Answered step by step

Verified Expert Solution

Question

1 Approved Answer

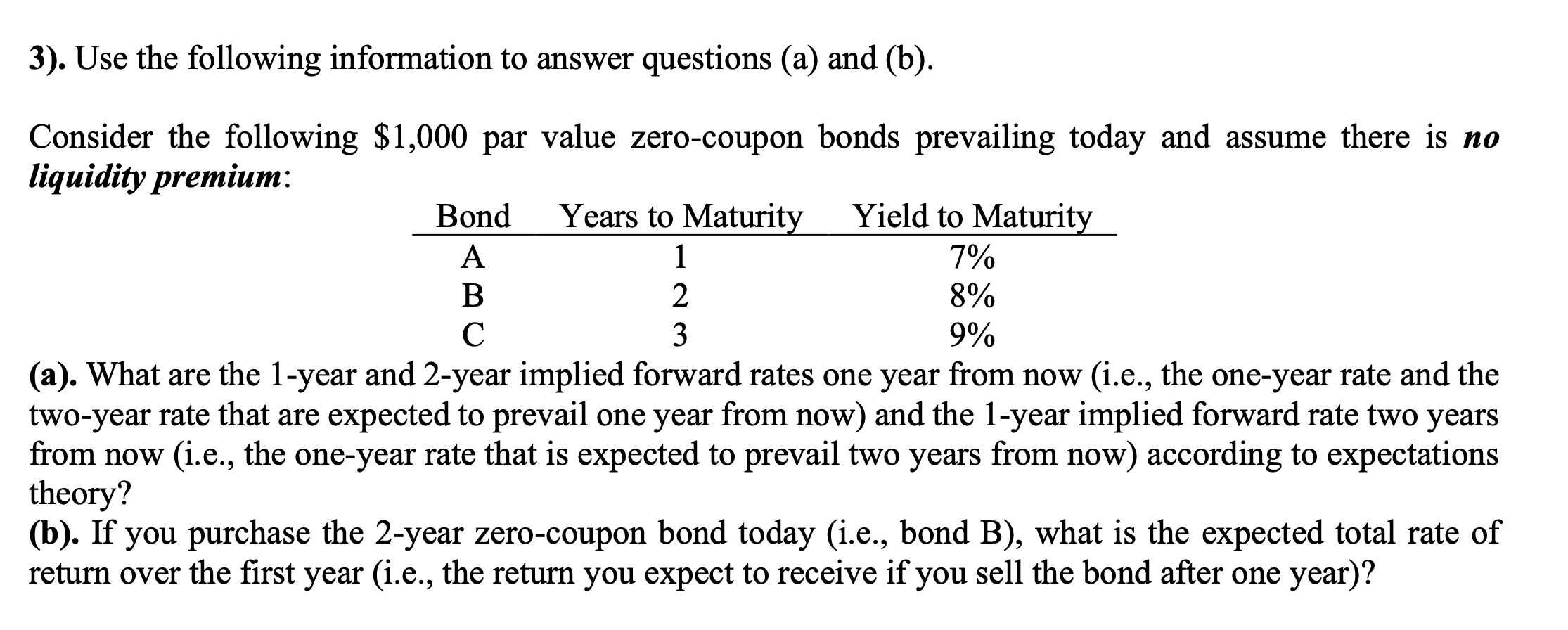

3). Use the following information to answer questions (a) and (b). Consider the following $1,000 par value zero-coupon bonds prevailing today and assume there is

3). Use the following information to answer questions (a) and (b). Consider the following $1,000 par value zero-coupon bonds prevailing today and assume there is no liquidity premium: (a). What are the 1-year and 2-year implied forward rates one year from now (i.e., the one-year rate and the two-year rate that are expected to prevail one year from now) and the 1-year implied forward rate two years from now (i.e., the one-year rate that is expected to prevail two years from now) according to expectations theory? (b). If you purchase the 2-year zero-coupon bond today (i.e., bond B), what is the expected total rate of return over the first year (i.e., the return you expect to receive if you sell the bond after one year)

3). Use the following information to answer questions (a) and (b). Consider the following $1,000 par value zero-coupon bonds prevailing today and assume there is no liquidity premium: (a). What are the 1-year and 2-year implied forward rates one year from now (i.e., the one-year rate and the two-year rate that are expected to prevail one year from now) and the 1-year implied forward rate two years from now (i.e., the one-year rate that is expected to prevail two years from now) according to expectations theory? (b). If you purchase the 2-year zero-coupon bond today (i.e., bond B), what is the expected total rate of return over the first year (i.e., the return you expect to receive if you sell the bond after one year)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing Finance

Authors: CMI Books

1st Edition

1781252181, 978-1781252185