Question

1.SI received a $ 100 million loan from the bank for the construction of the new stadium. Transaction costs of $ 2 million were expensed

1.SI received a $ 100 million loan from the bank for the construction of the new stadium. Transaction costs of $ 2 million were expensed during the year as a finance cost. In 2023, SIi nvested cash from the bank loan until needed for construction in shares of High Tech Incorporated. SI purchased 2% of

2. SI started construction of the new sports stadium in March 2023. The estimated completion date was December 31, 2025. Costs capitalized in 2023 were $ 15 million and included materials, labour and variable overhead. Costs expensed in 2023 were $ 2 million in interest. In July 2023, a strike occurred that shut down construction for months and will delay the operating of the new stadium.

3. SI issued $ 1,000,000 of term preferred shares to two of the owners. The cumulative dividend of 10% and a mandatory repayment date in 10 years. Any unpaid dividends must be repaid at that date. These shares were recorded on the statement of financial position as debt, and the shares and will sell them when cash is needed over the next year and a half. These shares were classified as FVTOCI

4.SI has $ 10 million of unused losses. It has decided that the future is too uncertain to recognized the benefit of these losses. This industry has a history of strikes

5. SI uses the Black Scholes model to determine the fair value. Since SIs shares are not frequently traded, it does not measure stock price volatility. SIs stock option plan vests annually over a five-year period. The entire stock option expense recognized in period stock option is granted. Any forfeitures are recognized when they occur.

6. SI issued common shares during the year. Share issue costs of $ 1 million were expensed as a financing cost.

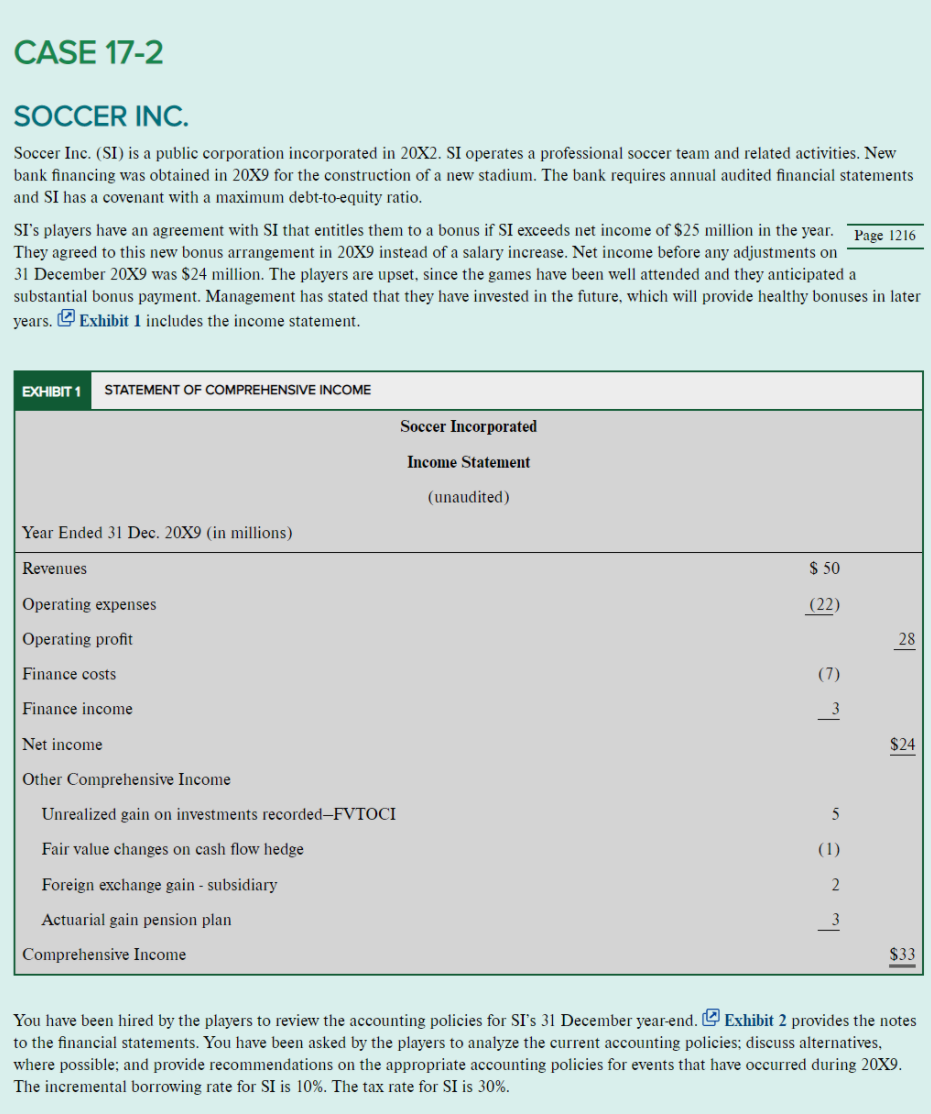

SOCCER INC. Soccer Inc. (SI) is a public corporation incorporated in 20X2. SI operates a professional soccer team and related activities. New bank financing was obtained in 20X9 for the construction of a new stadium. The bank requires annual audited financial statements and SI has a covenant with a maximum debt-to-equity ratio. SI's players have an agreement with SI that entitles them to a bonus if SI exceeds net income of $25 million in the year. They agreed to this new bonus arrangement in 20X9 instead of a salary increase. Net income before any adjustments on Page 1216 31 December 20X9 was $24 million. The players are upset, since the games have been well attended and they anticipated a substantial bonus payment. Management has stated that they have invested in the future, which will provide healthy bonuses in later years. Exhibit 1 includes the income statement. You have been hired by the players to review the accounting policies for SI's 31 December year-end. (\$) Exhibit 2 provides the notes to the financial statements. You have been asked by the players to analyze the current accounting policies; discuss alternatives, where possible; and provide recommendations on the appropriate accounting policies for events that have occurred during 20X9. The incremental borrowing rate for SI is 10%. The tax rate for SI is 30%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Of The Drug Enforcement Administrations Controls Over Seized And Collected Drugs

Authors: Office Of Inspector General, U.S. Department Of Justice, Penny Hill Press

1st Edition

1537075683, 978-1537075686