Answered step by step

Verified Expert Solution

Question

1 Approved Answer

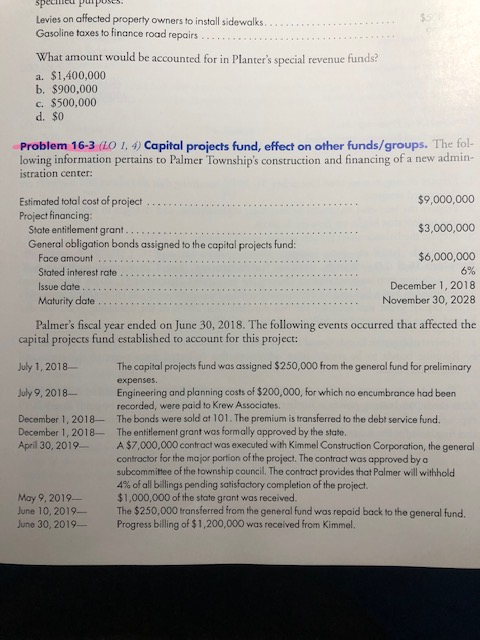

specifie Levies on affected property owners to install sidewalks... Gasoline taxes to finance road repairs What amount would be accounted for in Planter's special

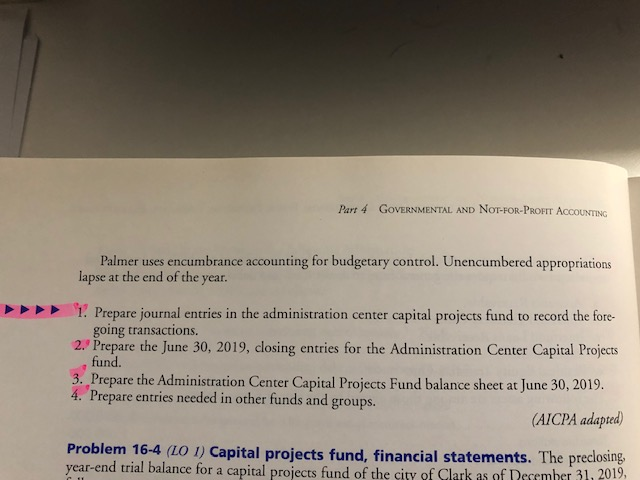

specifie Levies on affected property owners to install sidewalks... Gasoline taxes to finance road repairs What amount would be accounted for in Planter's special revenue funds? a. $1,400,000 b. $900,000 c. $500,000 d. $0 Problem 16-3 (LO 1, 4) Capital projects fund, effect on other funds/groups. The fol- lowing information pertains to Palmer Township's construction and financing of a new admin- istration center: Estimated total cost of project Project financing: State entitlement grant... General obligation bonds assigned to the capital projects fund: Face amount Stated interest rate Issue date.. Maturity date $9,000,000 $3,000,000 $6,000,000 6% December 1, 2018 November 30, 2028 Palmer's fiscal year ended on June 30, 2018. The following events occurred that affected the capital projects fund established to account for this project: July 1, 2018- July 9, 2018- December 1, 2018 December 1, 2018 April 30, 2019- May 9, 2019- June 10, 2019- June 30, 2019- The capital projects fund was assigned $250,000 from the general fund for preliminary expenses. Engineering and planning costs of $200,000, for which no encumbrance had been recorded, were paid to Krew Associates. The bonds were sold at 101. The premium is transferred to the debt service fund. The entitlement grant was formally approved by the state. A $7,000,000 contract was executed with Kimmel Construction Corporation, the general contractor for the major portion of the project. The contract was approved by a subcommittee of the township council. The contract provides that Palmer will withhold 4% of all billings pending satisfactory completion of the project. $1,000,000 of the state grant was received. The $250,000 transferred from the general fund was repaid back to the general fund. Progress billing of $1,200,000 was received from Kimmel. Part 4 GOVERNMENTAL AND NOT-FOR-PROFIT ACCOUNTING Palmer uses encumbrance accounting for budgetary control. Unencumbered appropriations lapse at the end of the year. 1. Prepare journal entries in the administration center capital projects fund to record the fore- going transactions. 2. Prepare the June 30, 2019, closing entries for the Administration Center Capital Projects fund. 3. Prepare the Administration Center Capital Projects Fund balance sheet at June 30, 2019. 4. Prepare entries needed in other funds and groups. (AICPA adapted) Problem 16-4 (LO 1) Capital projects fund, financial statements. The preclosing year-end trial balance for a capital projects fund of the city of Clark as of 31, 2019,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To solve these problems well address both parts the special revenue funds for Planter and the capital projects fund for Palmer Township Part 1 Planter...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Why CISOs Fail Internal Audit And IT Audit The Missing Link In Security Management How To Fix It

Authors: Barak Engel

1st Edition

1138197890, 978-1138197893