Will S. (age 42) and Mari N. (age 41) Frost are married and live at 426 East

Question:

Will S. (age 42) and Mari N. (age 41) Frost are married and live at 426 East Twin Oaks Road, Sioux Falls, SD 57105. Will is the regional manager for a restaurant chain (Moveable Feast), and Mari is a self-employed architect. They are calendaryear, cash-basis taxpayers.

1. Will’s annual salary from Moveable Feast is $82,000. He also earns an annual bonus. The amount is determined in late December, and Will receives it in January of the next year. Will’s 2012 bonus was $6,000 (received in 2013), and his 2013 bonus was $7,000 (received in 2014). Will is also paid a flat travel allowance of $16,000 per year. The allowance is to cover his expenses in visiting restaurants in his region to conduct inspections, consult with the local managers, and recruit potential hires. Although Will maintains substantiation of his travel, he is not required to account for these expenses to Moveable Feast. Will participates in his employer’s group health insurance plan to which he contributed $3,600 in 2013 for medical coverage. These contributions were made with after-tax dollars. The health plan covers Will, Mari, and their two dependent children. Moveable Feast does not provide any retirement benefits, but it has established a §401(k) plan to enable its employees to make voluntary contributions. Will contributed $10,000 to the plan in 2013. The company provides an office for Will’s use that is located at 110 North Reid Street, Suite 217, Sioux Falls.

2. Besides the business use of his car (see item 3 below), Will’s out-of-pocket employment-related expenses for 2013 are as follows:

Airfare $2,600

Lodging 3,200

Meals 3,400

Entertainment 800

Car rentals, limos, taxis 600

Parking and tolls 300

Subscriptions to trade journals 120

Dues to trade association 80

Business gifts 550

While on business trips in his car, Will was cited for speeding several times and paid related fines totaling $620. Will presented the business gifts in late December to managers of the top 11 restaurants in his region, with each manager receiving a $50 gift card to a national retailer.

3. On March 5, 2012, Will purchased a new Ford Focus for use in his job. The car cost $24,000 (including sales tax), with no trade-in involved. The car was driven 14,000 miles in 2012 and 18,000 in 2013 with usage as follows: 20% for commuting to the office and 80% for business trips. The mileage for 2013 was evenly distributed throughout the year. Will uses the actual operating cost method, and for depreciation purposes, uses 200% declining-balance with a half-year convention. In addition, Will did not claim any §179 expensing or additional first-year depreciation last year when he bought the car. (See Table 3 of the Instructions to Form 4562.) Will’s expenses related to operating the Ford Focus for 2013 are as follows:

Gasoline $2,900

Oil change and lubrication 150

Auto insurance 1,800

Repairs 400

Auto club dues 160

License and registration 120

Interest on car loan 900

4. Mari Frost is a licensed architect who works part time on a consulting basis. Her professional activity code is 541310. Her major clients are real estate developers (both residential and commercial) for whom she prepares structural designs and construction plans. She also advises on building code requirements regarding the renovation and remodeling of existing structures. Mari collected $52,000 in consulting fees during 2013. This total includes a $3,000 payment for work she performed in 2012 and does not include $5,000 she billed in December for work performed in late 2013. In addition, Mari has an unpaid invoice for $6,000 from a client for work done in 2011. This client was convicted of arson in August 2013 and is now serving a five-year sentence in state prison. Mari feels certain that she will never collect the $6,000 she is owed.

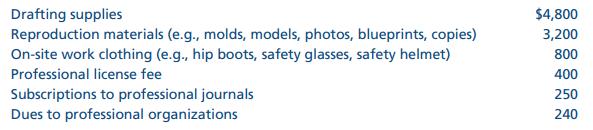

Mari does her work at the client’s premises or in her office at home (see item 5 below). Her business expenses for 2013 are as follows:

In addition, Mari drove the family Acura (purchased on June 7, 2012) 940 miles on her job assignments. She uses the standard mileage method to deduct business costs related to the Acura. During 2013, Mari drove the car a total of 10,000 miles.

5. When the Frosts purchased their home on February 2, 2012, they set aside 300 square feet (out of a total of 2,400 square feet) of living space for Mari’s office. As of January 1, 2013, the home had an adjusted basis of $240,000 for purposes of line 36 of Form 8829 (of which $40,000 is attributable to the land)—the fair market value of the property is in excess of this amount. Relevant information concerning the residence for all of 2013 follows:

The cost of Mari’s office furniture and equipment was previously deducted under §179 in the years these assets were acquired. On June 29, 2013, she purchased a fireproof file cabinet for $800 to safeguard the blueprints of her structural designs and construction plans. If possible, Mari prefers to avoid depreciating capital expenditures.

6. One of Mari’s clients was interested in building a shopping center on a tract of land Mari owned in Lincoln County. Mari inherited the property from her uncle when he died on June 6, 1993. At that time, the land was worth $40,000. It has since been rezoned for commercial use and has a current value of $200,000. On February 10, 2013, Mari exchanged the Lincoln County parcel for a similar tract in Minnehaha County (worth $190,000) and cash of $10,000.

7. On September 2, 2013, Mari sold a tract of land in McCook County to a farmer who owned the adjoining property. The land was inherited from the same uncle who died in 1993 and was worth $30,000 on June 6, 1993. Under the terms of the sale, Mari received cash of $20,000 and four notes receivable (to be paid at one-year intervals) that each call for the payment of $25,000 plus simple interest of 8%. To the extent allowed by law, Mari wants to defer recognition of gain as long as possible.

