Answered step by step

Verified Expert Solution

Question

1 Approved Answer

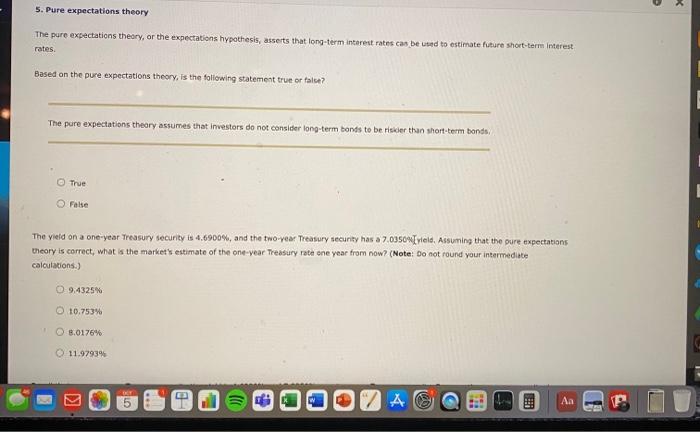

5. Pure expectations theory The pure exfectations theory, or the expectations hypothesis, asserts that long-tirm interent rates cas be uted to estimate future short-term interest.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

R In Finance And Economics A Beginners Guide

Authors: Abhay Kumar Singh, David Edmund Allen

1st Edition

9813144467, 978-9813144460