Question: Hello, my question is for number 3. 3. Should this report presumably increase the reliability of the financial statements? Why? I put the answer together

Hello, my question is for number 3. 3. Should this report presumably increase the reliability of the financial statements? Why?

I put the answer together finding bits and pieces from the internet. Copy and pasted. I would like it to sound original but to point of the question.

Can you help me with this?

Project Questions

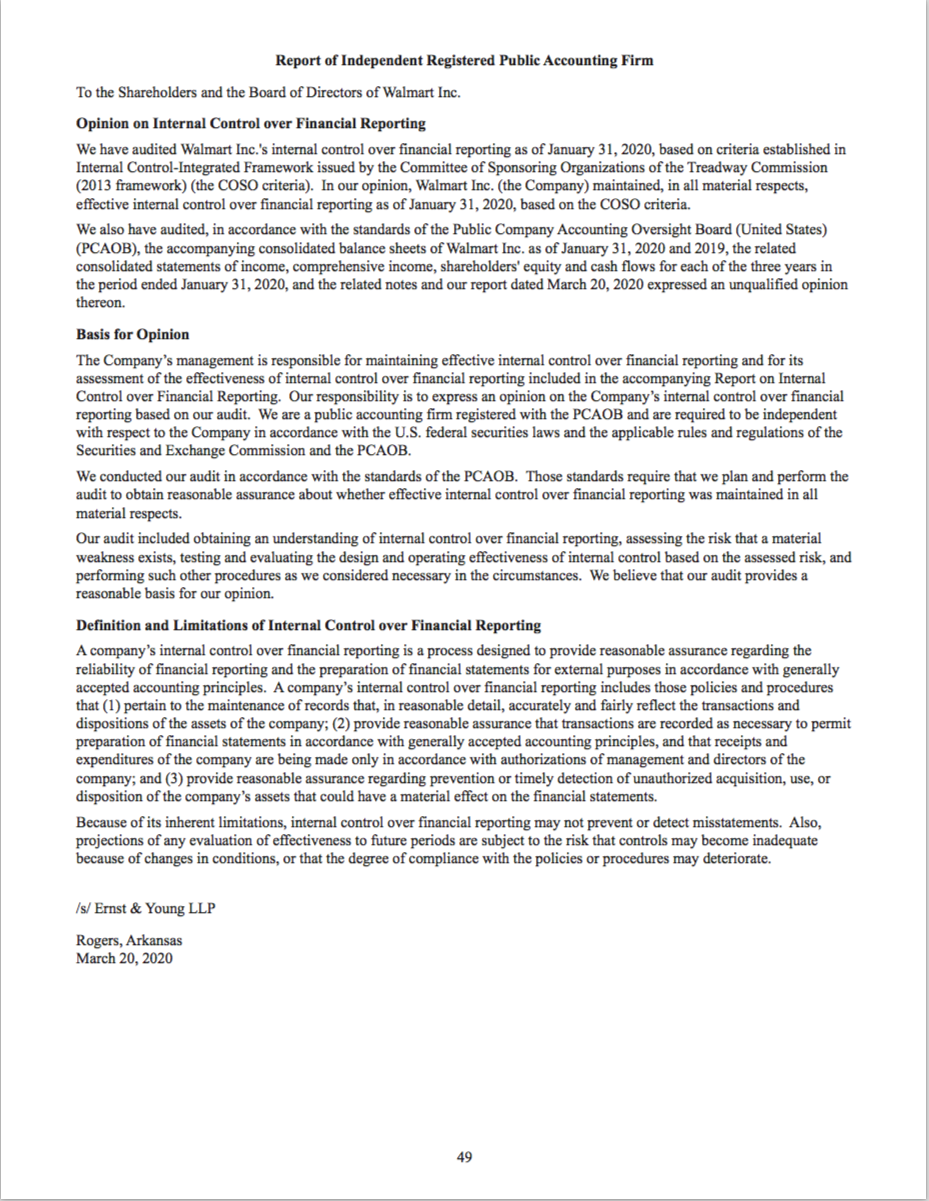

Accountants Report:

1. Who are the independent CPAs?

Target:

The independent auditors of Target Corporation are Ernst and Young LLP (31).

