ZARA: Fast Fashion Fashion is the imitation of a given example and satises the demand for social adaptation. . . . The more an article

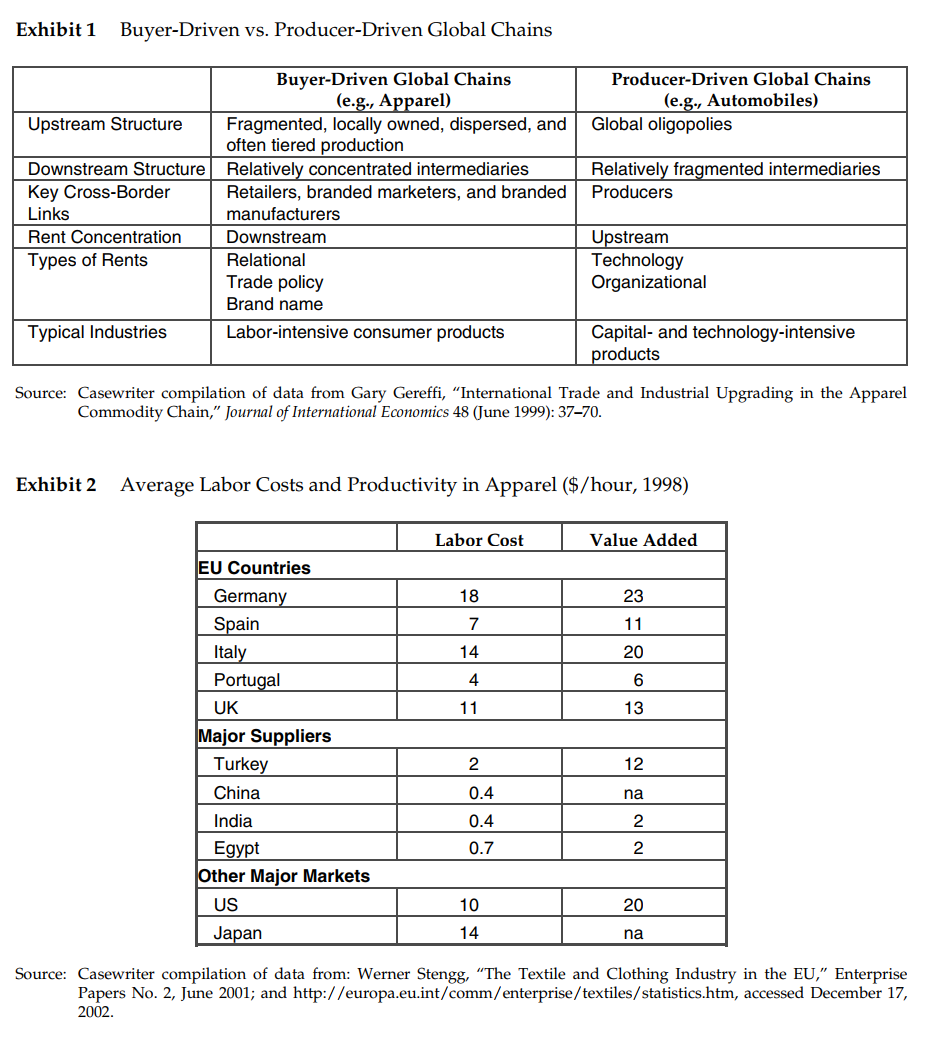

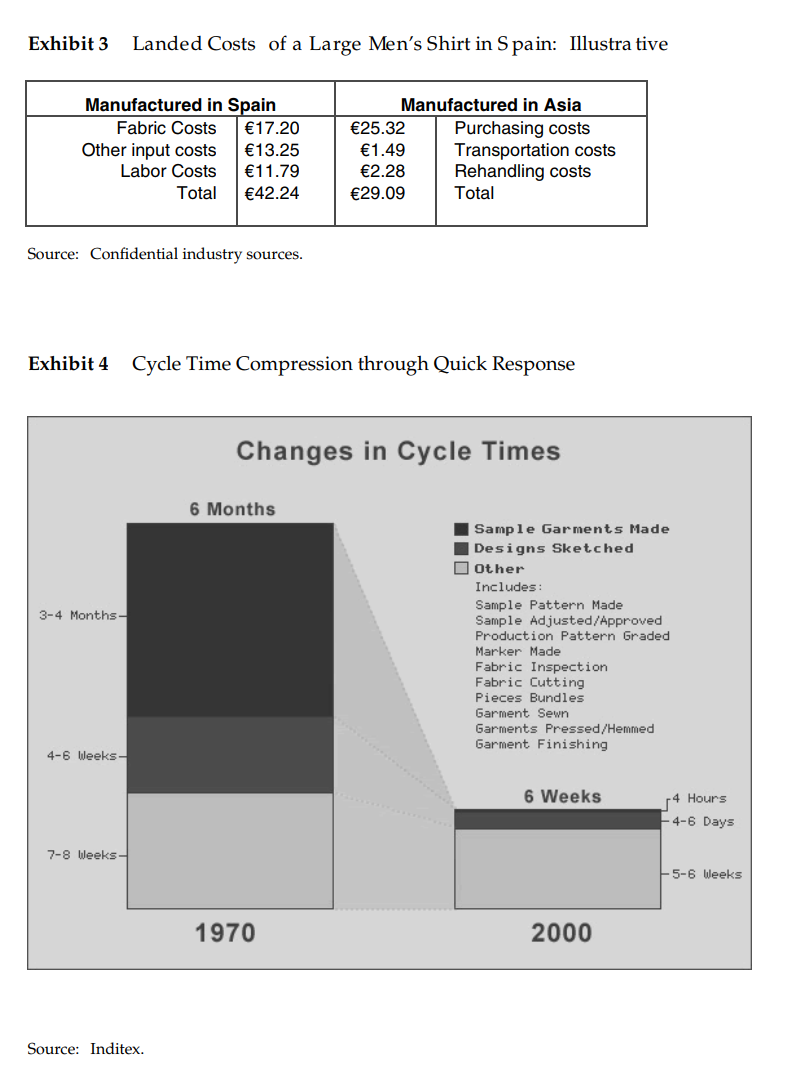

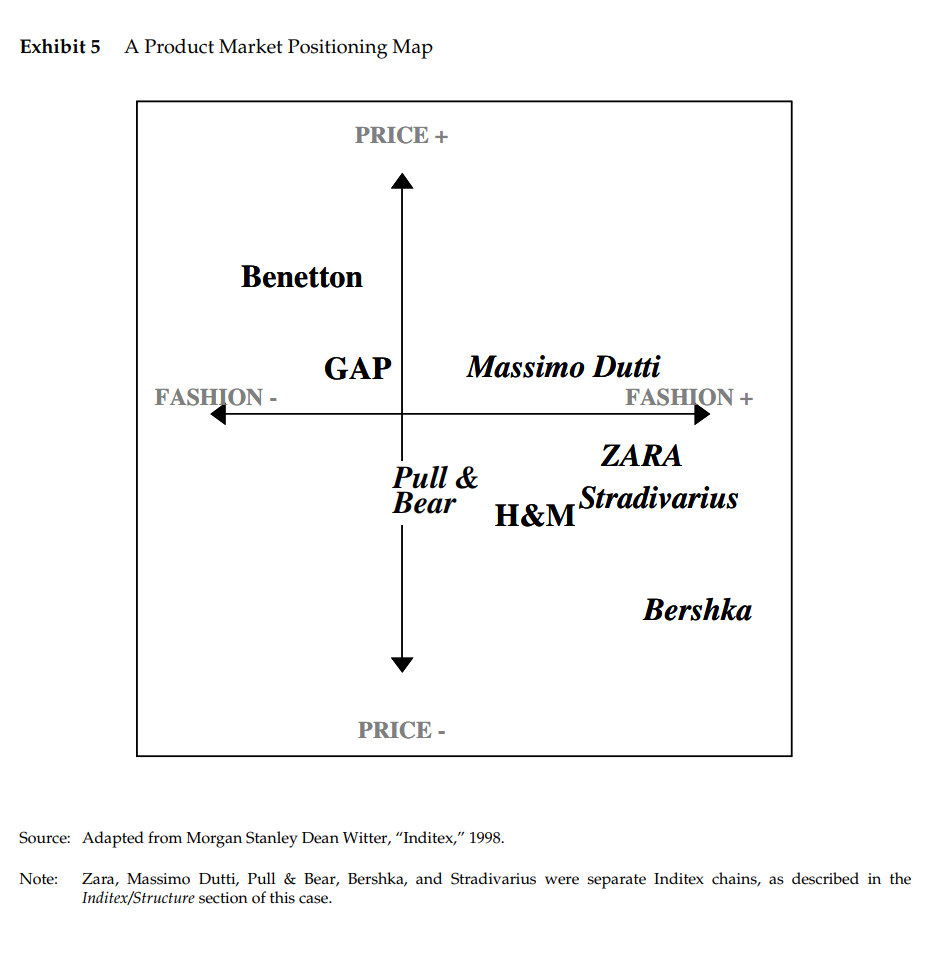

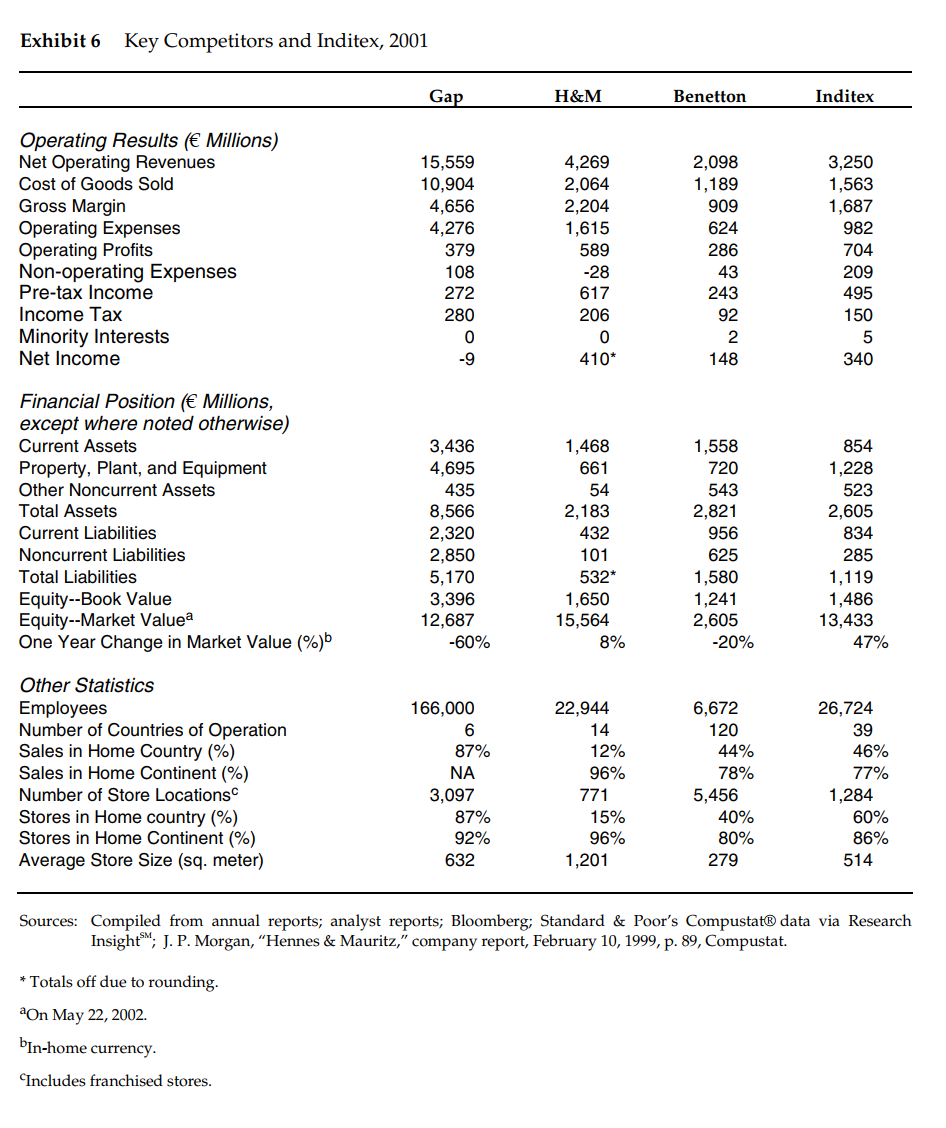

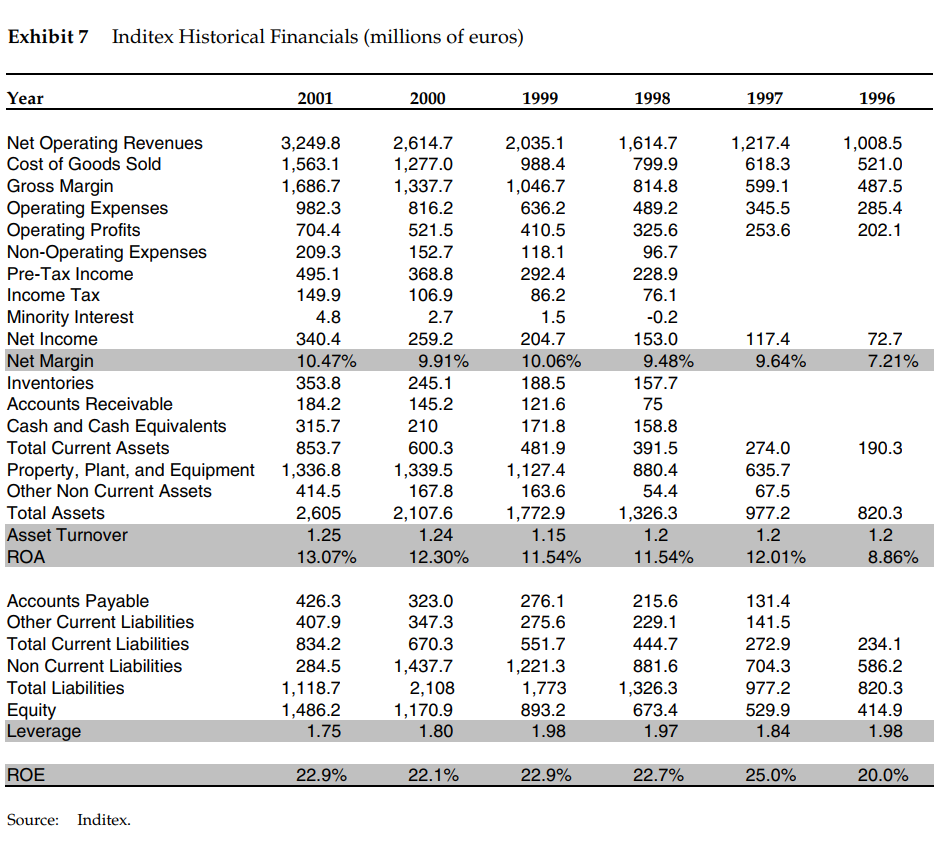

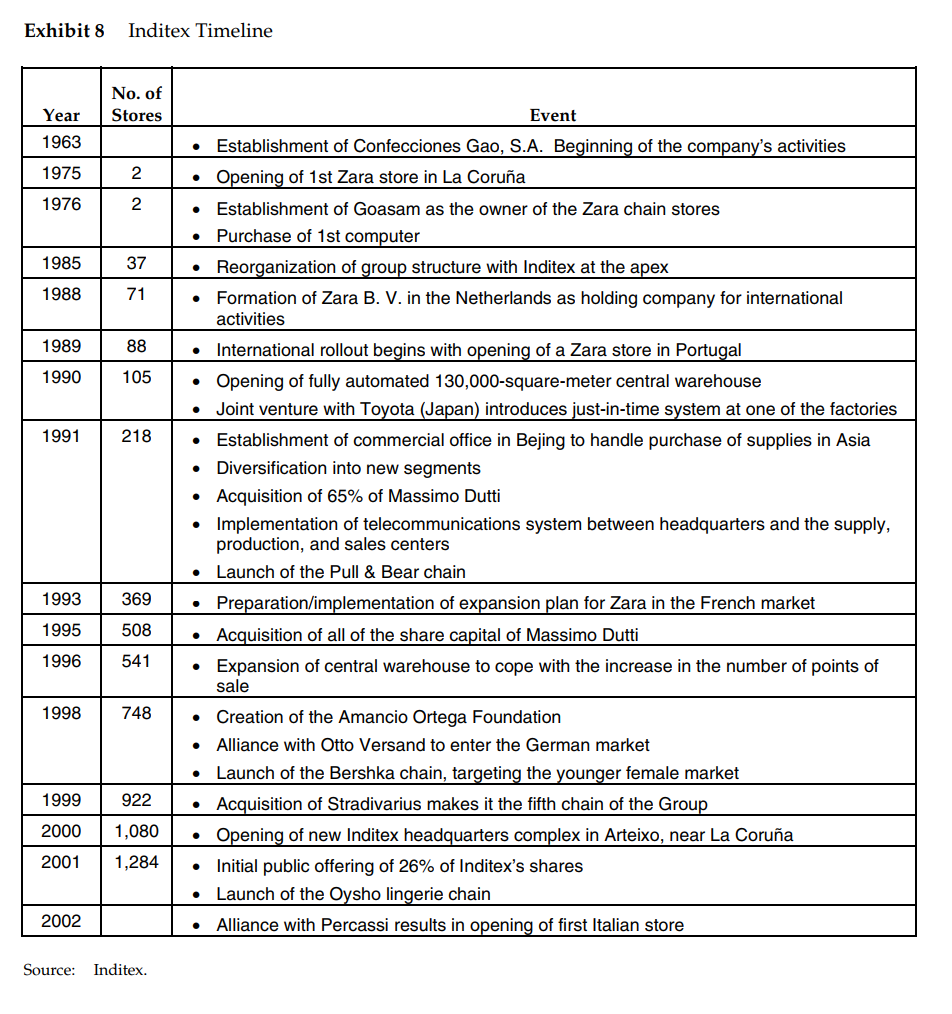

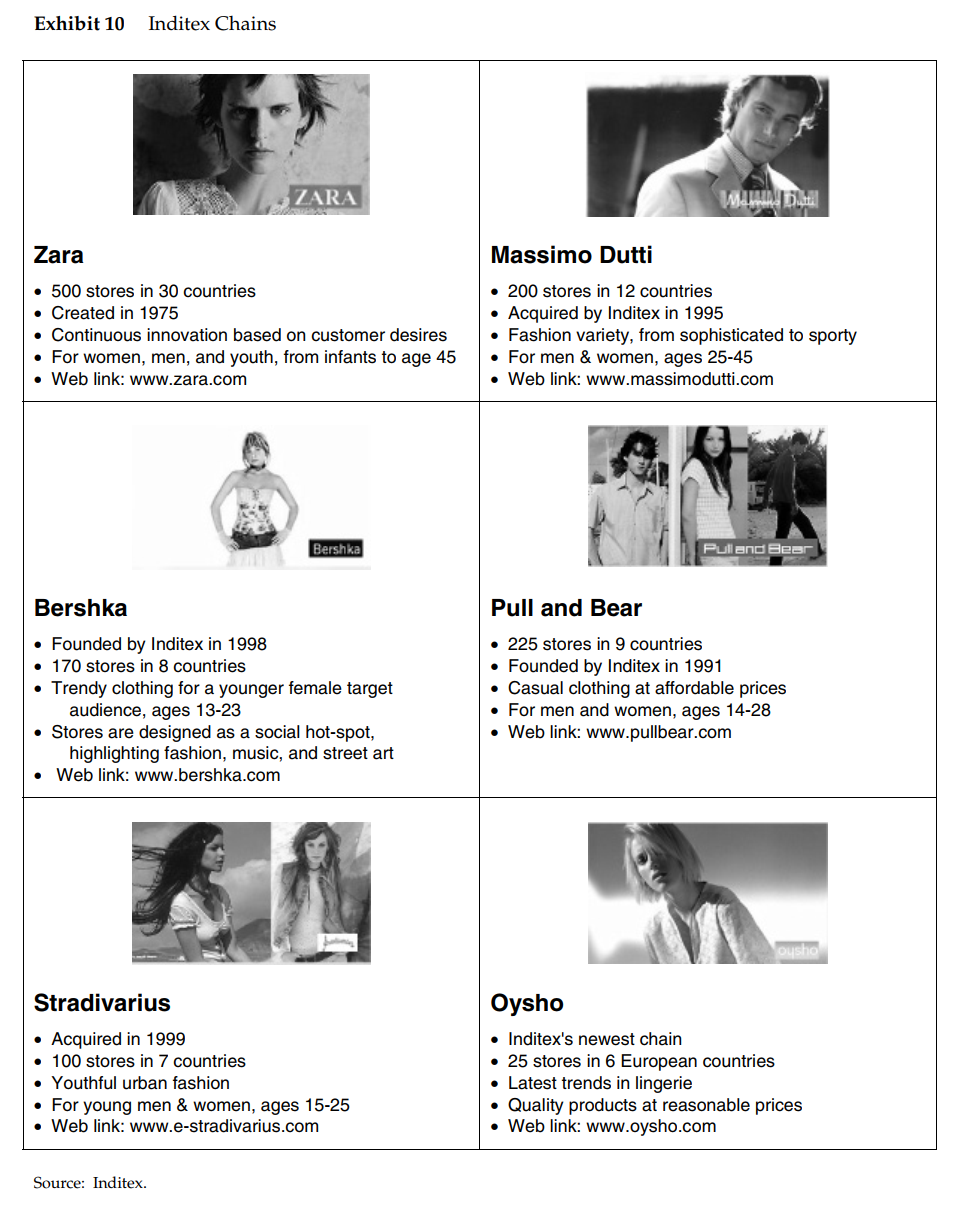

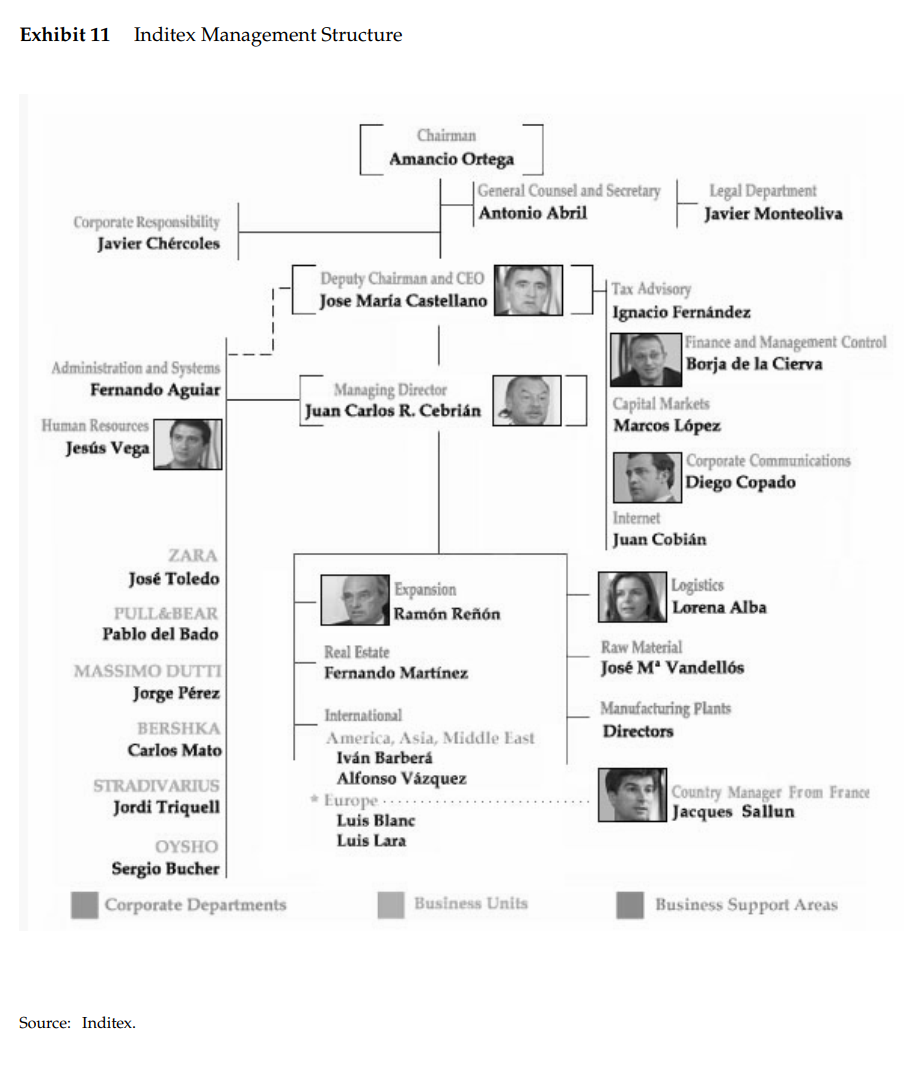

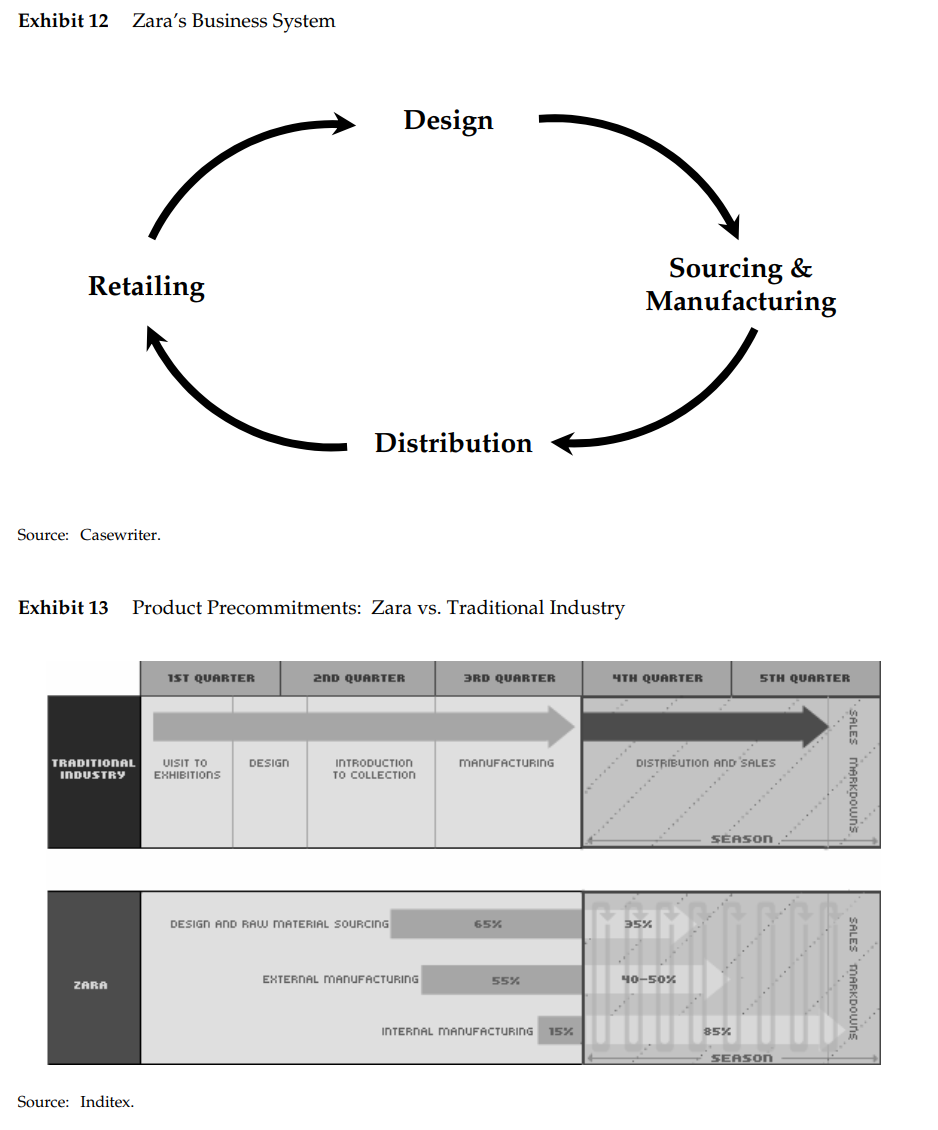

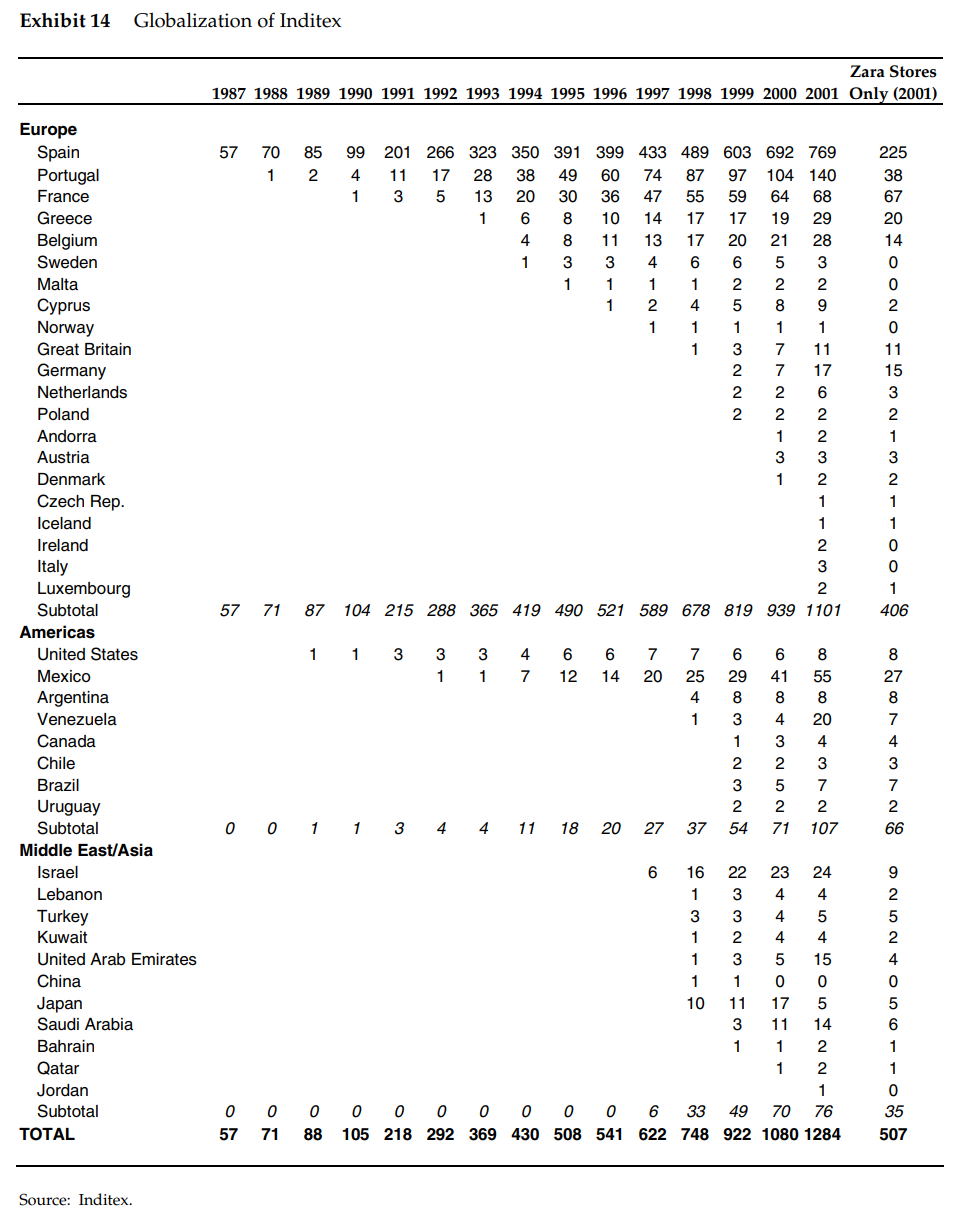

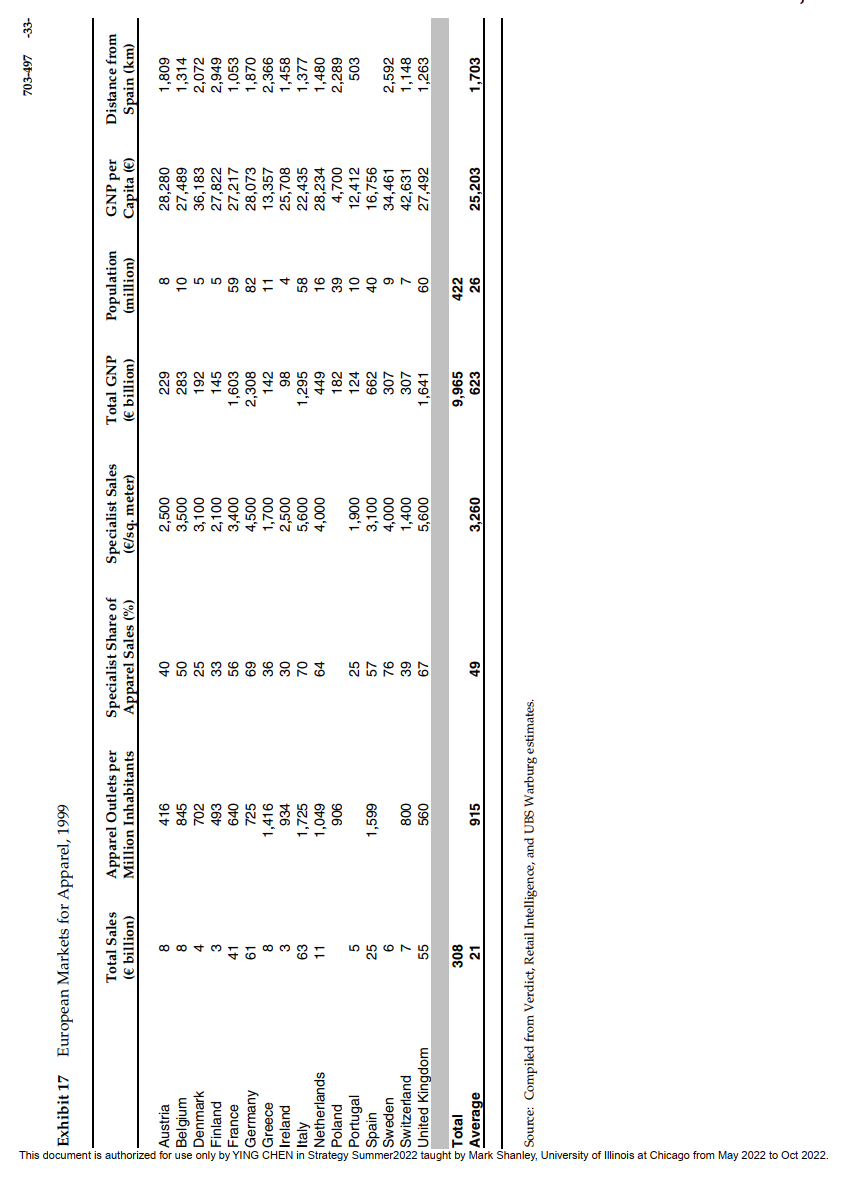

ZARA: Fast Fashion Fashion is the imitation of a given example and satises the demand for social adaptation. . . . The more an article becomes subject to rapid changes of fashion, the greater the demand for cheap products of its kind. Georg Simmel, \"Fashion\" (1904) Inditex (Industria de Diseo Textil) of Spain, the owner of Zara and five other apparel retailing chains, continued a trajectory of rapid, profitable growth by posting net income of 340 million on revenues of 3,250 million in its fiscal year 2001 (ending January 31, 2002). Inditex had had a heavily oversubscribed Initial Public Offering in May 2001. Over the next 12 months, its stock price increased by nearly 50/odespite bearish stock market conditionsto push its market valuation to 13.4 billion. The high stock price made Inditex's founder, Amancio Ortega, who had begun to work in the apparel trade as an errand boy half a century earlier, Spain's richest man. However, it also implied a significant growth challenge. Based on one set of calculations, for example, 76% of the equity value implicit in Inditex's stock price was based on expectations of future growthhigher than an estimated 69% for Wal-Mart or, for that matter, other high-performing retailers.1 The next section of this case briey describes the structure of the global apparel chain, from producers to final customers. The section that follows profiles three of Inditex's leading international competitors in apparel retailing: The Gap (U.S.), Hennes & Mauritz (Sweden), and Benetton (Italy). The rest of the case focuses on Inditex, particularly the business system and international expansion of the Zara chain that dominated its results. The Global Apparel Chain The global apparel chain had been characterized as a prototypical example of a buyer-driven global chain, in which profits derived from \"unique combinations of high-value research, design, sales, marketing, and financial services that allow retailers, branded marketers, and branded manufacturers to act as strategic brokers in linking overseas factories\"2 with markets. These attributes were thought to distinguish the vertical structure of commodity chains in apparel and other labor- intensive industries such as footwear and toys from producer-driven chains (e. g., in automobiles) that were coordinated and dominated by upstream manufacturers rather than downstream intermediaries (see Exhibit 1). Production Apparel production was very fragmented. On average, individual apparel manufacturing firms employed only a few dozen people, although internationally traded production, in particular, could feature tiered production chains comprising as many as hundreds of firms spread across dozens of countries. About 30% of world production of apparel was exported, with developing countries generating an unusually large share, about one-half, of all exports. These large cross-border ows of apparel reected cheaper labor and inputspartly because of cascading labor efcienciesin developing countries. (See Exhibit 2 for comparative labor productivity data and Exhibit 3 for an example.) Despite extensive mvestments in substituting capital for labor, apparel production remained highly labor-intensive so that even relatively large \"manufacturers\" in developed countries outsourced labor-intensive production steps (e.g., sewing) to lower-cost labor sources nearby. Proximity also mattered because it reduced shipping costs and lags, and because poorer neighbors sometimes benefited from trade concessions. While China became an export powerhouse across the board, greater regionalization was the dominant motif of changes in the apparel trade in the 1990s. Turkey, North Africa, and sundry Eastern European countries emerged as major suppliers to the European Union; Mexico and the Caribbean Basin as major suppliers to the United States; and China as the dominant supplier to Japan (where there were no quotas to restrict imports)? World trade in apparel and textiles continued to be regulated by the Multi-Fiber Arrangement (MFA), which had restricted imports into certain markets (basically the United States, Canada, and Western Europe) since 1974. Two decades later, agreement was reached to phase out the MEA's quota system by 2005, and to further reduce tariffs (which averaged 7% to 9% in the major markets). As of 2002, some warned that the transition to the post-WA world could prove enormously disruptive for suppliers in many exporting and importing countries, and might even ignite demands for \"managed trade.\" There was also potential for protectionism in the questions that nongovernmental organizations and others in developed countries were posing about the basic legitimacy of \"sweatshop trade\" in buyer-driven global chains such as apparel and footwear. Cross-Border In termediation Trading companies had traditionally played the primary role in orchestrating the physical ows of apparel from factories in exporting countries to retailers in importing countries. They continued to be important cross-border intermediaries, although the complexity and (as a result) the specialization of their operations seemed to have increased over time. Thus, Hong Kong's largest trading company, Li 6: Fung, derived 75% of its turnover from apparel and the remainder from hard goods by setting up and managing multinational supply chains for retail clients through its offices in more than 30 countries.4 For example, a down jacket's filling might come from China, the outer shell fabric from Korea, the zippers from japan, the inner lining from Taiwan, and the elastics, label, and other trim from Hong Kong. Dyeing might take place in South Asia and stitching in China, followed by quality assurance and packaging in Hong Kong. The product might then be shipped to the United States for delivery to a retailer such as The Limited or Abercrombie 8: Fitch, to whom credit risk matching, market research, and even design services might also be supplied. Branded marketers represented another, newer breed of middlemen. Such intermediaries outsourced the production of apparel that they sold under their own brand names. Liz Claiborne, founded in 1976, was a good example.5 Its eponymous founder identified a growing customer group (professional women) and sold them branded apparel designed to fit evolving workplace norms and their actual shapes (which she famously described as \"pear-shaped"), that was presented in collections within which they could mix and match in upscale department stores. Production was outsourced from the outset, rst domestically, and then, in the course of the 19805, increasingly to Asia, with a heavy reliance on OEM or \"full-package" suppliers. Production was organized in terms of six seasons rather than four to let stores buy merchandise in smaller batches. After a performance decline in the first half of the 1990s, Liz Claiborne restructured its supply chain to reduce the number of suppliers and inventory levels, shifted half of production back to the Western Hemisphere to compress cycle times, and simultaneously cut the number of seasonal collections from six to four so as to allow some reorders of merchandise that was selling well in the third month of a season. Other types of cross-border intermediaries could be seen as forward or backward integrators rather than as pure middlemen. Branded manufacturers, like branded marketers, sold products under their own brand names through one or more independent retail channels and owned some manufacturing as well. Some branded manufacturers were based in developed countries (e.g., US.