Tax

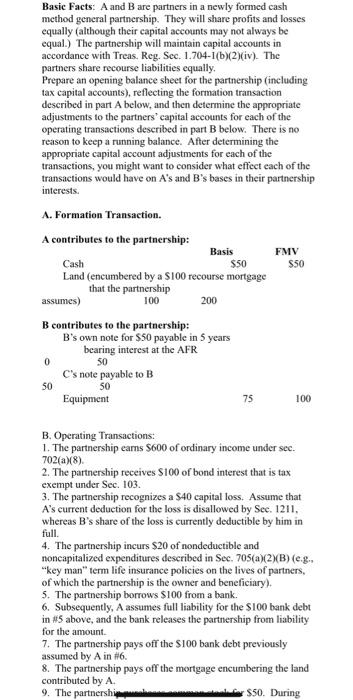

Basic Facts: A and B are partners in a newly formed cash method general partnership. They will share profits and losses equally (although their capital accounts may not always be equal.) The partnership will maintain capital accounts in accordance with Treas. Reg. Scc. 1.704-1(b)(2)(iv). The partners share recourse liabilities equally, Prepare an opening balance sheet for the partnership (including tax capital accounts), reflecting the formation transaction described in part A below, and then determine the appropriate adjustments to the partners' capital accounts for each of the operating transactions described in part B below. There is no reason to keep a running balance. After determining the appropriate capital account adjustments for each of the transactions, you might want to consider what effect each of the transactions would have on A's and B's bases in their partnership interests. FMV $50 A. Formation Transaction. A contributes to the partnership: Basis Cash $50 Land (encumbered by a S100 recourse mortgage that the partnership assumes) 100 200 B contributes to the partnership: B's own note for $50 payable in 5 years bearing interest at the AFR 0 50 C's note payable to B 50 50 Equipment 75 100 B. Operating Transactions: 1. The partnership earns $600 of ordinary income under sec. 702(a)(8) 2. The partnership receives S100 of bond interest that is tax exempt under Sec. 103. 3. The partnership recognizes a $40 capital loss. Assume that A's current deduction for the loss is disallowed by Sec. 1211, whereas B's share of the loss is currently deductible by him in full 4. The partnership incurs $20 of nondeductible and noncapitalized expenditures described in Sec. 705(a)(2XB) (eg.. "key man" term life insurance policies on the lives of partners, of which the partnership is the owner and beneficiary), 5. The partnership borrows $100 from a bank. 6. Subsequently, A assumes full liability for the S100 bank debt in 5 above, and the bank releases the partnership from liability for the amount 7. The partnership pays off the $100 bank debt previously assumed by A in 6. 8. The partnership pays off the mortgage encumbering the land contributed by A 9. The partnershi $50. During 8. The partnership pays off the mortgage encumbering the land contributed by A. 9. The partnership purchases common stock for $50. During the year the stock appreciates to $100, and the partnership distributes it to A. 10. The partnership purchases land for $200 by paying $100 cash and giving the seller a $100 recourse purchase-money mortgage. While the land is still worth $200, the partnership distributes it to A, subject to the mortgage. Does your answer depend on whether A formally assumes the liability and whether the partnership is released by the lender? 11. The partnership distributes to B its promissory note payable to B in a later year ($100 face amount with interest at the applicable federal rate). 8. The partnership pays off the mortgage encumbering the land contributed by A. 9. The partnership purchases common stock for $50. During the year the stock appreciates to $100, and the partnership distributes it to A. 10. The partnership purchases land for $200 by paying $100 cash and giving the seller a $100 recourse purchase-money mortgage. While the land is still worth $200, the partnership distributes it to A, subject to the mortgage. Does your answer depend on whether A formally assumes the liability and whether the partnership is released by the lender? 11. The partnership distributes to B its promissory note payable to B in a later year ($100 face amount with interest at the applicable federal rate)