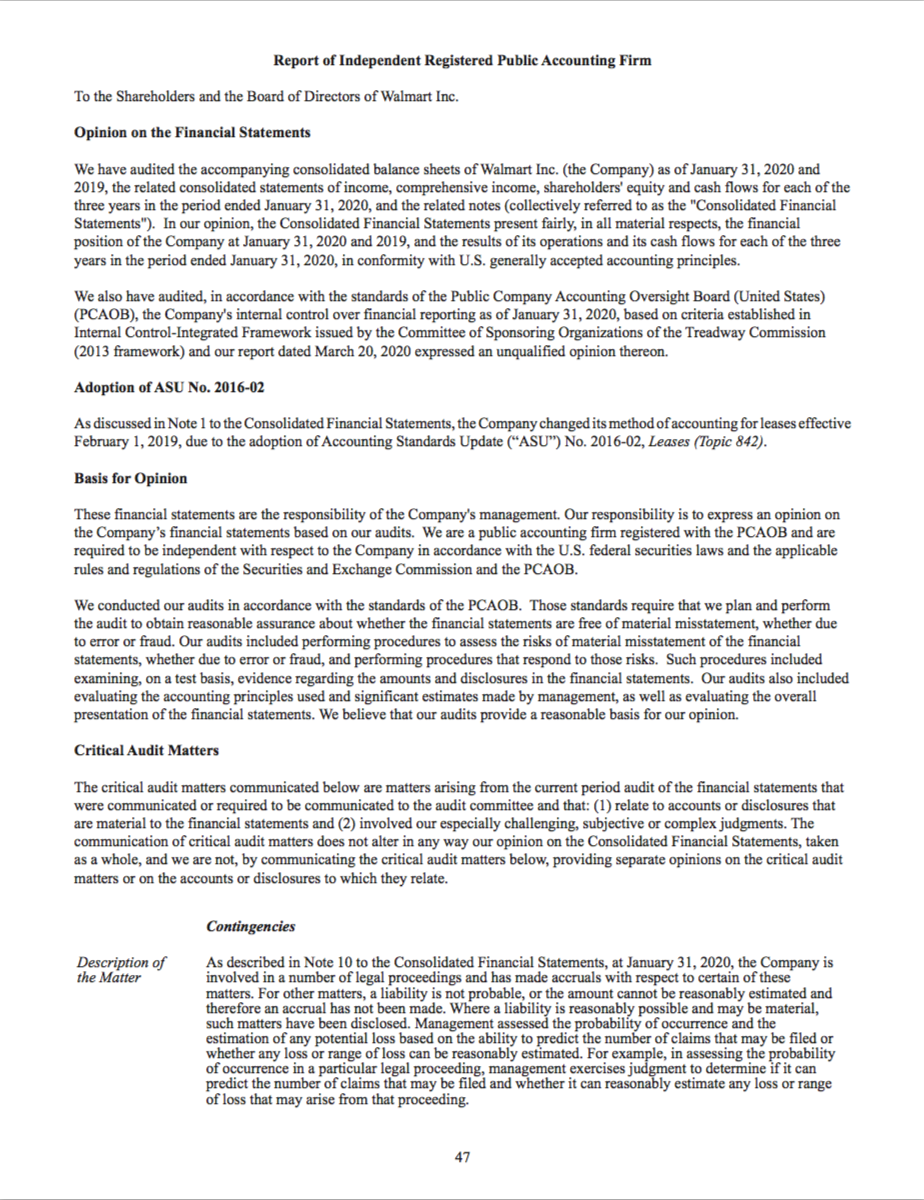

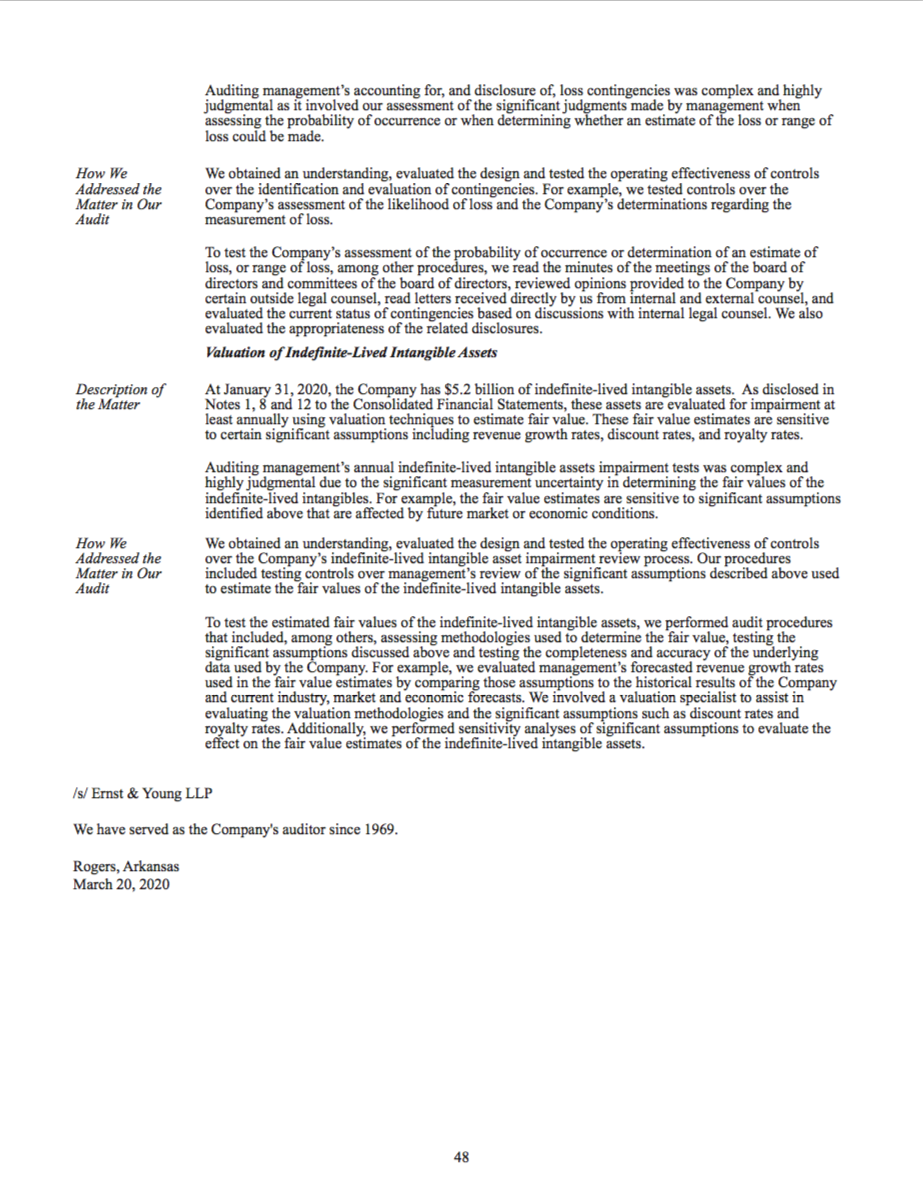

Walmart:

The independent auditors of Walmart Incorporation are Ernst and Young LLP (48).

2. What kind of opinion was issued?

Target:

The auditors issued an unqualified audit opinion. The auditors report states that the consolidated financial Position, consolidated results of operation, and the consolidated statements of cash flows of Target Corporation and its subsidiaries are in conformity with U.S Generally Accepted Accounting Principles (GAAP) (31).

Walmart:

The opinion issued is the Consolidated Financial Statements present fairly, in all material respects: the financial position of the Company at January 31, 2020 and 2019, and the results of its operations and its cash flows for each of the three years in the period ended January 31, 2020, are in conformity with U.S. generally accepted accounting principles (48).

