Question

Interest Rate Swaps: Use the following information from the balance sheet to construct a swap of asset cash flows for the bank. The bank is

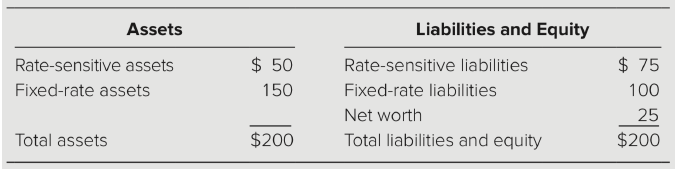

Interest Rate Swaps: Use the following information from the balance sheet to construct a swap of asset cash flows for the bank. The bank is a price taker in both the fixed-rate market at 9% and the rate-sensitive market at the T-bill rate plus 1.5%. A securities dealer has a large portfolio of rate-sensitive assets funded with fixed-rate liabilities. The dealer is a price taker in a fixed-rate market paying 8.5% and a floating-rate market paying the 91-day T bill rate plus 1.25%. All interest is paid annually.

What is the interest rate risk exposure to the bank? How can the bank use a swap to hedge its interest rate risk exposure?

What is the interest rate risk exposure to the securities dealer? How can the securities dealer use a swap to hedge its interest rate risk exposure?

Assets Rate-sensitive assets Fixed-rate assets $ 50 150 Liabilities and Equity Rate-sensitive liabilities Fixed-rate liabilities Net worth Total liabilities and equity $ 75 100 25 $200 Total assets $200Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Of Capital In Managerial Finance

Authors: Dennis Schlegel

2015th Edition

3319151347, 978-3319151342