- based VF Corporation, which sold jeans produced in its factories overseas under the Lee and Wrangler brands) and others in developing countries (e.g., Giordano, Hong Kong's leading apparel brand). In terms of backward integration, many retailers internalized at least some cross-border functions by setting up their own overseas buying offices, although they continued to rely on specialized intermediaries for others (e.g., import documentation and clearances). Retailing Irrespective of whether they internalized most cross-border functions, retailers played a dominant role in shaping imports into developed countries: thus, direct imports by retailers accounted for half of all apparel imports into Western Europe.+5 The increasing concentration of apparel retailing in major markets was thought to be one of the key drivers of increased trade. In the United States, the top five chains came to account for more than half of apparel sales during the 19905, and concentration levels elsewhere, while lower, also rose during the decade. Increased concentration was generally accompanied by displacement of independent stores by retail chains, a trend that had also helped increase average store size over time. By the late 19905, chains accounted for about 85% of total retail sales in the United States, about 7'0% in Western Europe, between one-third to one-half in Latin America, East Asia, and Eastern Europe, and less than 10% in large but poor markets such as China and India.\"r Larger apparel retailers had also played the leading role in promoting quick response (QR), a set of policies and practices targeted at improving coordination between retailing and manufacturing in order to increase the speed and flexibility of responses to market shifts, which began to diffuse in apparel and textiles in the second half of the 1980s.3 QR required changes that spanned functional, geographic, and organizational boundaries but could help retailers reduce forecast errors and inventory risks by planning assortments closer to the selling season, probing the market, placing smaller initial orders and reordering more frequently, and so on. QR had led to significant compression of cycle times (see Exhibit 4), enabled by improvements in information technology and encouraged by shorter fashion cycles and deeper markdowns, particularly in women's wear. Retailing activities themselves remained quite local: the top 10 retailers worldwide operated in an average of 10 countries in 2000compared with top averages of 135 countries in pharmaceuticals, 73 in petroleum, 44 in automobiles, and 33 in electronicsand derived less than 15% of their total sales from outside their home markets.9 Against this baseline, apparel retailing was relatively globalized, particularly in the fashion segment. Apparel retailing chains from Europe had been the most successful at cross-border expansion, although the US. market remained a major challenge. Their success probably reected the European design roots of apparelsomewhat akin to U.S.-based fast food chains' international dominanceand the gravitational pull of the large U.S. market for US.- based retailers. Thus, The Gap, based on its sales at home in the United States, dwarfed H&:M and Inditex combined. The latter two companies were perhaps the most pan-European apparel retailers but had yet to achieve market shares of more than 2%3% in more than two or three major countries. Markets and Customers In 2000, retail spending on clothing or apparel reached approximately 900 billion worldwide. According to one set of estimates, (Western) Europe accounted for 34% of the total market, the United States for 29%, and Asia for 23%.1D Differences in market size reected signicant differences in per capita spending on apparel as well as in population levels. Per capita spending on apparel tended to grow less than proportionately with increases in per capita income, so that its share of expenditures typically decreased as income increased. Per capita spending was also affected by price levels, which were inuenced by variations in per capita income, in costs, and in the intensity of competition (given that competition continued to be localized to a significant extent). There was also signicant local variation in customers' attributes and preferences, even within a region or a country. Just within Western Europe, for instance, one study concluded that the British sought out stores based on social affinity, that the French focused on variety/ quality, and that Germans were more price-sensitive.\" Relatedly, the French and the Italians were considered more fashion-forward than the Germans or the British. Spaniards were exceptional in buying apparel only seven times a year, compared with a European average of nine times a year, and higher-than-average levels for the Italians and French, among others. 12 Differences between regions were even greater than within regions: Japan, while generally traditional, also had a teenage market segment that was considered the trendiest in the world on many measures, and the US. market was, from the perspective of many European retailers, significantly less trendy except in a few, generally coastal pockets. There did, however, seem to be more cross-border homogeneity within the fashion segment. Popular fashion, in particular, had become less of a hand-me-down from high-end designers. It now seemed to move much more quickly as people, especially young adults and teenagers, with ever richer communication links reacted to global and local trends, including other elements of popular culture (e.g., desperately seeking the skirt worn by the rock star at her last concert). Attempts had also been made to identify the strategic implications of the changing structure of the global apparel chain that were discussed above. Some implications simplified to \"get big fast\"; others, however, were more sophisticated. Thus, an article by three McKinsey consultants identified five ways for retailers to expand across borders: choosing a \"sliver" of value instead of competing across the entire value chain; emphasizing partnering; investing in brands; minimizing (tangible) investments; and arbitraging international factor price differences.13 But Inditex, particularly its Zara chain, served as a reminder that strategic imperatives depended on how a retailer sought to create and sustain a competitive advantage through its cross-border activities. Key International Competitors While Inditex competed with local retailers in most of its markets, analysts considered its three closest comparable competitors to be The Gap, H&:M, and Benetton. All three had narrower vertical scope than Zara, which owned much of its production and most of its stores. The Gap and HkM, which were the two largest specialist apparel retailers in the world, ahead of Lnditex, owned most of their stores but outsourced all production. Benetton, in contrast, had invested relatively heavily in production, but licensees ran its stores. The three competitors were also positioned differently in product space from [nditex's chains. (See Exhibit 5 for a positioning map and Exhibit 6 for nancial and other comparisons.)l4 The Gap The Gap, based in San Francisco, had been founded in 1969 and had achieved stellar growth and profitability through the 1980s and much of the 19905 with what was described as an \"unpretentious real clothes stance,\" comprising extensive collections of T-shirts and jeans as well as \"smart casual\" work clothes. The Gap's production was internationalizedmore than 90% of it was outsourced from outside the United Statesbut its store operations were U.S.