3. Should this report presumably increase the reliability of the financial statements? Why?

Target and Walmart:

Presumably yes, because an independent Auditors Report is an official opinion issued by an external or internal auditor on truth and fairness of financial statements. It gives assurance to shareholders that financial statements which were prepared by management show true and fair or not. In addition, as to the quality and accuracy of the financial statements prepared by a company. The report is a primary source of communication between the auditor and the users of financial statements. The users include equity holders, lenders, creditors. The accountants report expresses an opinion on reviewed financial statements. However, a disclaimer of opinion indicates that one should not look to the auditor's report as an indication of the reliability of the statements. The auditors' opinion, also known as the auditors' report, is a formal opinion, or disclaimer thereof, issued as a result of an internal or external audit or evaluation.

Target: (32) Walmart: (48)

[Target] [Wallmart]

Report of Independent Registered Public Accounting Firm

To the Shareholders and the Board of Directors of Target Corporation

Opinion on the Financial Statements

/s/ Michael J. Fiddelke

Michael J. Fiddelke Executive Vice President and Chief Financial Officer

We have audited the accompanying consolidated statements of financial position of Target Corporation (the Corporation) as of February 1, 2020 and February 2, 2019, the related consolidated statements of operations, comprehensive income, cash flows and shareholders' investment for each of the three years in the period ended February 1, 2020, and the related notes (collectively referred to as the consolidated financial statements). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Corporation at February 1, 2020 and February 2, 2019, and the results of its operations and its cash flows for each of the three years in the period ended February 1, 2020, in conformity with U.S. generally accepted accounting principles.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the Corporation's internal control over financial reporting as of February 1, 2020, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (2013 framework) and our report dated March 11, 2020 expressed an unqualified opinion thereon.

Basis for Opinion

These financial statements are the responsibility of the Corporation's management. Our responsibility is to express an opinion on the Corporations financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Corporation in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

Critical Audit Matters

The critical audit matters communicated below are matters arising from the current period audit of the financial statements that were communicated or required to be communicated to the audit committee and that: (1) relate to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the consolidated financial statements, taken as a whole, and we are not, by communicating the critical audit matters below, providing separate opinions on the critical audit matters or on the accounts or disclosures to which they relate.

