Answered step by step

Verified Expert Solution

Question

1 Approved Answer

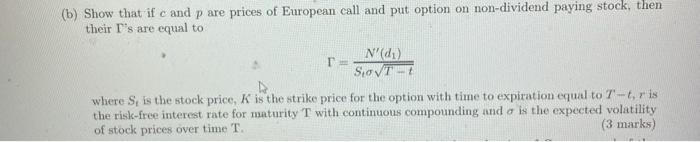

(b) Show that if c and p are prices of European call and put option on non-dividend paying stock, then their I's are equal to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The New Finance Overreaction Complexity And Their Consequences

Authors: Robert A. Haugen

4th International Edition

0132775875, 9780132775878