-centric. Intemational expansion of the store network had begun in 1987, but its pace had been limited by difculties finding locations in markets such as the United Kingdom, Germany, and Japan (which accounted for 86% of store locations outside North America}, adapting to different customer sizes and preferences, and dealing with what were, in many cases, more severe pricing pressures than in the United States. By the end of the 1990s, supply chains that were still too long, market saturation, imbalances and inconsistencies across the company's three store chantsBanana Republic, The Gap, and Old Navyand the lack of a clear fashion positioning had started to take a toll even in the US. market. A failed attempt to reposition to a more fashion-driven assortmenta major fashion misstriggered significant writedowns, a loss for calendar year 2001, a massive decline in The Gap's stock price, and the departure, in May 2002, of its long-time CEO, Niillard Drexler. Hennes and Mauritz I-Iennes and Mauritz (HEIM), founded as I-lennes (hers) in Sweden in 1947, was another high- performing apparel retailer. While it was considered Inditex's closest competitor, there were a number of key differences. H&M outsourced all its production, half of it to European suppliers, implying lead times that were good by industry standards but significantly longer than Zara's. HSIM had been quicker to internationalize, generating more than half its sales outside its home country by 1990, 10 years earlier than Inditex. H&M also had adopted a more focused approach, entering one cormtry at a timewith an emphasis on northern Europeand building a distribution center in each one. Unlike lnditex, H&:M operated a single format, although it marketed its clothes under numerous labels or concepts to different customer segments. HuSrM also tended to have slightly lower prices than Zara (which H&:M displayed prominently in store windows and on shelving), engaged in extensive advertising like most other apparel retailers, employed fewer designers (60% fewer than Zara, although Zara was still 40% smaller), and refurbished its stores less frequently. H&M's price- earnings ratio, while still high, had declined to levels comparable to Inditex's because of a fashion miss that had reduced net income by 17% in 2000 and because of a recent announcement that an aggressive effort to expand in the United States was being slowed down. Benetton Benetton, incorporated in 1965 in Italy, emphasized brightly colored knitwear. It achieved prominence in the 19805 and 1990s for its controversial advertising and as a network organization that outsourced activities that were labor-intensive or scale-insensitive to subcontractors. But Benetton actually invested relatively heavily in controlling other production activities. Where it had little investment was downstream: it sold its production through licensees, often entrepreneurs with no more than $100,000 to invest in a small outlet that could sell only Benetton products. While Benetton was fast at certain activities such as dyeing, it looked for its retailing business to provide significant forward order books for its manufacturing business and was therefore geared to operate on lead times of several months. Benetton's format appeared to hit saturation by the early 19905, and profitability continued to slide through the rest of the 19905. In response, it embarked on a strategy of narrowing product lines, further consolidating key production activities by grouping them into "production poles\" in a number of different regions, and expanding or focusing existing outlets while starting a program to set up much larger company-owned outlets in big cities. About 100 such Benetton megastores were in operation by the end of 2001, compared with a network of approximately 5,500 smaller, third-party-owned stores. Inditex lnditex (Industria de Diseo Textil) was a global specialty retailer that designed, manufactured, and sold apparel, footwear, and accessories for women, men, and children through Zara and five other chains around the world. At the end of the 2001 fiscal year, it operated 1,284 stores around the world, including Spain, with a selling area of 659,400 square meters. The 515 stores located outside of Spain generated 54% of the total revenues of 3,250 million. lnditex employed 26,724 people, 10,919 of them outside Spain. Their average age was 26 years, and the overwhelming majority were women (78%}. Just over 80% of Inditex's employees were engaged in retail sales in stores; 8.5% were employed in manufacturing; and design, logistics, distribution, and headquarters activities accounted for the remainder. Capital expenditures had recently been split roughly 80% on new-store openings, 10% on refurbishing, and 10% on logistics/ maintenance, roughly in line with capital employed. Operating working capital was negative at most year-ends, although it typically registered higher levels at other times of the year given the seasonality of apparel sales. (See Exhibit 7 for these and other historical nancial data.) Plans for 2002 called for continued ght management of working capital and 510560 million of capital expenditures, mostly on opening 230275 new stores (across all chains). The operating economics for 2001 had involved gross margins of 52%, operating expenses equivalent to 30% of revenues, of which one-half were related to personnel, and operating margins of 22%. Net margins on sales revenue were about one-half the size of operating margins, with depreciation of xed assets (158 million) and taxes (150 million) helping reduce operating profits of 704 million to net income of 340 million. Despite high margins, top management stressed that Inditex was not the most profitable apparel retailer in the worldthat stability was perhaps a more distinctive feature. The rest of this section describes the pluses and minuses of Inditex's home base, its foundation by Amancio Ortega and subsequent growth, the structure of the group in early 2002, and recent changes in its governance. (A timeline, Exhibit 8, summarizes key events over this period chronologically.) Home Base Inditex was headquartered in and had most of its upstream assets concentrated in the region of Galicia on the northwestern tip of Spain (see Exhibit 9). Galicia, the third-poorest of Spain's 17 autonomous regions, reported an unemployment rate in 2001 of 17% (compared with a national average of 14%), had poor communication links with the rest of the country, and was still heavily dependent on agriculture and fishing. In apparel, however, Galicia had a tradition that dated back to the Renaissance, when Galicians were tailors to the aristocracy, and was home to thousands of small apparel workshops. What Galicia lacked were a strong base upstream in textiles, sophisticated local demand, technical institutes and universities to facilitate specialized initiatives and training, and an industry association to underpin these or other potentially cooperative activities. And even more critical for Inditex, as CEO Jose Maria Castellano put it, was that "Galicia is in the corner of Europe from the perspective of transport costs, which are very important to us given our business mode .