TARGET CORPORATION 2019 Form 10-K 31

Description of the Matter

How We Addressed the Matter in Our Audit

Description of the Matter

How We Addressed the Matter in Our Audit

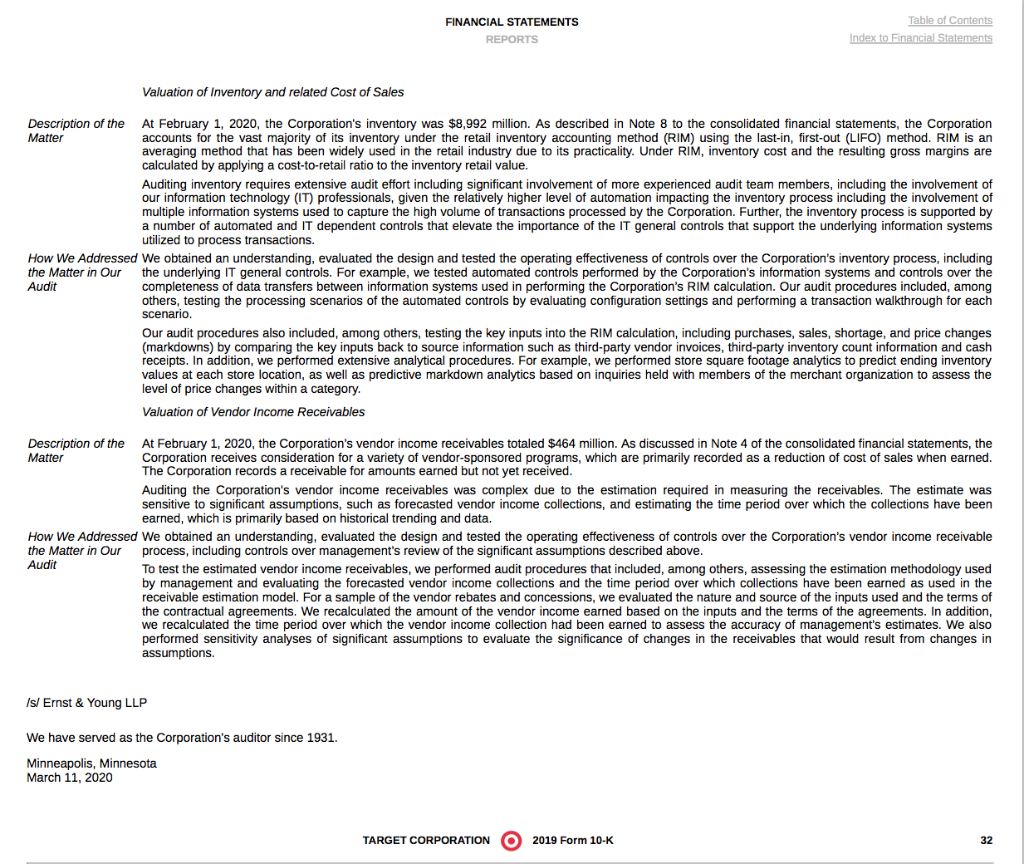

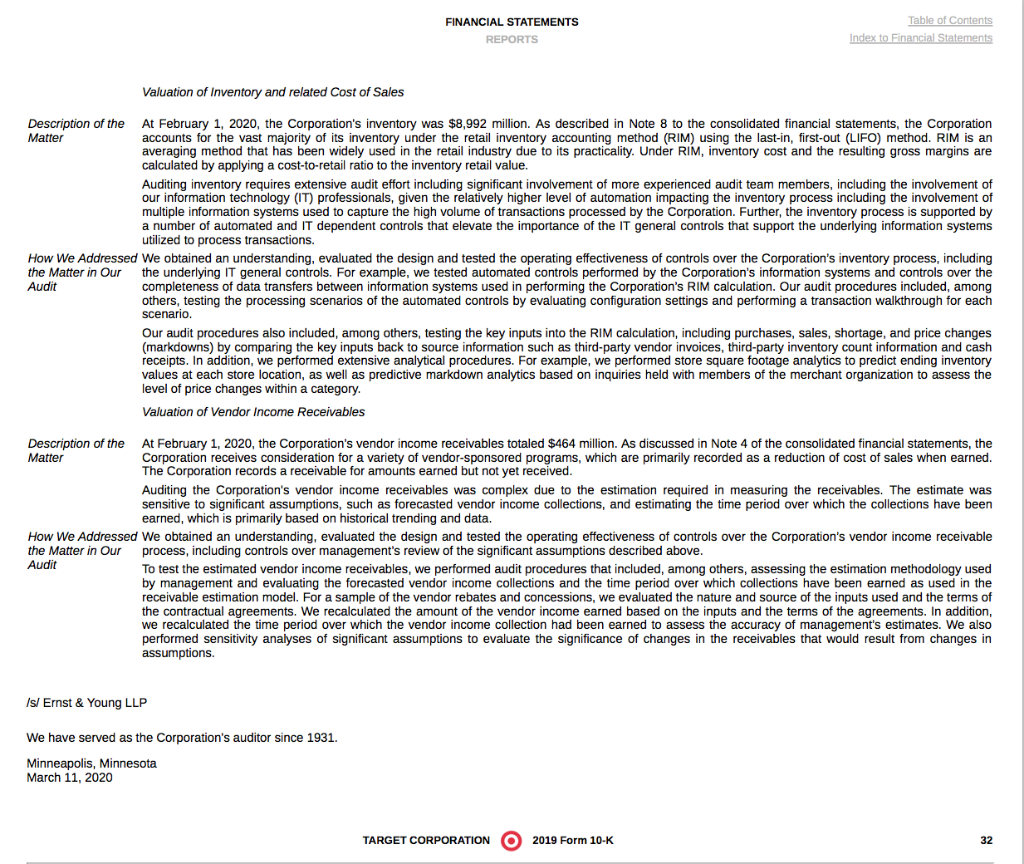

FINANCIAL STATEMENTS Table of Contents REPORTS Index to Financial Statements

At February 1, 2020, the Corporation's inventory was $8,992 million. As described in Note 8 to the consolidated financial statements, the Corporation accounts for the vast majority of its inventory under the retail inventory accounting method (RIM) using the last-in, first-out (LIFO) method. RIM is an averaging method that has been widely used in the retail industry due to its practicality. Under RIM, inventory cost and the resulting gross margins are calculated by applying a cost-to-retail ratio to the inventory retail value.

Auditing inventory requires extensive audit effort including significant involvement of more experienced audit team members, including the involvement of our information technology (IT) professionals, given the relatively higher level of automation impacting the inventory process including the involvement of multiple information systems used to capture the high volume of transactions processed by the Corporation. Further, the inventory process is supported by a number of automated and IT dependent controls that elevate the importance of the IT general controls that support the underlying information systems utilized to process transactions.

We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporations inventory process, including the underlying IT general controls. For example, we tested automated controls performed by the Corporations information systems and controls over the completeness of data transfers between information systems used in performing the Corporations RIM calculation. Our audit procedures included, among others, testing the processing scenarios of the automated controls by evaluating configuration settings and performing a transaction walkthrough for each scenario.

Our audit procedures also included, among others, testing the key inputs into the RIM calculation, including purchases, sales, shortage, and price changes (markdowns) by comparing the key inputs back to source information such as third-party vendor invoices, third-party inventory count information and cash receipts. In addition, we performed extensive analytical procedures. For example, we performed store square footage analytics to predict ending inventory values at each store location, as well as predictive markdown analytics based on inquiries held with members of the merchant organization to assess the level of price changes within a category.

Valuation of Vendor Income Receivables

At February 1, 2020, the Corporations vendor income receivables totaled $464 million. As discussed in Note 4 of the consolidated financial statements, the Corporation receives consideration for a variety of vendor-sponsored programs, which are primarily recorded as a reduction of cost of sales when earned. The Corporation records a receivable for amounts earned but not yet received.

Auditing the Corporation's vendor income receivables was complex due to the estimation required in measuring the receivables. The estimate was sensitive to significant assumptions, such as forecasted vendor income collections, and estimating the time period over which the collections have been earned, which is primarily based on historical trending and data.

We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporations vendor income receivable process, including controls over managements review of the significant assumptions described above.

To test the estimated vendor income receivables, we performed audit procedures that included, among others, assessing the estimation methodology used by management and evaluating the forecasted vendor income collections and the time period over which collections have been earned as used in the receivable estimation model. For a sample of the vendor rebates and concessions, we evaluated the nature and source of the inputs used and the terms of the contractual agreements. We recalculated the amount of the vendor income earned based on the inputs and the terms of the agreements. In addition, we recalculated the time period over which the vendor income collection had been earned to assess the accuracy of managements estimates. We also performed sensitivity analyses of significant assumptions to evaluate the significance of changes in the receivables that would result from changes in assumptions.

Valuation of Inventory and related Cost of Sales

/s/ Ernst & Young LLP

We have served as the Corporation's auditor since 1931.