8. In early 2012, Will learned that one of his restaurant managers, Carrie Jones, was suffering domestic abuse at the hands of her husband Steve. When Steve also started to abuse their 5-year-old daughter, Carrie decided it was time for her and her daughter to get away. Before they left on April 14, 2012, Will loaned Carrie $5,500 to help them relocate. Will had her sign an interest-free note due in one year. Will never heard from Carrie again. In late 2013, Will learned that Steve tracked down Carrie and their daughter and killed both of them before committing suicide. Given these tragic circumstances, Will has no expectation that the loan will ever be repaid.

9. On August 5, 2011, Will purchased 1,000 shares of Farmer’s Markets America (FMA) common stock for $16 a share as part of its initial public offering. The corporation was formed to establish and operate farmers’ markets in mid-size cities throughout the United States. Although some market locations were profitable, the venture as a whole proved to be a failure. In November 2013, FMA’s remaining assets were seized by its creditors, and FMA stock became worthless.

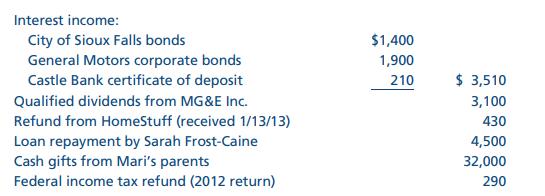

10. Besides the items previously noted, the Frosts had the following receipts for 2013:

In December 2012, the Frosts made major purchases of household items (e.g., appliances, furniture) at HomeStuff (a discount big box store). They called the manager when they realized they did not receive the advertised sale price. Consequently, the store corrected the mistake and sent a $430 refund. Four years ago when his sister Sarah married, Will lent her $4,000 to help pay for her honeymoon. Will was pleasantly surprised when Sarah paid him back (plus interest of $500) on December 20, 2013. On March 20 of each year, Mari’s parents send a generous gift of cash as a birthday present. Just as she has done for the past seven years, Mari immediately invested the cash in her kids’ § 529 college savings plans.

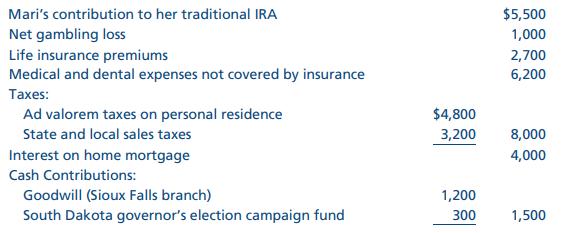

11. In addition to the items already noted, the Frosts had the following expenditures for 2013:

The $1,000 net gambling loss for 2013 is the difference between the Frosts’ gambling winnings of $1,200 and losses of $2,200. The life insurance premiums relate to the universal life insurance policies that Will and Mari own. The first beneficiary on both policies is the other spouse, with the second beneficiaries being the children. Included in the medical expenses are $1,200 incurred in 2012, which was paid in early February 2013. The Frosts can substantiate the $3,200 in sales taxes paid based on their purchase receipts for the year. The local sales tax rate in Sioux Falls is 2%. [HINT: Be sure to check to see if the Optional Sales Tax Tables provide the Frosts with a greater deduction.] Mari contributed to the governor’s campaign fund because she thinks his influence is key in getting the Lincoln County land rezoned for commercial use (see item 6 above).

12. The Frosts maintain a household that includes their two children, Austin (age 16) and Emma (age 19). Austin is a junior in high school and a talented wrestler. In hopes of competing at the state tournament, all of his free time is consumed with weight training and wrestling practices. Emma graduated from high school on June 7, 2013, and is undecided about college. Emma is an accomplished vocalist and during 2013 earned $7,200 performing at various events (e.g., weddings, funerals). She placed most of her earnings in a savings account and kept only a small amount to spend on herself.

13. Will’s Form W–2 from Moveable Feast shows $13,800 withheld for Federal income tax. The Frosts have made total quarterly income tax payments of $4,000.

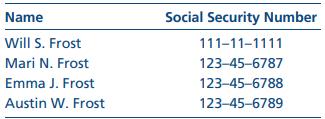

14. Relevant Social Security numbers are as follows:

Requirements

Prepare an income tax return (with appropriate schedules) for the Frosts for 2013, using the following guidelines:

• The Frosts choose to file a joint income tax return.

• The Frosts do not wish to contribute to the Presidential Election Campaign Fund.

• The Frosts do not own any foreign bank accounts or other investments.

• The Frosts prefer to receive any refund of overpaid taxes.

• The taxpayers are preparing their own return (i.e., no preparer is involved).

• For the past several years, the Frosts have itemized their deductions from AGI instead of using the standard deduction.

• The taxpayers have the necessary substantiation (e.g., records, receipts) to support all transactions reported in their tax return.

• Make necessary assumptions for information not given in the problem but needed to complete the return.

Step by Step Answer:

It appears that you are looking for a detailed preparation of a 2013 US federal income tax return for Will S Frost and Mari N Frost This type of tax preparation requires an extensive stepbystep calcul...View the full answer

South Western Federal Taxation 2015

ISBN: 9781305310810

38th Edition

Authors: William H. Hoffman, William A. Raabe, David M. Maloney, James C. Young