Answered step by step

Verified Expert Solution

Question

1 Approved Answer

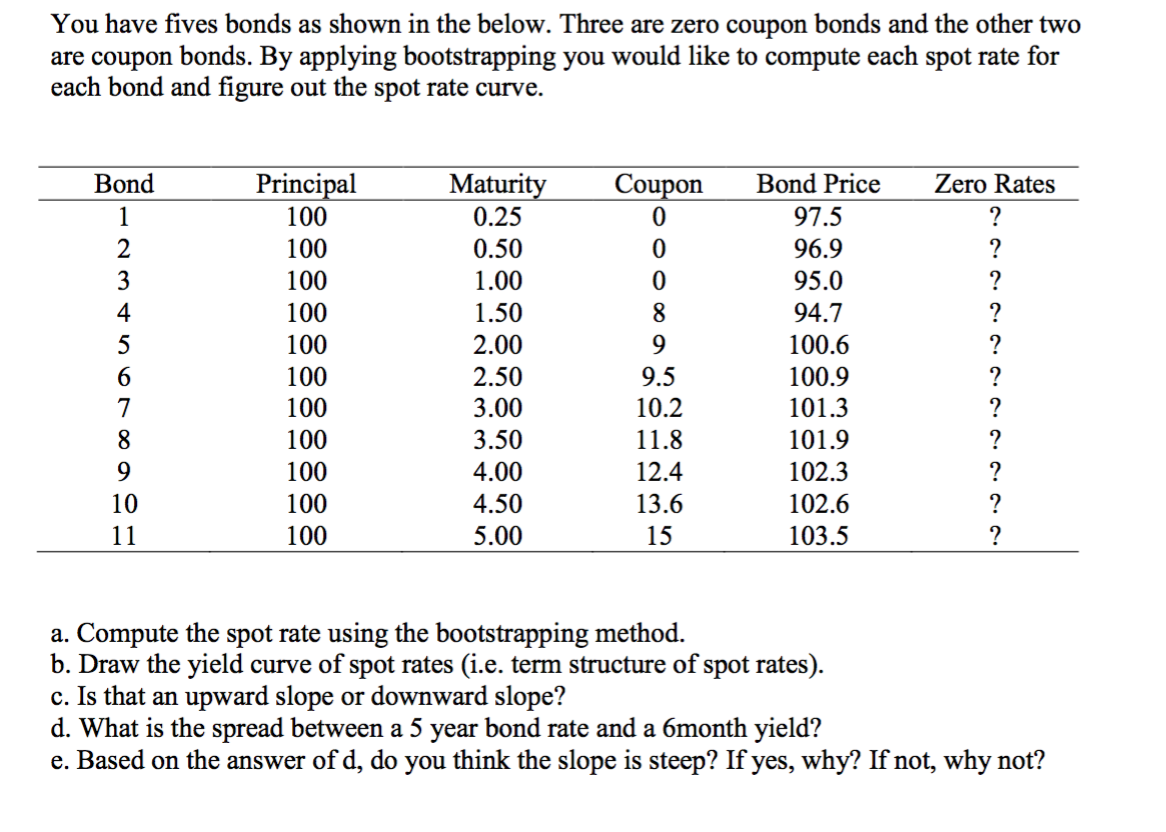

You have fives bonds as shown in the below. Three are zero coupon bonds and the other two are coupon bonds. By applying bootstrapping

You have fives bonds as shown in the below. Three are zero coupon bonds and the other two are coupon bonds. By applying bootstrapping you would like to compute each spot rate for each bond and figure out the spot rate curve. Bond Principal Maturity Coupon Bond Price Zero Rates 1 100 0.25 0 97.5 ? 23456789 100 0.50 0 96.9 ? 100 1.00 0 95.0 ? 100 1.50 8 94.7 ? 100 2.00 9 100.6 ? 100 2.50 9.5 100.9 ? 100 3.00 10.2 101.3 ? 100 3.50 11.8 101.9 100 4.00 12.4 102.3 10 100 4.50 13.6 102.6 11 100 5.00 15 103.5 2222 ? ? ? ? a. Compute the spot rate using the bootstrapping method. b. Draw the yield curve of spot rates (i.e. term structure of spot rates). c. Is that an upward slope or downward slope? d. What is the spread between a 5 year bond rate and a 6month yield? e. Based on the answer of d, do you think the slope is steep? If yes, why? If not, why not?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Bootstrapping Spot Rates and Yield Curve Analysis We can use the bootstrapping method to compute the spot rates for each bond and analyze the resultin...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management for Public Health and Not for Profit Organizations

Authors: Steven A. Finkler, Thad Calabrese

4th edition

133060411, 132805669, 9780133060416, 978-0132805667