Minneapolis, Minnesota March 11, 2020

FINANCIAL STATEMENTS REPORTS Table of Contents Index to Financial Statements Valuation of Inventory and related Cost of Sales Description of the At February 1, 2020, the Corporation's inventory was $8,992 million. As described in Note 8 to the consolidated financial statements, the Corporation Matter accounts for the vast majority of its inventory under the retail inventory accounting method (RIM) using the last-in, first-out (LIFO) method. RIM is an averaging method that has been widely used in the retail industry due to its practicality. Under RIM, inventory cost and the resulting gross margins are calculated by applying a cost-to-retail ratio to the inventory retail value. Auditing inventory requires extensive audit effort including significant involvement of more experienced audit team members, including the involvement of our information technology (IT) professionals, given the relatively higher level of automation impacting the inventory process including the involvement of multiple information systems used to capture the high volume of transactions processed by the Corporation. Further, the inventory process is supported by a number of automated and IT dependent controls that elevate the importance of the IT general controls that support the underlying information systems utilized to process transactions. How We Addressed We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporation's inventory process, including the Matter in Our the underlying IT general controls. For example, we tested automated controls performed by the Corporation's information systems and controls over the Audit completeness of data transfers between information systems used in performing the Corporation's RIM calculation. Our audit procedures included, among others, testing the processing scenarios of the automated controls by evaluating configuration settings and performing a transaction walkthrough for each scenario. Our audit procedures also included, among others, testing the key inputs into the RIM calculation, including purchases, sales, shortage, and price changes (markdowns) by comparing the key inputs back to source information such as third-party vendor invoices, third-party inventory count information and cash receipts. In addition, we performed extensive analytical procedures. For example, we performed store square footage analytics to predict ending inventory values at each store location, as well as predictive markdown analytics based on inquiries held with members of the merchant organization to assess the level of price changes within a category. Valuation of Vendor Income Receivables Description of the At February 1, 2020, the Corporation's vendor income receivables totaled $464 million. As discussed in Note 4 of the consolidated financial statements, the Matter Corporation receives consideration for a variety of vendor-sponsored programs, which are primarily recorded as a reduction of cost of sales when earned. The Corporation records a receivable for amounts earned but not yet received. Auditing the Corporation's vendor income receivables was complex due to the estimation required in measuring the receivables. The estimate was sensitive to significant assumptions, such as forecasted vendor income collections, and estimating the time period over which the collections have been earned, which is primarily based on historical trending and data. How We Addressed We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporation's vendor income receivable the Matter in Our process, including controls over management's review of the significant assumptions described above. Audit To test the estimated vendor income receivables, we performed audit procedures that included, among others, assessing the estimation methodology used by management and evaluating the forecasted vendor income collections and the time period over which collections have been earned as used in the receivable estimation model. For a sample of the vendor rebates and concessions, we evaluated the nature and source of the inputs used and the terms of the contractual agreements. We recalculated the amount of the vendor income earned based on the inputs and the terms of the agreements. In addition, we recalculated the time period over which the vendor income collection had been earned to assess the accuracy of management's estimates. We also performed sensitivity analyses of significant assumptions to evaluate the significance of changes in the receivables that would result from changes in assumptions. /s/ Ernst & Young LLP We have served as the Corporation's auditor since 1931. Minneapolis, Minnesota March 11, 2020 TARGET CORPORATION O 2019 Form 10-K 32 FINANCIAL STATEMENTS REPORTS Table of Contents Index to Financial Statements Valuation of Inventory and related Cost of Sales Description of the At February 1, 2020, the Corporation's inventory was $8,992 million. As described in Note 8 to the consolidated financial statements, the Corporation Matter accounts for the vast majority of its inventory under the retail inventory accounting method (RIM) using the last-in, first-out (LIFO) method. RIM is an averaging method that has been widely used in the retail industry due to its practicality. Under RIM, inventory cost and the resulting gross margins are calculated by applying a cost-to-retail ratio to the inventory retail value. Auditing inventory requires extensive audit effort including significant involvement of more experienced audit team members, including the involvement of our information technology (IT) professionals, given the relatively higher level of automation impacting the inventory process including the involvement of multiple information systems used to capture the high volume of transactions processed by the Corporation. Further, the inventory process is supported by a number of automated and IT dependent controls that elevate the importance of the IT general controls that support the underlying information systems utilized to process transactions. How We Addressed We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporation's inventory process, including the Matter in Our the underlying IT general controls. For example, we tested automated controls performed by the Corporation's information systems and controls over the Audit completeness of data transfers between information systems used in performing the Corporation's RIM calculation. Our audit procedures included, among others, testing the processing scenarios of the automated controls by evaluating configuration settings and performing a transaction walkthrough for each scenario. Our audit procedures also included, among others, testing the key inputs into the RIM calculation, including purchases, sales, shortage, and price changes (markdowns) by comparing the key inputs back to source information such as third-party vendor invoices, third-party inventory count information and cash receipts. In addition, we performed extensive analytical procedures. For example, we performed store square footage analytics to predict ending inventory values at each store location, as well as predictive markdown analytics based on inquiries held with members of the merchant organization to assess the level of price changes within a category. Valuation of Vendor Income Receivables Description of the At February 1, 2020, the Corporation's vendor income receivables totaled $464 million. As discussed in Note 4 of the consolidated financial statements, the Matter Corporation receives consideration for a variety of vendor-sponsored programs, which are primarily recorded as a reduction of cost of sales when earned. The Corporation records a receivable for amounts earned but not yet received. Auditing the Corporation's vendor income receivables was complex due to the estimation required in measuring the receivables. The estimate was sensitive to significant assumptions, such as forecasted vendor income collections, and estimating the time period over which the collections have been earned, which is primarily based on historical trending and data. How We Addressed We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporation's vendor income receivable the Matter in Our process, including controls over management's review of the significant assumptions described above. Audit To test the estimated vendor income receivables, we performed audit procedures that included, among others, assessing the estimation methodology used by management and evaluating the forecasted vendor income collections and the time period over which collections have been earned as used in the receivable estimation model. For a sample of the vendor rebates and concessions, we evaluated the nature and source of the inputs used and the terms of the contractual agreements. We recalculated the amount of the vendor income earned based on the inputs and the terms of the agreements. In