EXAMPLE OF EARNED VALUE The Project Management Institute, the largest professional organization of project management professionals in

Question:

EXAMPLE OF EARNED VALUE The Project Management Institute, the largest professional organization of project management professionals in the world, has developed a simple example of the logic underlying earned value assessment for a project. It demonstrates in the following steps the calculation of the more relevant components of earned value and shows how these steps fit together to contribute an overall understanding of earned value.

Earned value is a management technique that relates resource planning to schedules and to technical cost and schedule requirements. All work is planned, budgeted, and scheduled in time-phased planned value increments constituting a cost and schedule measurement baseline. There are two major objectives of an earned value system: to encourage contractors to use effective internal cost and schedule management control systems, and to permit the customer to be able to rely on timely data produced by those systems for determining product-oriented contract status.

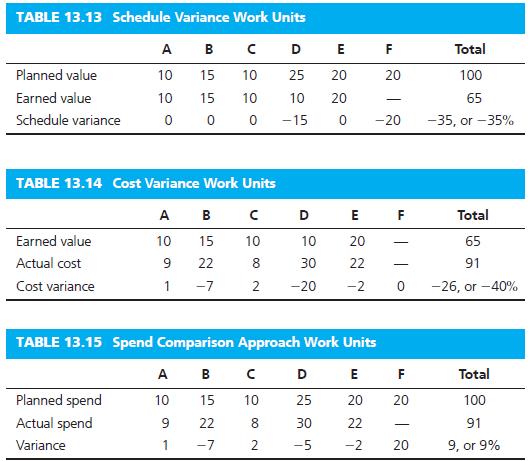

Baseline. The baseline plan in Table 13.12 shows that six work units (A–F) would be completed at a cost of $100 for the period covered by this report.

Schedule Variance. As work is performed, it is “earned” on the same basis as it was planned, in dollars or other quantifiable units such as labor hours. Planned value compared with earned value measures the dollar volume of work planned versus the equivalent dollar volume of work accomplished. Any difference is called a schedule variance. In contrast to what was planned, Table 13.13 shows that work unit D was not completed and work unit F was never started, or $35 of the planned work was not accomplished. As a result, the schedule variance shows that 35% of the work planned for this period was not done.

Cost Variance. Earned value compared with the actual cost incurred (from contractor accounting systems) for the work performed provides an objective measure of planned and actual cost. Any difference is called a cost variance. A negative variance means more money was spent for the work accomplished than was planned. Table 13.14 shows the calculation of cost variance.

The work performed was planned to cost $65 and actually cost $91. The cost variance is 40%.

Spend Comparison. The typical spend comparison approach, whereby contractors report actual expenditures against planned expenditures, is not related to the work that was accomplished.

Table 13.15 shows a simple comparison of planned and actual spending, which is unrelated to work performed and therefore not a useful comparison. The fact that the total amount spent was $9 less than planned for this period is not useful without the comparisons with work accomplished.

Use of Earned Value Data. The benefits to project management of the earned value approach come from the disciplined planning conducted and the availability of metrics that show real variances from the plan in order to generate necessary corrective actions.17

Step by Step Answer:

Project Management Achieving Competitive Advantage

ISBN: 9780134730714

5th Edition

Authors: Jeffrey K. Pinto