\" Some of the same characterizations applied at a national level, to Inditex's home base of Spain compared, for example, to Italy. Spanish consumers demanded low prices but were not considered as discriminating or fashion-conscious as Italian buyersalthough Spain had advanced rapidly in this regard as well as in many others, since the death of long-time dictator General Francisco Franco in 1975 and the country's subsequent opening up to the world. On the supply side, Spain was a relatively productive apparel manufacturing base by European standards (see Exhibit 2), but lacked Italy's fully developed thread-to-apparel vertical chain (including machinery suppliers), its dominance of high-quality fabrics (such as wool suiting), and its international fashion image. For this reason, and because rivalry among them had historically been fierce, Italian apparel chains had been quick to move overseas. Spanish apparel retailers had followed suit in the 1990s, and not just lnditex. Mango, a smaller Spanish chain that relied on a franchising model with returnable merchandise, was already present in more countries around the world than Inditex. Early History Amancio Ortega Gaona, Inditex's founder, was still its president and principal shareholder in early 2002 and still came in to work every day, where he could often be seen lunching in the company cafeteria with employees. Ortega was otherwise extremely reclusive, but reports indicated that he had been born in 1936 to a railroad worker and a housemaid and that his first job had been as an errand boy for a La Corufia shirtmaker in 1949. As he moved up through that company, he apparently developed a heightened awareness of how costs piled up through the apparel chain. In 1963, he founded Confecciones Goa (his initials reversed) to manufacture products such as housecoats. Eventually, Ortega's quest to improve the manufacturing/ retailing interface led him to integrate forward into retailing: the first Zara store was opened on an upmarket shopping street in La Corua, in 1975. From the beginning, Zara positioned itself as a store selling \"medium quality fashion clothing at affordable prices.\" By the end of the 1970s, there were half a dozen Zara stores in Galician cities. Ortega, who was said to be a gadgeteer by inclination, bought his rst computer in 1976. At the time, his operations encompassed just four factories and two stores but were already making it clear that what (other) buyers ordered from his factories was different from what his store data told him customers wanted. Ortega's interest in information technology also brought him into contact with Iose Maria Castellano, who had a doctorate in business economics and professional experience in information technology, sales, and finance. In 1985, Castellano joined lnditex as the deputy chairman of its board of directors, although he continued to teach accounting part-time at the local university. Under Ortega and Castellano, Zara continued to roll out nationally through the 19805 by expanding into adjoining markets. It reached the Spanish capital, Madrid, in 1985 and, by the end of the decade, operated stores in all Spanish cities with more than 100,000 inhabitants. Zara then began to open stores outside Spain and to make quantum investments in manufacturing logistics and IT. The early 1990s was also when lnditex started to add other retail chains to its network through acquisition as well as internal development. Structure At the beginning of 2002, Inditex operated six separate chains: Zara, Massimo Dutti, Pull 8.: Bear, Bershka, Stradivarius, and Oysho (as illustrated in Exhibit 10). These chains' retailing subsidiaries in Spain and abroad were grouped into 60 companies, or about one-half the total number of companies whose results were consolidated into Inditex at the group level; the remainder were involved in textile purchasing and preparation, manufacturing, logistics, real estate, finance, and so forth. Given internal transfer pricing and other policies, retailing (as opposed to manufacturing and other activities) generated 82% of Inditex's net income, which was roughly in line with its share of the group's total capital investment and employment. The six retailing chains were organized as separate business units within an overall structure that also included six business support areas (raw materials, manufacturing plants, logistics, real estate, expansion, and international) and nine corporate departments or areas of responsibility (see Exhibit 11). In effect, each of the chains operated independently and was responsible for its own strategy, product design, sourcing and manufacturing, dishibution, image, personnel, and financial results, while group management set the strategic vision of the group, coordinated the activities of the concepts, and provided them with administrative and various other services. Coordination across the chains had deliberately been limited but had increased somewhat, particularly in the areas of real estate and expansion, as lnditex had recently moved toward opening up some multichain locations. More broadly, the experience of the older, better-established chains, particularly Zara, had helped accelerate the expansion of the newer ones. Thus Oysho, the lingerie chain, drew 75% of its human resources from the other chains and had come to operate stores in seven European markets within six months of its launch in September 2001. Top corporate managers, who were all Spanish, saw the role of the corporate center as a \"strategic controller\" involved in setting the corporate strategy, approving the business strategies of the individual chains, and controlling their performance rather than as an \"operator\" functionally involved in running the chains. Their ability to control performance down to the local store level was based on standardized reporting systems that focused on (like-for-like) sales growth, earnings before interest and taxes (EBIT) margin, and return on capital employed. CEO Castellano looked at key performance metrics once a week, while one of his direct reports monitored them on a daily basis. Recent Governance Changes Inditex's initial public offering (IPO) in May 2001 had sold 26% of the company's shares to the public, but founder Amancio Ortega retained a stake of more than 60%. Since lnditex generated substantial free cash ow (some of which had been used to make portfolio investments in other lines of business), the IPO was thought to be motivated primarily by Ortega's desire to put the company on a firm footing for his eventual retirement and the transition to a new top management team. Also in 2001, lnditex made progress toward implementing a social strategy involving dialogue with employees, suppliers, subcontractors, nongovernmental organizations, and local communities. Immediate initiatives included approval of an internal code of conduct, the establishment of a corporate responsibility department, social audits of supplier and external workshops in Spain and Morocco, pilot developmental projects in Venezuela and Guatemala, and the joining, in August 2001, of the Global Compact, an initiative headed by Kofi Annan, Secretary General of the United Nations, that aimed to improve global companies' social performance. Zara's Business System Zara was the largest and most internationalized of lnditex's chains. At the end of 2001, it operated 507 stores in countries around the world, including Spain (40% of the total number for lnditex), with 488,400 square meters of selling area (74% of the total) and employing 1,050 million of the company's capital (72% of the total), of which the store network accounted for about 80%. During scal year 2001, it had posted EBIT of 441 million (85% of the total) on sales of 2,477 million (76% of the total}. While Zara's share of the group's total sales was expected to drop by two or three percentage points each year, it would continue to be the principal driver of the group's growth for some time to come, and to play the lead role in increasing the share of Inditex's sales accounted for by international operations. Zara completed its rollout in the Spanish market by 1990, and began to move overseas around that time. It also began to make major investments in manufacturing logistics and IT, including establishment of a just-in-time manufacturing system, a 130,000-square-meter warehouse close to corporate headquarters in Arteixo, outside La Corua, and an advanced telecommunications system to connect headquarters and supply, production, and sales locations. Development of logistical, retail, financial, merchandising, and other information systems continued through the 1990s, much of it taking place internally. For example, while there were many logistical packages on the market, Zara's unusual requirements mandated intemal development. The business system that had resulted (see Exhibit 12) was particularly distinctive in that Zara manufactured its most fashionsensitive products internally. (The other lnditex chains were too small to justify such investments but generally did emphasize reliance on suppliers in Europe rather than farther away.) Zara's designers continuously tracked customer preferences and placed orders with internal and external suppliers. About 11,000 distinct items were produced during the yearseveral hundred thousand SKUs given variations in color, fabric, and sizescompared with 2,0004,000 items for key competitors. Production took place in small batches, with vertical integration into the manufacture of the most time-sensitive items. Both internal and external production flowed into Zara's central distribution center. Products were shipped directly from the central distribution center to well-located, attractive stores twice a week, eliminating the need for warehouses and keeping inventories low. Vertical integration helped reduce the \"bullwhip effect"the tendency for uctuations in final demand to get amplified as they were transmitted back up the supply chain. Even more importantly, Zara was able to originate a design and have finished goods in stores within four to five weeks in the case of entirely new designs, and two weeks for modifications (or restocking) of existing products. In contrast, the traditional indusin model might involve cycles of up to six months for design and three months for manufacturing. The short cycle time reduced working capital intensity and facilitated continuous manufacture of new merchandise, even during the biannual sales periods, letting Zara commit to the bulk of its product line for a season much later than its key competitors (see Exhibit 13). Thus, Zara undertook 35% of product design and purchases of raw material, 40/o50% of the purchases of finished products from external suppliers, and 85% of the in-house production after the season had started, compared with only 0%20% in the case of traditional retailers. But while quick response was critical to Zara's superior performance, the connection between the two was not automatic. World Co. of Japan, perhaps the only other apparel retailer in the world with comparable cycle times, provided a counterexample. It, too, had integrated backward into (domestic) manufacturing, and had achieved gross margins comparable to Zara's.15 But World Cofs net margins remained stuck at around 2% of sales, compared with 10% in the case of Zara, largely because of selling, general, and administrative expenses that swallowed up about 40% of its revenues, versus about 20% for Zara. Different choices about how to exploit quick-response capabilities underlay these differences in performance. World Co. served the relatively depressed Japanese market, appeared to place less emphasis on design, had an unprofitable contract manufacturing arm, supported about 40 brands with distinct identities for use exclusively within its own store network (smaller than Zara's), and operated relatively small stores, averaging less than 100 square meters of selling area. Zara had made very different choices along these and other dimensions. Design Each of Zara's three product linesfor women, men, and childrenhad a creative team consisting of designers, sourcing specialists, and product development personnel. The creative teams simultaneously worked on products for the current season by creating constant variation, expanding on successful product items and continuing in-season development, and on the following season and year by selecting the fabrics and product mix that would be the basis for an initial collection. Top management stressed that instead of being run by maestros, the design organization was very at and focused on careful interpretation of catwalk trends suitable for the mass market. Zara created two basic collections each year that were phased in through the fall/ winter and spring/summer seasons, starting in July and January, respectively. Zara's designers attended trade fairs and ready-to-wear fashion shows in Paris, New York, London, and Milan, referred to catalogs of luxury brand collections, and worked with store managers to begin to develop the initial sketches for a collection close to nine months before the start of a season. Designers then selected fabrics and other complements. Simultaneously, the relative price at which a product would be sold was determined, guiding further development of samples. Samples were prepared and presented to the sourcing and product development personnel, and the selection process began. As the collection came together, the sourcing personnel identified production requirements, decided whether an item would be insourced or outsourced, and set a timeline to ensure that the initial collection arrived in stores at the start of the selling season. The process of adapting to trends and differences across markets was more evolutionary, ran through most of the selling season, and placed greater reliance on high-frequency information. Frequent conversations with store managers were as important in this regard as the sales data captured by Zara's IT system. Other sources of information included industry publications, TV, lntemet, and film content; trend spotters who focused on venues such as university campuses and discotheques; and even Zara's young, fashion-conscious staff. Product development personnel played a key role in linking the designers and the stores, and were often from the country in which the stores they dealt with were located. On average, several dozen items were designed each day, but only slightly more than one-third of them actually went into production. Time permitting, very limited volumes of new items were prepared and presented in certain key stores and produced on a larger scale only if consumer reactions were unambiguously positive. As a result, failure rates on new products were supposed to be only 1%, compared with an average of 10% for the sector. Learning by doing was considered very important in achieving such favorable outcomes. Overall, then, the responsibilities of Zara's design teams transcended design, narrowly defined. The teams also continuously tracked customer preferences and used information about sales potential based, among other things, on a consumption information system that supported detailed analysis of product life cycles, to transmit repeat orders and new designs to internal and external suppliers. The design teams thereby bridged merchandising and the back end of the production process. These functions were generally