addition, we recalculated the time period over which the vendor income collection had been earned to assess the accuracy of management's estimates. We also performed sensitivity analyses of significant assumptions to evaluate the significance of changes in the receivables that would result from changes in assumptions. /s/ Ernst & Young LLP We have served as the Corporation's auditor since 1931. Minneapolis, Minnesota March 11, 2020 TARGET CORPORATION O 2019 Form 10-K 32 Report of Independent Registered Public Accounting Firm To the Shareholders and the Board of Directors of Walmart Inc. Opinion on the Financial Statements We have audited the accompanying consolidated balance sheets of Walmart Inc. (the Company) as of January 31, 2020 and 2019, the related consolidated statements of income, comprehensive income, shareholders' equity and cash flows for each of the three years in the period ended January 31, 2020, and the related notes (collectively referred to as the "Consolidated Financial Statements"). In our opinion, the Consolidated Financial Statements present fairly, in all material respects, the financial position of the Company at January 31, 2020 and 2019, and the results of its operations and its cash flows for each of the three years in the period ended January 31, 2020, in conformity with U.S. generally accepted accounting principles. We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the Company's internal control over financial reporting as of January 31, 2020, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (2013 framework) and our report dated March 20, 2020 expressed an unqualified opinion thereon. Adoption of ASU No. 2016-02 As discussed in Note l to the Consolidated Financial Statements, the Company changed its method of accounting for leases effective February 1, 2019, due to the adoption of Accounting Standards Update ("ASU") No. 2016-02, Leases (Topic 842). Basis for Opinion These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on the Company's financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion. Critical Audit Matters The critical audit matters communicated below are matters arising from the current period audit of the financial statements that were communicated or required to be communicated to the audit committee and that: (1) relate to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the Consolidated Financial Statements, taken as a whole, and we are not, by communicating the critical audit matters below, providing separate opinions on the critical audit matters or on the accounts or disclosures to which they relate. Contingencies Description of the Matter As described in Note 10 to the Consolidated Financial Statements, at January 31, 2020, the Company is involved in a number of legal proceedings and has made accruals with respect to certain of these matters. For other matters, a liability is not probable, or the amount cannot be reasonably estimated and therefore an accrual has not been made. Where a liability is reasonably possible and may be material, such matters have been disclosed. Management assessed the probability of occurrence and the estimation of any potential loss based on the ability to predict the number of claims that may be filed or whether any loss or range of loss can be reasonably estimated. For example, in assessing the probability of occurrence in a particular legal proceeding, management exercises judgment to determine if it can predict the number of claims that may be filed and whether it can reasonably estimate any loss or range of loss that may arise from that proceeding. 47 Auditing management's accounting for, and disclosure of, loss contingencies was complex and highly judgmental as it involved our assessment of the significant judgments made by management when assessing the probability of occurrence or when determining whether an estimate of the loss or range of loss could be made. How We Addressed the Matter in Our Audit We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the identification and evaluation of contingencies. For example, we tested controls over the Company's assessment of the likelihood of loss and the Company's determinations regarding the measurement of loss. To test the Company's assessment of the probability of occurrence or determination of an estimate of loss, or range of loss, among other procedures, we read the minutes of the meetings of the board of directors and committees of the board of directors, reviewed opinions provided to the Company by certain outside legal counsel, read letters received directly by us from internal and external counsel, and evaluated the current status of contingencies based on discussions with internal legal counsel. We also evaluated the appropriateness of the related disclosures. Valuation of Indefinite-Lived Intangible Assets Description of the Matter At January 31, 2020, the Company has $5.2 billion of indefinite-lived intangible assets. As disclosed in Notes 1, 8 and 12 to the Consolidated Financial Statements, these assets are evaluated for impairment at least annually using valuation techniques to estimate fair value. These fair value estimates are sensitive to certain significant assumptions including revenue growth rates, discount rates, and royalty rates. Auditing management's annual indefinite-lived intangible assets impairment tests was complex and highly judgmental due to the significant measurement uncertainty in determining the fair values of the indefinite-lived intangibles. For example, the fair value estimates are sensitive to significant assumptions identified above that are affected by future market or economic conditions. We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Company's indefinite-lived intangible asset impairment review process. Our procedures included testing controls over management's review of the significant assumptions described above used to estimate the fair values of the indefinite-lived intangible assets. How We Addressed the Matter in Our Audit To test the estimated fair values of the indefinite-lived intangible assets, we performed audit procedures that included, among others, assessing methodologies used to determine the fair value, testing the significant assumptions discussed above and testing the completeness and accuracy of the underlying data used by the Company. For example, we evaluated management's forecasted revenue growth rates used in the fair value estimates by comparing those assumptions to the historical results of the Company and current industry, market and economic forecasts. We involved a valuation specialist to assist in evaluating the valuation methodologies and the significant assumptions such as discount rates and royalty rates. Additionally, we performed sensitivity analyses of significant assumptions to evaluate the effect on the fair value estimates of the indefinite-lived intangible assets. /s/Ernst & Young LLP We have served as the Company's auditor since 1969. Rogers, Arkansas March 20, 2020 48 Report of Independent Registered Public Accounting Firm To the Shareholders and the Board of Directors of Walmart Inc. Opinion on Internal Control over Financial Reporting We have audited Walmart Inc.'s internal control over financial reporting as of January 31, 2020, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (2013 framework) (the COSO criteria). In our opinion, Walmart Inc. (the Company) maintained, in all material respects, effective internal control over financial reporting as of January 31, 2020, based on the COSO criteria. We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the accompanying consolidated balance sheets of Walmart Inc. as of January 31, 2020 and 2019, the related consolidated statements of income, comprehensive income, shareholders' equity and cash flows for each of the three years in the period ended January 31, 2020, and the related notes and our report dated March 20, 2020 expressed an unqualified opinion thereon. Basis for Opinion The Company's management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting included in the accompanying Report on Internal Control over Financial Reporting. Our responsibility is to express an opinion on the Company's internal control over financial reporting based on our audit. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects. Our audit included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, testing and evaluating the design and operating effectiveness of internal control based on the assessed risk, and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. Definition and Limitations of Internal Control over Financial Reporting A company's internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company's internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements. Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. /s/ Ernst & Young LLP Rogers, Arkansas March 20, 2020 49 FINANCIAL STATEMENTS REPORTS Table of Contents Index to Financial Statements Valuation of Inventory and related Cost of Sales Description of the At February 1, 2020, the Corporation's inventory was $8,992 million. As described in Note 8 to the consolidated financial statements, the Corporation Matter accounts for the vast majority of its inventory under the retail inventory accounting method (RIM) using the last-in, first-out (LIFO) method. RIM is an averaging method that has been widely used in the retail industry due to its practicality. Under RIM, inventory cost and the resulting gross margins are calculated by applying a cost-to-retail ratio to the inventory retail value. Auditing inventory requires extensive audit effort including significant involvement of more experienced audit team members, including the involvement of our information technology (IT) professionals, given the relatively higher level of automation impacting the inventory process including the involvement of multiple information systems used to capture the high volume of transactions processed by the Corporation. Further, the inventory process is supported by a number of automated and IT dependent controls that elevate the importance of the IT general controls that support the underlying information systems utilized to process transactions. How We Addressed We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporation's inventory process, including the Matter in Our the underlying IT general controls. For example, we tested automated controls performed by the Corporation's information systems and controls over the Audit completeness of data transfers between information systems used in performing the Corporation's RIM calculation. Our audit procedures included, among others, testing the processing scenarios of the automated controls by evaluating configuration settings and performing a transaction walkthrough for each scenario. Our audit procedures also included, among others, testing the key inputs into the RIM calculation, including purchases, sales, shortage, and price changes (markdowns) by comparing the key inputs back to source information such as third-party vendor invoices, third-party inventory count information and cash receipts. In addition, we performed extensive analytical procedures. For example, we performed store square footage analytics to predict ending inventory values at each store location, as well as predictive markdown analytics based on inquiries held with members of the merchant organization to assess the level of price changes within a category. Valuation of Vendor Income Receivables Description of the At February 1, 2020, the Corporation's vendor income receivables totaled $464 million. As discussed in Note 4 of the consolidated financial statements, the Matter Corporation receives consideration for a variety of vendor-sponsored programs, which are primarily recorded as a reduction of cost of sales when earned. The Corporation records a receivable for amounts earned but not yet received. Auditing the Corporation's vendor income receivables was complex due to the estimation required in measuring the receivables. The estimate was sensitive to significant assumptions, such as forecasted vendor income collections, and estimating the time period over which the collections have been earned, which is primarily based on historical trending and data. How We Addressed We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporation's vendor income receivable the Matter in Our process, including controls over management's review of the significant assumptions described above. Audit To test the estimated vendor income receivables, we performed audit procedures that included, among others, assessing the estimation methodology used by management and evaluating the forecasted vendor income collections and the time period over which collections have been earned as used in the receivable estimation model. For a sample of the vendor rebates and concessions, we evaluated the nature and source of the inputs used and the terms of the contractual agreements. We recalculated the amount of the vendor income earned based on the inputs and the terms of the agreements. In addition, we recalculated the time period over which the vendor income collection had been earned to assess the accuracy of management's estimates. We also performed sensitivity analyses of significant assumptions to evaluate the significance of changes in the receivables that would result from changes in assumptions. /s/ Ernst & Young LLP We have served as the Corporation's auditor since 1931. Minneapolis, Minnesota March 11, 2020 TARGET CORPORATION O 2019 Form 10-K 32 FINANCIAL STATEMENTS REPORTS Table of Contents Index to Financial Statements Valuation of Inventory and related Cost of Sales Description of the At February 1, 2020, the Corporation's inventory was $8,992 million. As described in Note 8 to the consolidated financial statements, the Corporation Matter accounts for the vast majority of its inventory under the retail inventory accounting method (RIM) using the last-in, first-out (LIFO) method. RIM is an averaging method that has been widely used in the retail industry due to its practicality. Under RIM, inventory cost and the resulting gross margins are calculated by applying a cost-to-retail ratio to the inventory retail value. Auditing inventory requires extensive audit effort including significant involvement of more experienced audit team members, including the involvement of our information technology (IT) professionals, given the relatively higher level of automation impacting the inventory process including the involvement of multiple information systems used to capture the high volume of transactions processed by the Corporation. Further, the inventory process is supported by a number of automated and IT dependent controls that elevate the importance of the IT general controls that support the underlying information systems utilized to process transactions. How We Addressed We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporation's inventory process, including the Matter in Our the underlying IT general controls. For example, we tested automated controls performed by the Corporation's information systems and controls over the Audit completeness of data transfers between information systems used in performing the Corporation's RIM calculation. Our audit procedures included, among others, testing the processing scenarios of the automated controls by evaluating configuration settings and performing a transaction walkthrough for each scenario. Our audit procedures also included, among others, testing the key inputs into the RIM calculation, including purchases, sales, shortage, and price changes (markdowns) by comparing the key inputs back to source information such as third-party vendor invoices, third-party inventory count information and cash receipts. In addition, we performed extensive analytical procedures. For example, we performed store square footage analytics to predict ending inventory values at each store location, as well as predictive markdown analytics based on inquiries held with members of the merchant organization to assess the level of price changes within a category. Valuation of Vendor Income Receivables Description of the At February 1, 2020, the Corporation's vendor income receivables totaled $464 million. As discussed in Note 4 of the consolidated financial statements, the Matter Corporation receives consideration for a variety of vendor-sponsored programs, which are primarily recorded as a reduction of cost of sales when earned. The Corporation records a receivable for amounts earned but not yet received. Auditing the Corporation's vendor income receivables was complex due to the estimation required in measuring the receivables. The estimate was sensitive to significant assumptions, such as forecasted vendor income collections, and estimating the time period over which the collections have been earned, which is primarily based on historical trending and data. How We Addressed We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Corporation's vendor income receivable the Matter in Our process, including controls over management's review of the significant assumptions described above. Audit To test the estimated vendor income receivables, we performed audit procedures that included, among others, assessing the estimation methodology used by management and evaluating the forecasted vendor income collections and the time period over which collections have been earned as used in the receivable estimation model. For a sample of the vendor rebates and concessions, we evaluated the nature and source of the inputs used and the terms of the contractual agreements. We recalculated the amount of the vendor income earned based on the inputs and the terms of the agreements. In addition, we recalculated the time period