Answered step by step

Verified Expert Solution

Question

1 Approved Answer

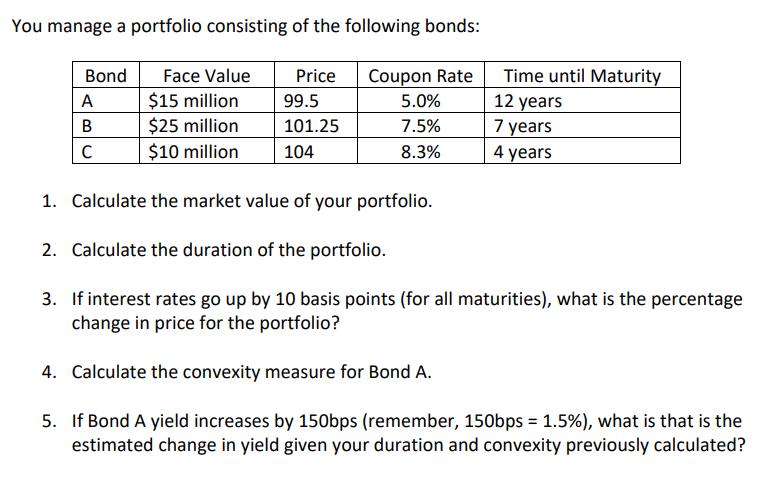

You manage a portfolio consisting of the following bonds: Bond Face Value Price Coupon Rate Time until Maturity A $15 million 99.5 5.0% 12

You manage a portfolio consisting of the following bonds: Bond Face Value Price Coupon Rate Time until Maturity A $15 million 99.5 5.0% 12 years B $25 million 101.25 7.5% 7 years C $10 million 104 8.3% 4 years 1. Calculate the market value of your portfolio. 2. Calculate the duration of the portfolio. 3. If interest rates go up by 10 basis points (for all maturities), what is the percentage change in price for the portfolio? 4. Calculate the convexity measure for Bond A. 5. If Bond A yield increases by 150bps (remember, 150bps = 1.5%), what is that is the estimated change in yield given your duration and convexity previously calculated?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To solve this problem we need to calculate the market value of the portfolio the duration of the por...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations of Finance The Logic and Practice of Financial Management

Authors: Arthur J. Keown, John D. Martin, J. William Petty

8th edition

132994879, 978-0132994873