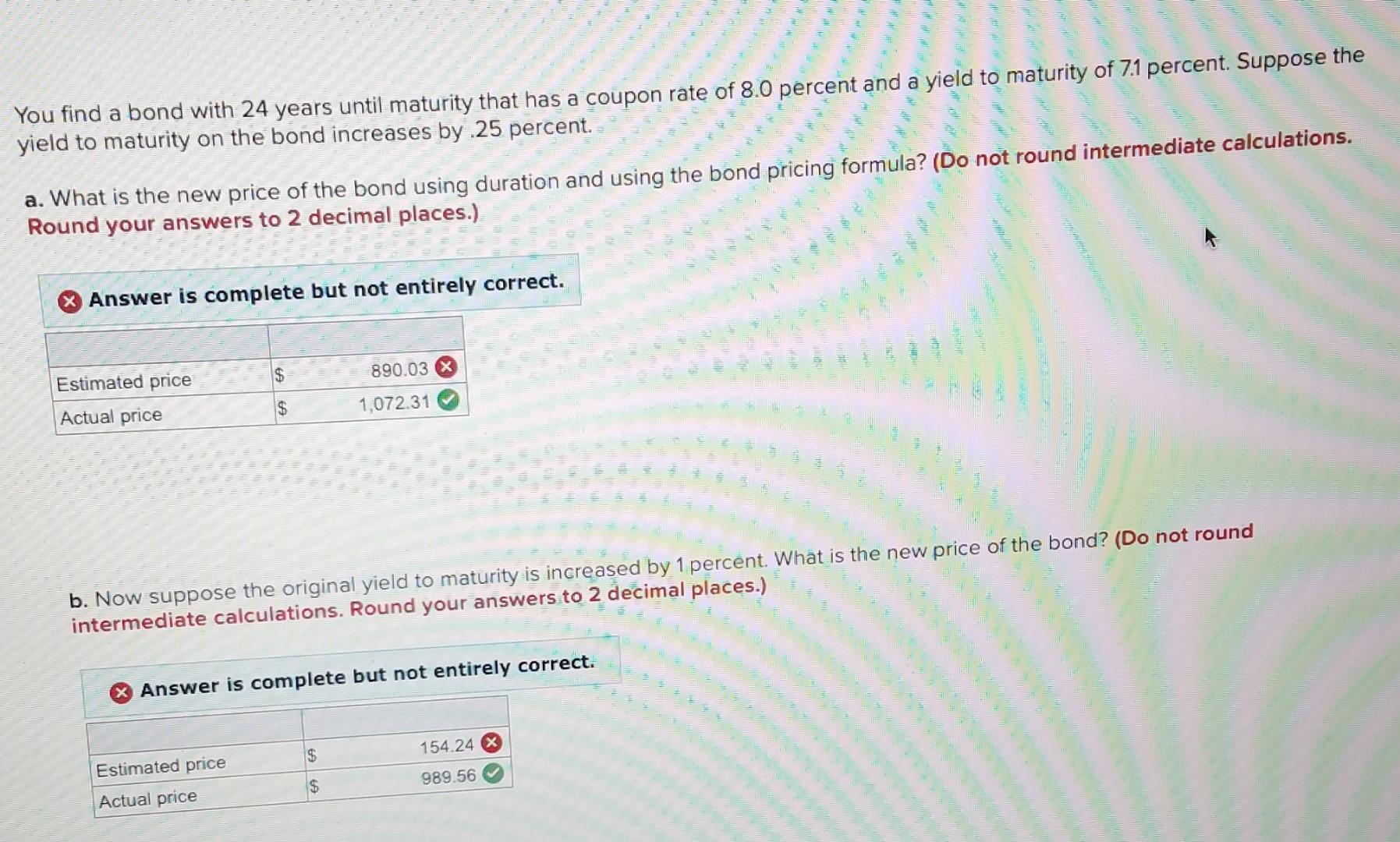

You find a bond with 24 years until maturity that has a coupon rate of 8.0 percent and a yield to maturity of 7.1 percent.

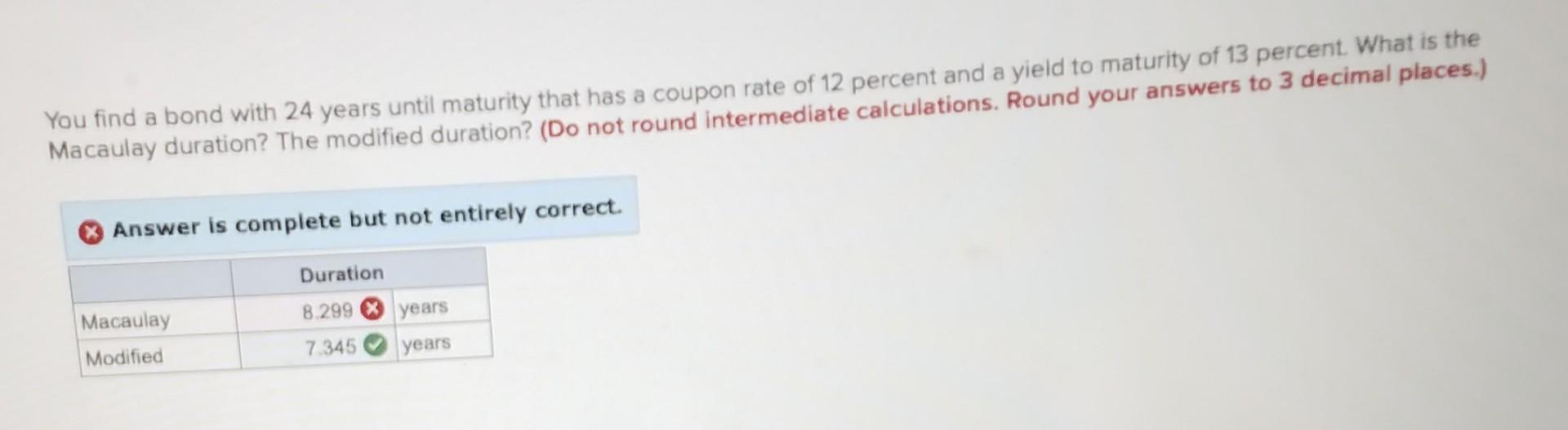

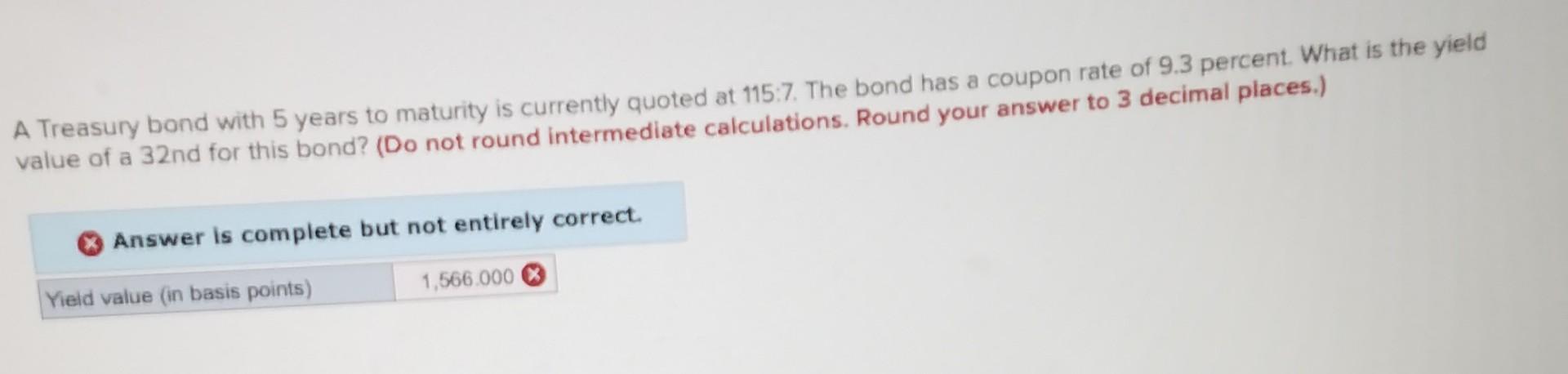

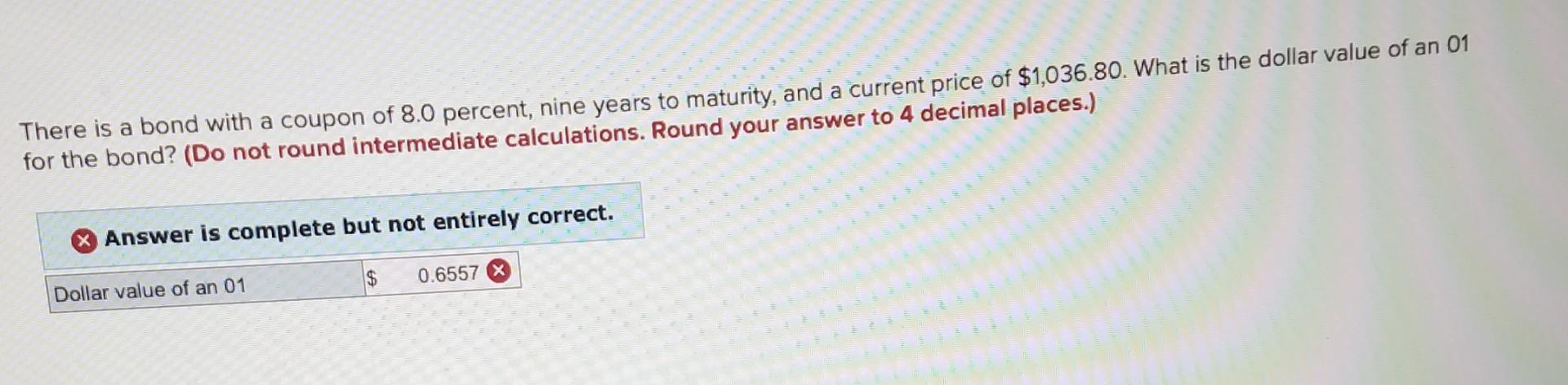

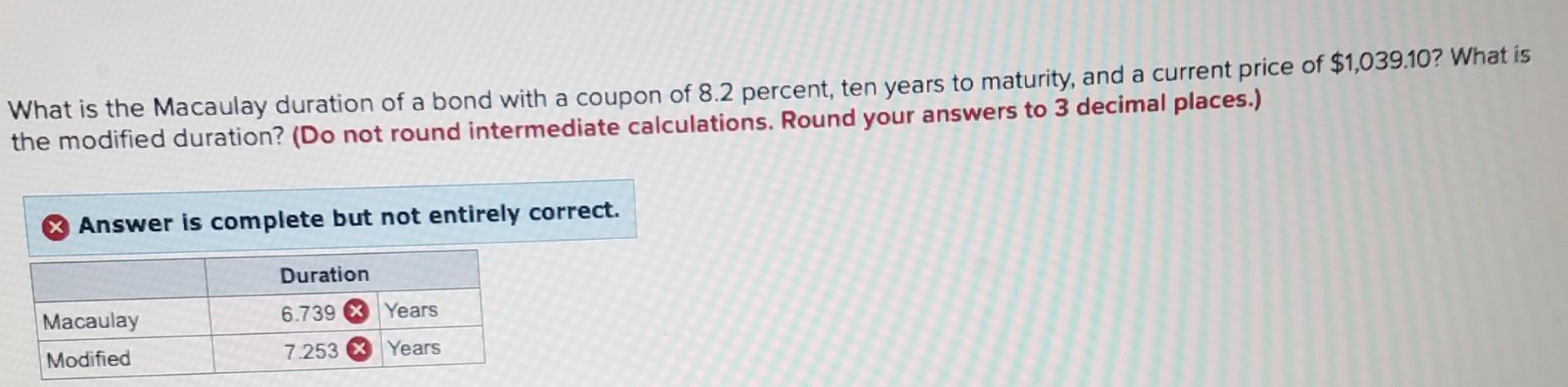

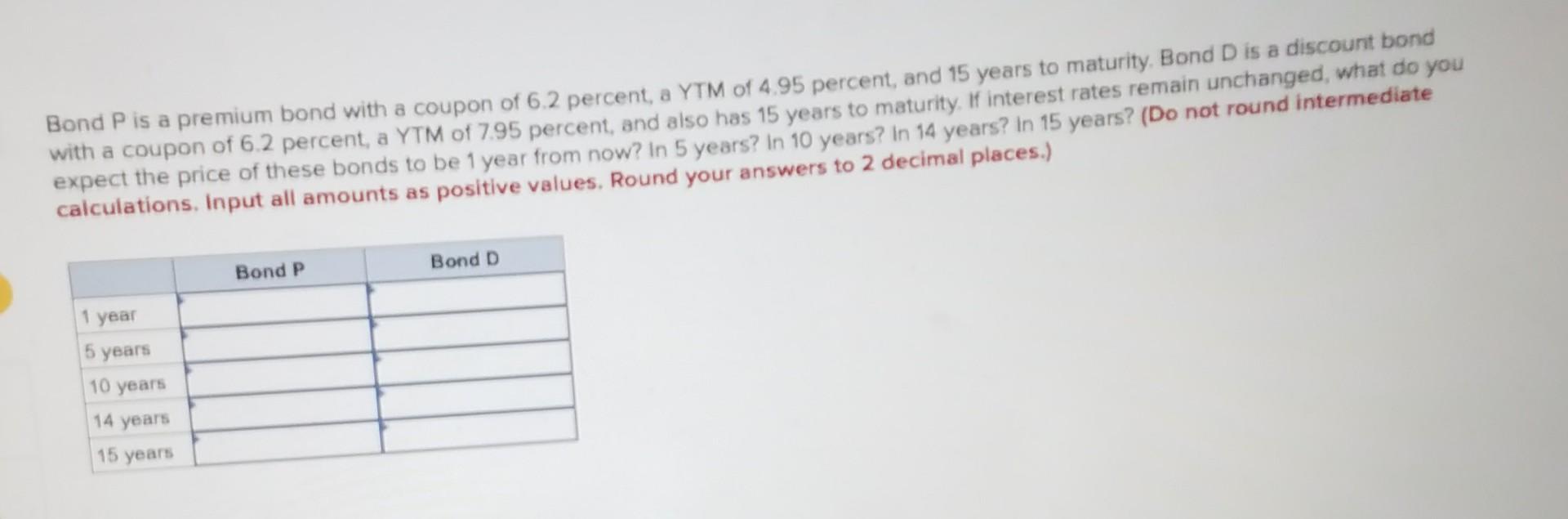

You find a bond with 24 years until maturity that has a coupon rate of 8.0 percent and a yield to maturity of 7.1 percent. Suppose the yield to maturity on the bond increases by .25 percent. a. What is the new price of the bond using duration and using the bond pricing formula? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Answer is complete but not entirely correct. $ 890.03 X Estimated price $ 1,072.31 Actual price b. Now suppose the original yield to maturity is increased by 1 percent. What is the new price of the bond? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Answer is complete but not entirely correct. $ 154.24 x 989.56 Estimated price Actual price $ You find a bond with 24 years until maturity that has a coupon rate of 12 percent and a yield to maturity of 13 percent. What is the Macaulay duration? The modified duration? (Do not round intermediate calculations. Round your answers to 3 decimal places.) Answer is complete but not entirely correct. Macaulay Duration 8.299 years 7.345 years Modified A Treasury bond with 5 years to maturity is currently quoted at 115.7. The bond has a coupon rate of 9.3 percent. What is the yield value of a 32nd for this bond? (Do not round intermediate calculations. Round your answer to 3 decimal places.) Answer is complete but not entirely correct. 1,566.000 Yield value (in basis points) There is a bond with a coupon of 8.0 percent, nine years to maturity, and a current price of $1,036.80. What is the dollar value of an 01 for the bond? (Do not round intermediate calculations. Round your answer to 4 decimal places.) & Answer is complete but not entirely correct. $ 0.6557 X Dollar value of an 01 What is the Macaulay duration of a bond with a coupon of 8.2 percent, ten years to maturity, and a current price of $1,039.10? What is the modified duration? (Do not round intermediate calculations. Round your answers to 3 decimal places.) & Answer is complete but not entirely correct. Duration 6.739 X Years Macaulay Modified 7.253 X Years Bond P is a premium bond with a coupon of 6.2 percent, a YTM of 4.95 percent, and 15 years to maturity, Bond D is a discount bond with a coupon of 6.2 percent, a YTM of 7.95 percent, and also has 15 years to maturity, if interest rates remain unchanged, what do you expect the price of these bonds to be 1 year from now? In 5 years? In 10 years? In 14 years? In 15 years? (Do not round intermediate calculations. Input all amounts as positive values. Round your answers to 2 decimal places.) Bond D Bond P 1 year 5 years 10 years 14 years 15 years

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Thomas Garman, Raymond Forgue

12th edition

9781305176409, 1133595839, 1305176405, 978-1133595830