over which the vendor income collection had been earned to assess the accuracy of management's estimates. We also performed sensitivity analyses of significant assumptions to evaluate the significance of changes in the receivables that would result from changes in assumptions. /s/ Ernst & Young LLP We have served as the Corporation's auditor since 1931. Minneapolis, Minnesota March 11, 2020 TARGET CORPORATION O 2019 Form 10-K 32 Report of Independent Registered Public Accounting Firm To the Shareholders and the Board of Directors of Walmart Inc. Opinion on the Financial Statements We have audited the accompanying consolidated balance sheets of Walmart Inc. (the Company) as of January 31, 2020 and 2019, the related consolidated statements of income, comprehensive income, shareholders' equity and cash flows for each of the three years in the period ended January 31, 2020, and the related notes (collectively referred to as the "Consolidated Financial Statements"). In our opinion, the Consolidated Financial Statements present fairly, in all material respects, the financial position of the Company at January 31, 2020 and 2019, and the results of its operations and its cash flows for each of the three years in the period ended January 31, 2020, in conformity with U.S. generally accepted accounting principles. We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the Company's internal control over financial reporting as of January 31, 2020, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (2013 framework) and our report dated March 20, 2020 expressed an unqualified opinion thereon. Adoption of ASU No. 2016-02 As discussed in Note l to the Consolidated Financial Statements, the Company changed its method of accounting for leases effective February 1, 2019, due to the adoption of Accounting Standards Update ("ASU") No. 2016-02, Leases (Topic 842). Basis for Opinion These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on the Company's financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion. Critical Audit Matters The critical audit matters communicated below are matters arising from the current period audit of the financial statements that were communicated or required to be communicated to the audit committee and that: (1) relate to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the Consolidated Financial Statements, taken as a whole, and we are not, by communicating the critical audit matters below, providing separate opinions on the critical audit matters or on the accounts or disclosures to which they relate. Contingencies Description of the Matter As described in Note 10 to the Consolidated Financial Statements, at January 31, 2020, the Company is involved in a number of legal proceedings and has made accruals with respect to certain of these matters. For other matters, a liability is not probable, or the amount cannot be reasonably estimated and therefore an accrual has not been made. Where a liability is reasonably possible and may be material, such matters have been disclosed. Management assessed the probability of occurrence and the estimation of any potential loss based on the ability to predict the number of claims that may be filed or whether any loss or range of loss can be reasonably estimated. For example, in assessing the probability of occurrence in a particular legal proceeding, management exercises judgment to determine if it can predict the number of claims that may be filed and whether it can reasonably estimate any loss or range of loss that may arise from that proceeding. 47 Auditing management's accounting for, and disclosure of, loss contingencies was complex and highly judgmental as it involved our assessment of the significant judgments made by management when assessing the probability of occurrence or when determining whether an estimate of the loss or range of loss could be made. How We Addressed the Matter in Our Audit We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the identification and evaluation of contingencies. For example, we tested controls over the Company's assessment of the likelihood of loss and the Company's determinations regarding the measurement of loss. To test the Company's assessment of the probability of occurrence or determination of an estimate of loss, or range of loss, among other procedures, we read the minutes of the meetings of the board of directors and committees of the board of directors, reviewed opinions provided to the Company by certain outside legal counsel, read letters received directly by us from internal and external counsel, and evaluated the current status of contingencies based on discussions with internal legal counsel. We also evaluated the appropriateness of the related disclosures. Valuation of Indefinite-Lived Intangible Assets Description of the Matter At January 31, 2020, the Company has $5.2 billion of indefinite-lived intangible assets. As disclosed in Notes 1, 8 and 12 to the Consolidated Financial Statements, these assets are evaluated for impairment at least annually using valuation techniques to estimate fair value. These fair value estimates are sensitive to certain significant assumptions including revenue growth rates, discount rates, and royalty rates. Auditing management's annual indefinite-lived intangible assets impairment tests was complex and highly judgmental due to the significant measurement uncertainty in determining the fair values of the indefinite-lived intangibles. For example, the fair value estimates are sensitive to significant assumptions identified above that are affected by future market or economic conditions. We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Company's indefinite-lived intangible asset impairment review process. Our procedures included testing controls over management's review of the significant assumptions described above used to estimate the fair values of the indefinite-lived intangible assets. How We Addressed the Matter in Our Audit To test the estimated fair values of the indefinite-lived intangible assets, we performed audit procedures that included, among others, assessing methodologies used to determine the fair value, testing the significant assumptions discussed above and testing the completeness and accuracy of the underlying data used by the Company. For example, we evaluated management's forecasted revenue growth rates used in the fair value estimates by comparing those assumptions to the historical results of the Company and current industry, market and economic forecasts. We involved a valuation specialist to assist in evaluating the valuation methodologies and the significant assumptions such as discount rates and royalty rates. Additionally, we performed sensitivity analyses of significant assumptions to evaluate the effect on the fair value estimates of the indefinite-lived intangible assets. /s/Ernst & Young LLP We have served as the Company's auditor since 1969. Rogers, Arkansas March 20, 2020 48 Report of Independent Registered Public Accounting Firm To the Shareholders and the Board of Directors of Walmart Inc. Opinion on Internal Control over Financial Reporting We have audited Walmart Inc.'s internal control over financial reporting as of January 31, 2020, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (2013 framework) (the COSO criteria). In our opinion, Walmart Inc. (the Company) maintained, in all material respects, effective internal control over financial reporting as of January 31, 2020, based on the COSO criteria. We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the accompanying consolidated balance sheets of Walmart Inc. as of January 31, 2020 and 2019, the related consolidated statements of income, comprehensive income, shareholders' equity and cash flows for each of the three years in the period ended January 31, 2020, and the related notes and our report dated March 20, 2020 expressed an unqualified opinion thereon. Basis for Opinion The Company's management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting included in the accompanying Report on Internal Control over Financial Reporting. Our responsibility is to express an opinion on the Company's internal control over financial reporting based on our audit. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects. Our audit included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, testing and evaluating the design and operating effectiveness of internal control based on the assessed risk, and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. Definition and Limitations of Internal Control over Financial Reporting A company's internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company's internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements. Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. /s/ Ernst & Young LLP Rogers, Arkansas March 20, 2020 49

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts