Answered step by step

Verified Expert Solution

Question

1 Approved Answer

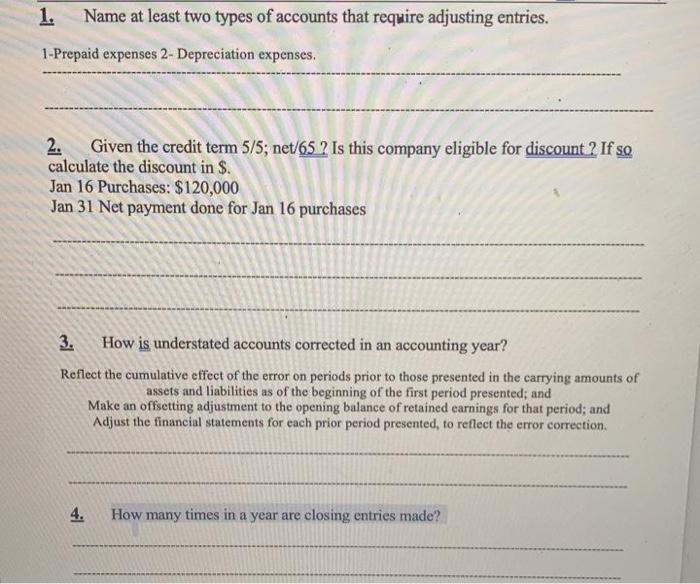

1. Name at least two types of accounts that require adjusting entries. 1-Prepaid expenses 2- Depreciation expenses. 2. Given the credit term 5/5; net/65 2

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost management a strategic approach

Authors: Edward J. Blocher, David E. Stout, Gary Cokins

5th edition

73526940, 978-0073526942