Answered step by step

Verified Expert Solution

Question

1 Approved Answer

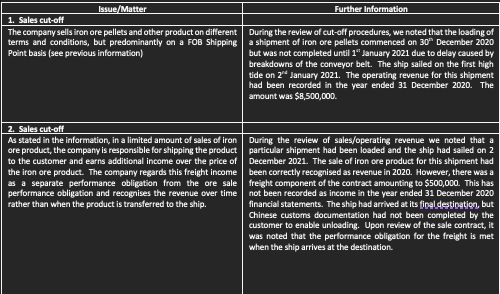

please help with recommendations Issue/Matter Further Information 1. Sales cut-off The company sells iron ore pellets and other product on different During the review of

please help with recommendations

Issue/Matter Further Information 1. Sales cut-off The company sells iron ore pellets and other product on different During the review of cut-off procedures, we noted that the loading of terms and conditions, but predominantly on a FOB Shipping a shipment of iron ore pellets commenced on 30 December 2020 Point basis (see previous information) but was not completed until 1" January 2021 due to delay caused by breakdowns of the conveyor belt. The ship sailed on the first high tide on 2 January 2021. The operating revenue for this shipment had been recorded in the year ended 31 December 2020. The amount was $8,500,000 2. Sales cut-off As stated in the information, in a limited amount of sales of iron During the review of sales/operating revenue we noted that a ore product, the company is responsible for shipping the product particular shipment had been loaded and the ship had sailed on 2 to the customer and earns additional income over the price of December 2021. The sale of iron ore product for this shipment had the iron ore product. The company regards this freight income been correctly recognised as revenue in 2020. However, there was a as a separate performance obligation from the ore sale freight component of the contract amounting to $500,000. This has performance obligation and recognises the revenue over time not been recorded as income in the year ended 31 December 2020 rather than when the product is transferred to the ship. financial statements. The ship had arrived at its final destination, but Chinese customs documentation had not been completed by the customer to enable unloading. Upon review of the sale contract, it was noted that the performance obligation for the freight is met when the ship arrives at the destination No. Key audit matter Assessment of the Implications of the audit matter Recommendations to management Sales cut-off ASA 560, paragraph 6 has stated, all events occur when the product is shipped without a shipping document, or the shipping invoice not on the correct trading date or is late. Therefore, determining sales is a major mistake. + Unresolved errors are not materially misstated 1 Sales cut-off According to AUS 306 showing that the basis for claiming sales revenue is materially erroneous; The auditor should obtain a report from management explaining the impact of uncorrected misstatements. When a freight component of the contract is discovered up to $500,000, which has not yet been recognized. This will result in products being shipped without shipping documents and shipping invoices that do not reflect the correct transaction date or are incorrect in value. So there is the problem of sales cut-off. Pursuant to paragraph 11 of ASA 700: + The auditor has obtained sufficient appropriate evidence about the unresolved matters 2Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Telecourse Guide For Accounting In Action Managerial Accounting

Authors: Ray H. Garrison, Eric W. Noreen

9th Edition

0072386533, 978-0072386530