organized under separate management teams at other apparel retailers. Sourcing 6' Manufacturing Zara sourced fabric, other inputs, and nished products from external suppliers with the help of purchasing offices in Barcelona and Hong Kong, as well as the sourcing personnel at headquarters. While Europe had historically dominated Zara's sourcing patterns, the recent establishment of three companies in Hong Kong for purposes of purchasing as well as trend-spotting suggested that sourcing from the Far East, particularly China, might expand substantially. About one-half of the fabric purchased was \"gray\" (undyed) to facilitate in-season updating with maximum exibility. Much of this volume was funneled through Comditel, a 1009'o-owned subsidiary of Inditex, that dealt with more than 200 external suppliers of fabric and other raw materials. Comditel managed the dyeing, patterning, and finishing of gray fabric for all of lnditex's chains, not just Zara, and supplied finished fabric to external as well as in-house manufacturers. This process, reminiscent of Benetton's, meant that it took only one week to finish fabric. Further down the value chain, about 40% of finished garments were manufactured internally, and of the remainder, approximately two-thirds of the items were sourced from Europe and North Africa and one-third from Asia. The most fashionable items tended to be the riskiest and therefore were the ones that were produced in small lots internally or under contract by suppliers who were located close by, and reordered if they sold well. More basic items that were more price-sensitive than time- sensitive were particularly likely to be outsourced to Asia, since production in Europe was typically 15%20/o more expensive for Zara. About 20 suppliers accounted for 70% of all external purchases. While Zara had long-term ties with many of these suppliers, it minimized formal contractual commitments to them. Internal manufacture was the primary responsibility of 20 fully owned factories, 18 of them located in and around Zara's headquarters in Arteixo. Room for growth was provided by vacant lots around the principal manufacturing complex and also north of La Corua and in Barcelona. Zara's factories were heavily automated, specialized by garment type, and focused on the capital-intensive parts of the production processpattern design and cuttingas well as on final finishing and inspection. Vertical integration into manufacturing had begun in 1980, and starting in 1990', significant investments had been made in installing a just-in-time system in these factories in cooperation with Toyotaone of the first experiments of its kind in Europe. As a result, employees had had to learn how to use new machines and work in multifunctional teams. Even for the garments that were manufactured in-house, cut garments were sent out to about 450 workshops, located primarily in IGalicia and across the border in northern Portugal, that performed the labor-intensive, scale-insensitive activity of sewing. These workshops were generally small operations, averaging about 2030 employees (although a few employed more than 100 people apiece), which specialized by product type. As subcontractors, they generally had long-term relations with Zara. Zara accounted for most if not all of their production; provided them with technology, logistics, and financial support,- paid them prearranged rates per nished garment; carried out inspections onsite; and insisted that they comply with local tax and labor legislation. The sewn garments were sent back from the workshops to Zara's manufacturing complex, where they were inspected, ironed, folded, bagged, and ticketed before being sent on to the adjoining distribution center. Distribution Like each of lnditex's chains, Zara had its own centralized distribution system. Zara's system consisted of an approximately 400,000-squaremeter facility located in Arteixo and much smaller satellite centers in Argentina, Brazil, and Mexico that consolidated shipments from Arteixo. All of Zara's merchandise, from internal and external suppliers, passed through the distribution center in Arteixo, which operated on a dual-shift basis and featured a mobile tracking system that docked hanging garments in the appropriate barcoded area on carousels capable of handling 45,000 folded garments per hour. As orders were received from hand-held computers in the stores (twice a week during regular periods, and thrice weekly during the sales season), they were checked in the distribution center and, if a particular item was in short supply, allocation decisions were made on the basis of historical sales levels and other considerations. Once an order had been approved, the warehouse issued the lists that were used to organize deliveries. Lorena Alba, lnditex's director of logistics, regarded the warehouse as a place to move merchandise rather than to store it. According to her, "The vast majority of clothes are in here only a few hours,\" and none ever stayed at the distribution center for more than three days. Of course, the rapidly expanding store network demanded constant adjustment to the sequencing and size of deliveries as well as their routing. The most recent revamp had been in January 2002, when Zara had started to schedule shipments by time zone. In the early morning while European store managers were still stocktaking, the distribution center packed and shipped orders to the Americas, the Middle East, and Asia; in the afternoon, it focused on the European stores. The distribution center generally ran at half its rated capacity, but surges in demand, particularly during the start of the two selling seasons in January and Iuly, boosted utilization rates and required the hiring of several hundred temporary workers to complement close to 1,000 permanent employees. Shipments from the warehouse were made twice a week to each store via third-party delivery services, with shipments two days a week to one part of the store network and two days a week to the other. Approximately 75% of Zara's merchandise by weight was shipped by truck by a third- party delivery service to stores in Spain, Portugal, France, Belgium, the United Kingdom, and parts of Germany. The remaining 25% was shipped mainly by air via KLM and DHL from airports in Santiago de Compostela (a major pilgrimage center in Galicia} and Porto in Portugal. Products were typically delivered within 2436 hours to stores located in Europe and within 2448 hours to stores located outside Europe. Air shipment was more expensive, but not prohibitively so. Thus, one industry participant suggested that air freight from Spain to the Middle East might cost 3%5% of FOB price (compared with 1.5% for sea freight) and, along with a 1.5% landing charge, a 1% finance charge, miscellaneous expenses, and (generally) a 4% customs duty, bring the landed markup on FOB price to 12% or so. In the case of the United States, a 20/o25/o landed markup seemed a better approximation because of tariffs of up to 12% as well as other added cost elements. Despite Zara's historical success at scaling up its distribution system, observers speculated that the centralized logistics model might ultimately be subject to diseconomies of scalethat what worked well with 1,000 stores might not work with 2,000 stores. In an attempt to increase capacity, Zara was beginning construction of a second distribution center, at Zaragoza, northeast of Madrid. This second major distribution facility, to be started up in summer 2003, would add 120,000 square meters of warehouse space at a cost of 88 million close to the local airport and with direct access to the railway and road network as well. Retailing Zara aimed to offer fresh assortments of designer-style garments and accessoriesshoes, bags, scarves, jewelry and, more recently, toiletries and cosmeticsfor relatively low prices in sophisticated stores in prime locations in order to draw masses of fashion-conscious repeat customers. Despite its tapered integration into manufacturing, Zara placed more emphasis on using backward vertical integration to be a very quick fashion follower than to achieve manufacturing efficiencies by building up signicant forward order books for the upstream operations. Production rims were limited and inventories strictly controlled even if that meant leaving demand unsatisfied. Both Zara's merchandising and store operations helped to reinforce these upstream policies. Merchandising Zara's product merchandising policies emphasized broad, rapidly changing product lines, relatively high fashion content, and reasonable but not excessive physical quality: \"clothes to be worn 10 times,\" some said. Product lines were segmented into women's, men's, and children's, with further segmentation of the women's line, considered the strongest, into three sets of offerings that varied in terms of their prices, fashion content, and age targets. Prices, which were determined centrally, were supposed to be lower than competitors' for comparable products in Zara's major markets, but percentage margins were expected to hold up not only because of the direct efciencies associated with a shortened, vertically integrated supply chain but also because of significant reductions in advertising and markdown requirements. Zara spent only 0.3% of its revenue on media advertising, compared with 3%4/o for most specialty retailers. Its advertising was generally limited to the start of the sales period at the end of the season, and the little that was undertaken did not create too strong a presence for the Zara brand or too specific an image of the \"Zara Woman\" or the \"Zara Girl\" (unlike the \"Mango Girl\" of Spanish competitor Mango). These choices reected concerns about overexposure and lock-in as well as limits on spending. Nor did Zara exhibit its merchandise at the ready-to-wear fashion shows: its new items were first displayed in its stores. The Zara name had nevertheless developed considerable drawing power in its major markets. Thus by the mid-1990s, it had already become one of the three clothing brands of which customers were most aware in its home market of Spain, with particular strengths among women between ages of 18 and 34 from households with middle to middle-high income. Zara's drawing power reected the freshness of its offerings, the creation of a sense of scarcity and an attractive ambience around them, and the positive word of mouth that resulted. Freshness was rooted in rapid product turnover, with new designs arriving in each twice-weekly shipment. Devout Zara shoppers even knew which days of the week delivery trucks came into stores, and shopped accordingly. About three-quarters of the merchandise on display was changed every three to four weeks, which also corresponded to the average time between visits given estimates that the average Zara shopper visited the chain 17 times a year, compared with an average figure of three to four times a year for competing chains and their customers. Attractive stores, outside and inside, also helped. Luis Blanc, one of Inditex's international directors, summarized some of these additional inuences: We invest in prime locations. We place great care in the presentation of our storefronts. That is how we project our image. We want our clients to enter a beautiful store, where they are offered the latest fashions. But most important, we want our customers to understand that if they like something, they must buy it now, because it won't be in the shops the following week. It is all about creating a climate of scarcity and opporhrnity.\" For the customers who did walk in through the door, the rapid turnover obviously created a sense of \"buy now because you won't see this item later.\" In addition, the sense of scarcity was reinforced by small shipments, display shelves that were sparsely stocked, limits of one month on how long individual items could be sold in the stores, and a degree of deliberate undersupply. Of course, even though Zara tried to follow fashions instead of betting on them, it did make some design mistakes. These were relatively cheap to reverse since there was typically no more than two to three weeks of forward cover for any risky item. Items that were slow to sell were immediately apparent and were ruthlessly weeded out by store managers with incentives to do so. Returns to the distribution center were either stripped to and sold at other Zara stores or disposed of through a small, separate chain of close-out stores near the distribution center. The target was to minimize the inventories that had to be sold at marked-down prices in Zara stores during the sales period that ended each season. Such markdowns had a significant impact on apparel retailers' revenue bases: in the United States, for example, women's apparel stores averaged markdowns of 309'0-plus of (potential) revenues in the mid-19905.\" Very rough estimates for Western Europe indicated markdowns that were smaller but still very significant. Zara was estimated to generate 15952091: of its sales at marked-down prices, compared with 30%4D% for most of its European peers. Additionally, since Zara had to move less of its merchandise during such periods, the percentage markdowns on the items affected did not have to be as largeperhaps only half as much as the 30% average for other European apparel retailers, according to Zara's management. Store operations Zara's stores functioned as both the company's face to the world and as information sources. The stores were typically located in highly visible locations, often including the premier shopping streets in a local market (e.g., the Champs Elyses in Paris, Regent Street in London, and Fifth Avenue in New York) and upscale shopping centers. Zara had initially purchased many of its store sites, particularly in Spain, but had preferred long-term leases (for 10 to 20' years) since the mid-19905, except when purchase was necessary to secure access to a very attractive site. [nditex's balance sheet valued the property that it owned (mostly Zara stores) at about 400 million on the basis of historical costs, but some analysts estimated that the market value of these store properties might be four or ve times that amount. Zara actively managed its portfolio of stores. Stores were occasionally relocated in response to the evolution of shopping districts and traffic patterns. More frequently, older, smaller stores might be relocated as well as updated (and typically expanded) in new, more suitable sites. The average size of the stores had gradually increased as Zara improved the breadth and strength of its customer pull. Thus, while the average size of Zara stores at the beginning of fiscal year 2001 was 910 square meters, the average size of the stores opened during the year was 1,376 square meters. In addition, Zara invested more heavily and more frequently than key competitors in refurbishing its store base, with older stores getting makeovers every three to four years. Zara also relied on significant centralization of store window displays and interior presentations in using the stores to promote its market image. As the season progressed and product offerings evolved, ideas about consistent looks for windows and for interiors in terms of themes, color schemes, and product presentation were prototyped in model window and store areas in the headquarters building in Arteixo. These ideas were principally carried to the stores by regional teams of window dressers and interior coordinators who visited each store every three weeks. But some adaptation was permitted and even planned for in the look of a store. For example, while all Zara in- store employees had to wear Zara clothes while working in the stores, the uniforms that the sales assistants were required to wear might vary across different Zara stores in the same city to reect socioeconomic differences in the neighborhoods in which they were located. Uniforms were selected twice a season by store managers from the current season's collection and submitted to headquarters for authorization. The size, location, and type of Zara store affected the number of employees in it. The number of sales assistants in each store was determined on the basis of variables such as sales volume and selling area. And the larger stores with the full complement of stores-within-storeswomen's, men's, and children'stypically had a manager for each section, with the head of the women's section also serving as store manager. Personnel were selected by the store manager in consultation with the section manager concerned. Training was the responsibility of the section manager and was exclusively on-the-job. After the first 15 days, the trainee's suitability for the post was reviewed. Personnel assessment was, once again, the job of the store manager. In addition to overseeing in-store personnel, store managers decided which merchandise to order and which to discontinue, and also transmitted customer data and their own sense of inflection points to Zara's design teams. In particular, they provided the creative teams with a sense of latent demand for new products that could not be captured through an automated sales-tracking system. The availability of store managers capable of handling these responsibilities was, according to CEO Castellano, the single most important constraint on the rate of store additions. Zara promoted approximately 90% of its store managers from within and had generally experienced low store manager turnover. Once an employee was selected for promotion, his or her store, together with the human resources department, developed a comprehensive training program that included training at other stores and a two-week training program, with specialized staff, at Zara's headquarters. Such off-site training fullled important socialization goals as well, and was followed up by periodic supplemental training. Store managers received a xed salary plus variable compensation based primarily on their store's performance, with the variable component representing up to one-half of the total, which made their compensation very incentive-intensive. Since prices were fixed centrally, the store managers' energies were primarily focused on volume and mix. Top management tried to make each store manager feel as if she were running a small business. To this end, clear cost, profit, and growth targets for each store were set, as were regular reporting requirementswith stores' volume metrics being tracked particularly closely at the top of the (relatively flat) managerial hierarchy. Zara's International Expansion At the end of 2001, Zara was by far the most internationalized as well as the largest of Inditex's chains. Zara operated 282 stores in 32 countries outside Spain (55% of the international total for Inditex) and had posted international sales of 1,506 million (86% of Inditex's international sales) during the year. Of its international stores, 186 were located in Europe, 35 in North America, 29 in South America, 27 in the Middle East, and 5 in Iapan. Overall, international operations accounted for 56% of Zara's stores and 61% of its sales in 2001, and had been steadily increasing its shares of those totals. The protability of Zara's operations was not disaggregated geographically but, according to top management, was roughly the same in (the rest of) Europe and the Americas as in Spain. Approximately 80% of the new Zara stores slated to be opened in 2002 were expected to be outside Spain, and lnditex even cited the weight of Zara in the group's total selling area as the principal reason lnditex's sales were increasingly international. But over a longer time frame, Zara faced several important issues regarding its international expansion. Market Selection Zara's international expansion began in 1988 with the opening of a store in Oporto in northern Portugal. In 1989, it opened its first store in New York and in 1990, its first store in Paris. Between 1992 and 1997', it entered about one country per year (at a median distance of about 3,000 kilometers from Spain), so that by the end of this period, there were Zara stores in seven European countries, the United States, and Israel. Since then, countries had been added more rapidly: 16 countries (at a median distance of 5,000 kilometers) in 19981999, and eight countries (at a median distance of less than 2,000 kilometers) in 20002001. Plans for 2002 included entry into Italy, Switzerland, and Finland. Rapid expansion gave Zara a much broader footprint than larger apparel chains: by way of comparison, H&:M added eight countries to its store network between the mid-1980s and 2001, and The Gap added ve. (Exhibit 14 tracks aggregate store additions across all of Inditex's chains.) Inditex's management sometimes described this pattern of expansion as an \"oil stain\" in which Zara would first open a agship store in a major city and, after developing some experience operating locally, add stores in adjoining areas. This pattern of expansion had first been employed in Spain and had been continued in Portugal. The rst store opened in New York was intended as a display window and listening post, but the first store in Paris anchored a pattern of regionaland then nationalexpansion that came to encompass about 30 stores in the Paris area and 67 in France by the end of 2001. Castellano explained the approach: For us it is cheaper to deliver to 67 shops than to one shop. Another reason, from the point of view of the awareness of the customers of Inditex or of Zara, is that it is not the same if we have one shop in Paris compared to having 30 shops in Paris. And the third reason is that when we open a country, we do not have advertising or local warehouse costs but we do have headquarters costs. Similarly, Zara's entry into Greece in 1993 was a springboard for its expansion into Cyprus and Israel. Zara had historically looked for new country markets that resembled the Spanish market, had a minimum level of economic development, and would be relatively easy to enter. To study a specific entry opportunity, a commercial team from headquarters conducted both the macro and micro analysis. Macro analysis focused on local macroeconomic variables and their likely future evolution, particularly in terms of how they would affect the prospects for stores (e.g., tariffs, taxes, legal costs, salaries, and property prices/rents). Micro analysis, performed onsite, focused on sector-specific information about local demand, channels, available store locations, and competitors. The explicitly competitive information that was gathered included data on levels of concentration, the formats that would compete most directly with Zara, and their potential political or legal ability to resist/ retard its entry, as well as local pricing levels. According to Castellano, Zaraunlike its competitors focused more on market prices than on its own costs in forecasting its prices in a particular market. These forecasts were then overlaid on cost estimates, wh

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance